China Merchants Energy Shipping (CMES) is doubling down on Very Large Crude Carriers (VLCCs), signaling strong long-term confidence in global crude oil trade despite short-term market volatility. In a recent Lloyd’s List report, the Chinese shipping giant dismissed a nearly 40% drop in VLCC spot rates since late June 2026 as a temporary distortion, raising its second-half rate outlook on expectations of recovering Chinese crude imports and robust Middle East Gulf (MEG) export activity.

This stance aligns with CMES’s aggressive fleet expansion. The company has placed significant newbuilding orders, including five VLCCs and five Aframaxes valued at around $930 million with deliveries scheduled for 2027–2028, as part of a broader rumored 100-ship ordering plan.

Additional orders for VLCCs at domestic yards like Dalian Shipbuilding Industry Co. (DSIC) underscore its commitment to modernizing and scaling its fleet for long-haul crude transport.

Why this matters: Long-term investors betting on sustained demand

Major players like CMES wouldn’t commit billions to new VLCCs if they anticipated a structural decline in oil demand. These are sophisticated, state-backed investors with deep visibility into China’s energy needs and global trade flows. Their actions reflect a belief that crude oil will remain a cornerstone of the global energy mix for decades, driven by economic growth in Asia and elsewhere.

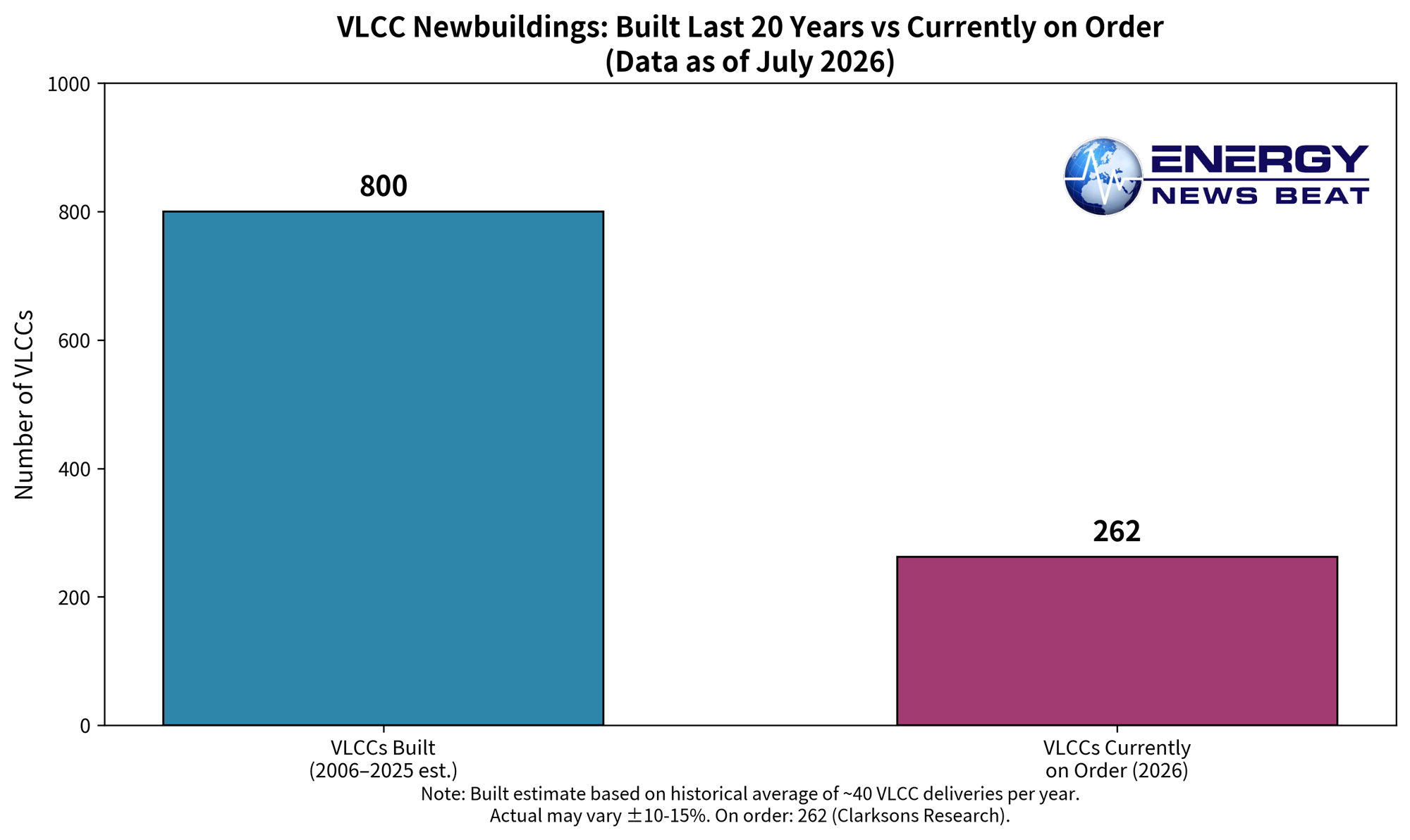

The broader VLCC market reinforces this view. The global orderbook has hit record highs, with 262 VLCCs on order and 127 contracted in 2026 alone — the highest annual total since 1973. The orderbook now represents roughly 30% of the existing fleet.

