Extend and pretend kicks into high gear. For example, the $975 million mortgage on a San Francisco office tower.

By Wolf Richter for WOLF STREET.

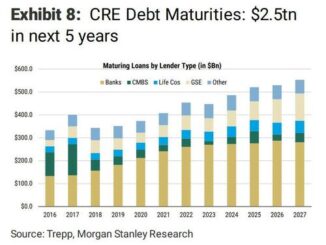

The portion of the $4.7 trillion in US commercial real estate debt that will come due this year – and in theory must be paid off through a sale, refinanced, or extended to avoid default – has ballooned from $659 billion to $929 billion, the Mortgage Bankers Association said today.

The reason the loan maturities ballooned in 2024 from the initial figure of $659 billion to $929 billion today is that many loans that matured in 2023 and were supposed to be paid off in 2023, were in fact not paid off.

Instead, the loans have been modified and extended into 2024 and others were extended further into the future, the MBA said in its report today. The dollar amounts reflect the unpaid principal balance as of December 31, 2023.

Lenders and landlords – those landlords that want to keep the property rather than walking away from it – are dealing with this situation each by holding a gun to the other’s head to make a deal, as we’ll see in a moment. Results may vary.

The new figures for maturities in 2024 by investor type, according to the MBA today:

$28 billion: government-backed mortgages (Fannie Mae, Freddie Mac, FHA, and Ginnie Mae) on multifamily and health-care buildings

$59 billion: held by life insurance companies.

$441 billion: held by banks, including foreign banks around the world that have now started to confess to their loan losses on US CRE. The MBA did not say what portion was held by US banks, and what portion was held by foreign banks.

$234 billion: in commercial mortgage-backed securities (CMBS), collateralized loan obligations (CLOs), and other asset-backed securities (ABS)

$168 billion: held by other credit companies of all types, including mortgage REITs, PE firms, and private-credit providers.

Maturities in 2024 by CRE type:

12% of loans backed by multifamily properties

17% of loans backed by retail properties

18% of loans backed by healthcare properties

25% of loans backed by office properties

27% of loans backed by industrial properties

38% of loans backed by lodging properties.

Landlords and lenders hold a gun to each other’s head.

For example, on February 6, 2024, a $975 million loan on a 1.58 million square-foot One Market Plaza office tower in San Francisco matured. In January, credit-rating agency KBRA warned that the loan faced “imminent maturity default.”

The tower, owned by a joint-venture of Blackstone and Paramount Group, was built in the 1970s and renovated in 2016. It was refinanced in 2017 with an interest-only mortgage of $975 million, which was then securitized into a single-asset CMBS (OMPT 2017-1 MKT) and sold to investors, including a variety of bond funds.

Google, which is on an aggressive push to reduce its office footprint, is the largest tenant in the building, with 21.6% of the space; the lease expires in 2025. Visa is the second-largest tenant with 10.2% of the space; the lease expires in 2026.

According to Trepp, which tracks CMBS, the tower had an occupancy rate of 96% as of September 2023. So that was good. But the biggest leases are set to expire this year and next year, and companies have used lease expiration as an opportunity to cut their footprint.

San Francisco is the worst among major office markets, with an availability rate of 36.7%; Dallas is in second place, with an availability rate of 30%. Atlanta and Houston follow closely behind. So when a loan matures on an office tower in San Francisco, and if the landlord defaults, the lender ends up with the tower and has to sell it at huge loss.

That loss that lenders take when selling the property in the current environment is the gun the landlord holds to the lender’s head. Everyone knows Blackstone is serious; it already got lenders stuck with some properties, including, as we discussed here, an office tower in Manhattan.

And the lender can take the building away from the landlord, which is the gun that the lender holds to the landlord’s head. That gun is loaded with blanks, if the landlord doesn’t want to keep the property. But if they do want to keep the property, that gun works.

Extend and pretend.

So the Blackstone-Paramount joint-venture and the special servicer representing the CMBS holders sat down and made a deal in January, ahead of the loan expiration, and last week, they announced the details of their deal: the mortgage was modified and extended.

The joint venture agreed to pay down by $125 million the existing $975 million loan and bring it to $850 million.

This modified loan has been extended for three years to February 2027, with an option to extend it for another year.

The existing loan’s fixed interest rate of 4.03% was raised to 4.08% for the modified loan.

So the landlord got a huge deal in terms of the interest rate (4.08%, fixed for three years), which is below the three-year Treasury yield (currently 4.26%), and far below current CRE mortgage rates. And they got a huge deal by not having to get a new loan, which would have been nearly impossible, and much more expensive.

The CMBS holders got a deal because the loan was paid down by $125 million, thus reducing their exposure and potential loss, and because they didn’t end up with an older office tower that they would have to sell in the worst office market in the US, and take massive losses.

Now both parties pray that in three years office CRE is a changed world with full offices, low availability rates, higher rents, and much lower interest rates. And if that’s not the case, it’ll start all over again. But until then, extend and pretend averted massive losses for both parties.

That’s how the better office properties will be dealt with: Extend and pretend in the hope for better times. Weaker office properties – where extend and pretend cannot be worked out – will go back to the lenders, and they get to sort out the fate of those properties at massive loss ratios.

ENB Top News

ENB

Energy Dashboard

ENB Podcast

ENB Substack