U.S. commercial crude oil inventories fell for the seventh consecutive week, according to the latest U.S. Energy Information Administration (EIA) Weekly Petroleum Status Report for the week ending June 5, 2026. Commercial crude stocks (excluding the Strategic Petroleum Reserve) dropped by 7.2 million barrels to 426.5 million barrels — now about 5% below the five-year average for this time of year.

This draw exceeded analyst expectations and continues a trend of tightening supplies, driven by strong refinery runs and elevated exports amid global supply disruptions.

Crude Oil Inventories: Persistently Low Relative to History

Commercial crude inventories have hovered in the 400–500 million barrel range in recent years but are trending lower amid sustained draws. Historical data show levels often reached higher peaks in the mid-2010s to early 2020s before settling into a more moderate band. Current levels sit toward the lower end of recent norms, especially with ongoing weekly withdrawals.

US Commercial Crude Oil Inventories (2010–2026). Levels remain elevated compared to 2010–2015 but have been under pressure in 2026. Source: EIA.

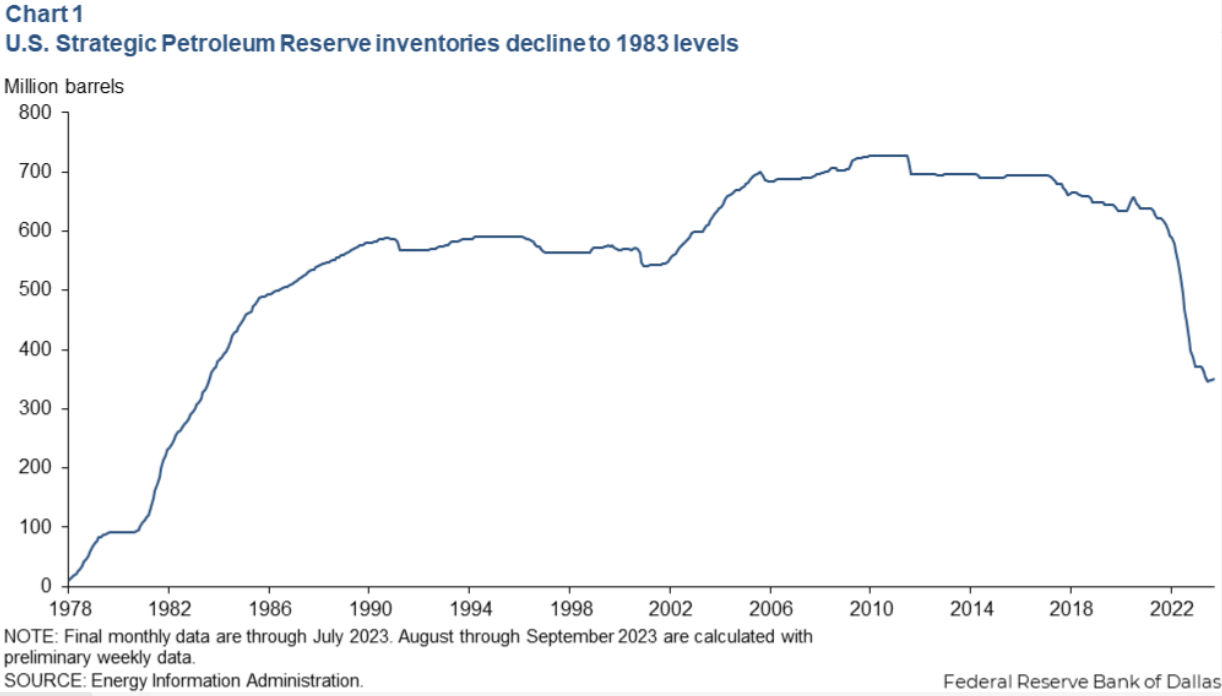

Strategic Petroleum Reserve (SPR) Continues Sharp DeclineThe SPR has seen accelerated drawdowns in 2026. As of June 5, 2026, SPR crude stocks stood at approximately 349.2 million barrels, down significantly from around 415 million barrels earlier in the year.

This marks one of the lower points in recent history following years of releases. Over the longer term (last 10+ years), the SPR peaked well above 700 million barrels in the late 2000s/early 2010s before gradual declines accelerated in recent periods.

U.S. Strategic Petroleum Reserve inventories have declined sharply, approaching levels not seen in decades. Source: Historical EIA data via Federal Reserve analysis.

Refined Products: Gasoline Builds Slightly, But Distillates and Broader Picture Tight

Motor Gasoline: Inventories rose by 186,000 barrels to approximately 215.1 million barrels — still about 6% below the five-year average.

Distillate Fuel Oil (primarily diesel and heating oil): Fell by 200,000 barrels to about 102.1 million barrels — roughly 13% below the five-year average.