China dominates VLCC shipbuilding

China has secured over 90% of global new VLCC orders in recent periods, highlighting its overwhelming dominance in high-value tanker construction. Chinese shipyards’ advantages in cost, quality, delivery timelines, and capacity have drawn orders from shipowners worldwide.

Chinese shipyards are building the future of global crude transport at an unprecedented pace.

While some analysts debate whether the recent rate rally has “legs,” the sheer volume of new orders — combined with an aging global fleet (with significant portions of VLCCs and Suezmaxes over 15 years old) — points to a market that needs modern tonnage to replace retiring vessels and meet ongoing trade requirements.

The number of tankers on order is the largest ordered in history.

One topic not often discussed is the Dark Fleet and the New Tanker ratio. We will be looking into this in future articles as the Dark Fleet will be realigned with new trading blocs that Stu Turley has been discussing on the Energy News Beat podcast.

U.S. Energy Dominance on full display through exports

As Stu Turley on the Energy News Beat Podcast frequently emphasizes: “Energy Security starts at home, and your Energy Dominance is displayed through your exports.”The United States continues to export record volumes of oil and gas products, reinforcing its position as a global energy superpower. This export strength creates sustained demand for VLCCs and other tankers to move U.S. crude and refined products to markets worldwide — a dynamic that Chinese shipping companies like CMES are well-positioned to serve alongside their own strategic needs.

Strategic Petroleum Reserves (SPR) expansion creates new opportunities

Geopolitical tensions and supply disruptions have triggered a global race to build and expand strategic oil and gas storage. China holds the world’s largest strategic inventories (approaching or exceeding 1.3–1.4 billion barrels when including commercial stockpiles) and continues aggressive additions into 2026. The U.S. SPR stands at roughly 400+ million barrels with ongoing management and replenishment activity. Other nations — including Japan, India, Australia, Pakistan, and Singapore — are actively expanding or planning new storage capacity.

Strategic storage facilities like the U.S. SPR represent critical infrastructure for national energy security.

Where should long-term investors look for SPR-related opportunities?

Direct investment in government SPRs is limited, but private-sector plays abound in the supporting infrastructure:

- Engineering, procurement, and construction (EPC) firms specializing in large-scale tank farms, underground storage, and terminals.

- Midstream and storage operators that benefit from increased commercial and strategic stockpiling.

- Companies involved in floating storage solutions and specialized terminals.

- Infrastructure funds focused on energy security assets in high-growth regions (Asia, the Middle East, and emerging markets).

U.S. Midstream: A massive long-term opportunity

Yes — U.S. midstream companies represent one of the most compelling investment themes in energy today. With robust domestic production, surging LNG export capacity (projected to rise significantly through 2026 and beyond), and growing power demand (including from AI/data centers), midstream assets are enjoying strong, fee-based cash flows.

Key tailwinds include:

- Pipeline and gathering system expansions

- Export terminal growth along the Gulf Coast

- NGL and natural gas infrastructure buildout

- M&A consolidation is creating larger, more efficient platforms

Major publicly traded names frequently cited in this space include Enterprise Products Partners (EPD), Energy Transfer (ET), Kinder Morgan (KMI), MPLX, and Cheniere Energy (LNG) for its pure-play LNG export leadership. These companies typically offer attractive yields, distribution growth, and defensive characteristics tied to contracted volumes rather than commodity price swings.

The Bottom Line

China Merchants’ continued investment in VLCCs is not a short-term bet — it is a calculated, long-horizon wager on the enduring role of oil in global trade and energy security. Paired with record tanker ordering (heavily concentrated in China), expanding SPR programs worldwide, and America’s export-driven energy dominance, the transportation and storage segments of the energy value chain look structurally attractive for patient capital.

Energy security truly does start at home — and is amplified through exports, reliable infrastructure, and strategic storage. The companies and nations positioning themselves today are laying the groundwork for the decades ahead.

Appendix: Sources

- Lloyd’s List: “China Merchants stays bullish on VLCCs as market debates whether rally has legs” (July 2026) — https://www.lloydslist.com/LL1157733/China-Merchants-stays-bullish-on-VLCCs-as-market-debates-whether-rally-has-legs

- Lloyd’s List: “China Merchants boosts tanker fleet with $930m newbuild spree” — https://www.lloydslist.com/LL1150257/China-Merchants-boosts-tanker-fleet-with-$930m-newbuild-spree

- S&P Global: “China Merchants Energy Shipping sees robust VLCC market through 2026-28” (Dec 2025) — https://www.spglobal.com/energy/en/news-research/latest-news/chemicals/121025-china-merchants-energy-shipping-sees-robust-vlcc-market-through-2026-28

- Splash 247: “VLCC orderbook hits record high” (June 2026) — https://splash247.com/vlcc-orderbook-hits-record-high/

- Global Times / Hellenic Shipping News: China secures over 90% of global new VLCC orders (May 2026)

- EIA: “China, the United States, and Japan hold most strategic oil inventories in 2025” (April 2026) — https://www.eia.gov/todayinenergy/detail.php?id=67504

- Reuters: “Iran war triggers global race to build oil reserves” (June 2026)

- Various reports on U.S. midstream outlook from Deloitte, PwC, and industry analyses (2025–2026)

Energy News Beat Channel – Bringing clarity to the energy transition and traditional markets.