Jet Fuel (Kerosene-type): Stocks reached a new year-to-date high around 45.4 million barrels in recent weeks, remaining above some shorter-term averages thanks to record U.S. production and exports. However, broader transportation fuel inventories (gasoline + distillate + jet) are forecast to trend toward multi-decade lows by year-end.

U.S. transportation fuel ending inventories (gasoline, distillate, jet fuel) historical and forecast. EIA projects significant tightening into 2026. Source: EIA Short-Term Energy Outlook.

High refinery utilization (95.3% of operable capacity last week) and strong product supplied numbers reflect efforts to meet demand and offset global shortfalls.

![]()

Oil Prices: Recent Pullback Provides Temporary Relief, But Volatility Looms

WTI crude futures (July 2026 contract) have traded in the mid-to-high $80s recently, with prices dipping toward the low-to-mid $80s amid some profit-taking or negotiation hopes. This represents a pullback from higher levels seen earlier amid peak tensions.

The market faces a key technical event: the looming expiration/rollover of the July 2026 WTI crude futures contract, with last trading days clustered around June 22–24, 2026. Futures rollovers often amplify volatility as positions shift to the next month (August), potentially exacerbating swings driven by positioning, contango/backwardation shifts, and headline risk.

Geopolitical Tensions: The Core Driver of Inventory Draws

Ongoing U.S.-Iran conflict (escalated in late February 2026 following strikes and the blockade of the Strait of Hormuz) has disrupted significant global oil flows. The U.S. has ramped up exports and refinery activity to help fill gaps, directly contributing to domestic inventory draws. Industry voices, including from the American Petroleum Institute, have warned of supply strains, with some forecasts (e.g., ExxonMobil commentary) highlighting risks of much higher prices ($140–$160/bbl range in worst-case unresolved scenarios) if the situation deteriorates further. Negotiations for a potential resolution are reportedly underway.

What This Means for Consumers

U.S. retail gasoline prices have eased somewhat recently but remain elevated. The national average for regular gasoline stands around $4.09–$4.15 per gallon (as of mid-June 2026), with on-highway diesel near $5.21/gallon.

Short-term relief is possible from the recent dip in crude prices and slight gasoline inventory build. However, persistently low distillate stocks, ongoing crude draws, high summer driving demand, and geopolitical uncertainty create upside risk for pump prices. Further escalation or prolonged tight supplies could push averages higher, adding to household and business costs.

What This Means for Investors

Energy producers and upstream companies:

Stand to benefit from tight global supplies and potential price spikes. Volatility around the June 24 contract rollover could create trading opportunities.

Refiners: Mixed — high utilization supports margins, but feedstock (crude) costs and product price dynamics add complexity.

Broader market: Higher energy costs contribute to inflationary pressures. Watch for any de-escalation news, which could trigger a sharp oil price reversal.

Risk management: Position sizing around the futures rollover and geopolitical headlines is critical. Diversification into energy-related assets or hedges may appeal to those bullish on structural tightness.

Overall, U.S. inventory data signals a tightening market responding to global disruptions. While recent lower oil prices offer a buffer, the combination of low stocks, the June 24 futures contract dynamics, and geopolitical uncertainty points to continued volatility. Consumers should prepare for potentially higher fuel costs, while investors have opportunities amid the swings — but timing and risk awareness will be key.

Monitor the next EIA report (June 17) and any developments on Hormuz negotiations closely.

Appendix: Sources and Links

- EIA Weekly Petroleum Status Report (week ending June 5, 2026): https://www.eia.gov/petroleum/supply/weekly/ and summary PDF: https://ir.eia.gov/wpsr/wpsrsummary.pdf

- EIA Crude Oil Stocks Data: https://www.eia.gov/dnav/pet/pet_stoc_wstk_dcu_nus_w.htm

- EIA SPR Historical Data: https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=WCSSTUS1&f=W

- EIA Short-Term Energy Outlook (for forecasts and product details): https://www.eia.gov/outlooks/steo/

- CME Group WTI Crude Futures Quotes (July 2026 contract details): https://www.cmegroup.com/markets/energy/crude-oil/light-sweet-crude.quotes.html

- AAA National Average Gas Prices: https://gasprices.aaa.com/

- EIA U.S. All Grades Retail Gasoline Prices: https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=pet&s=emm_epm0_pte_nus_dpg&f=w

- Additional context from Reuters, Oilprice.com, and industry reports on inventory trends and geopolitical impacts (specific articles cited inline where applicable).

Data as of the latest available EIA release (June 10, 2026) and market closes around June 12–13, 2026. Always verify latest figures directly from primary sources, as markets move quickly.