Authored by Peter Tchir via Academy Securities,

This seemed like one of the longest “short” weeks that I can remember. Maybe it was the Tuesday holiday. Maybe it was because I started the week somewhat jaded (What a “Weird” Week). Maybe it was because the jobs data also forced me to invoke the word “weird” repeatedly (Jobs – What You See Isn’t What You Get?). The fact that my air conditioning unit struggled to keep up with the heat and humidity definitely didn’t help, but neither did watching algo-driven markets (or having to wait until the last hour of trading for stocks to fade). However, I did enjoy catching up with some colleagues on Bloomberg’s Real Yield and talking about credit.

But enough on that right now, let’s focus on the matter at hand – the battle for resources and chips.

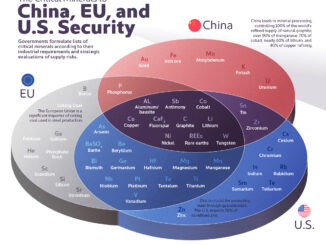

The week started with China imposing export restrictions on crucial raw materials. Gallium and germanium now require special permission from the government to be exported. These “rare elements” are crucial in the manufacturing of high-end chips.

The week ended with the Defense Department invoking the Defense Production Act to help collect and (even more crucially) refine the materials in question (Reuters story).

We have been discussing this theme on many fronts at Academy Securities. Our basic premise has been:

China figured out several years ago that rare earths and critical minerals (both their extraction and their processing) would shape the future of global trade and relationships. If the past few decades were shaped by petroleum products, the future will be shaped by these rare earths and critical minerals. We have argued that Russia and India seemed to figure this out a year or so ago (after China) and the U.S. is only recently reacting with the urgency necessary.

While sad to say, a tagline that we have been using for two years (or more) is that:

The West has a great vision for sustainability, but no plan to get there.

China has no vision for sustainability, but a great plan to attain the resources that they think we might need.

Yes, Yellen is in China (and Blinken was also there recently), but I don’t think that we will see any real thawing of tensions regarding the semiconductor industry or rare earths and critical minerals.

The cynical side of me expects that China will “throw us a bone” that we will happily gnaw on while they continue to secure the access to and the production of these resources.

Over two years ago, we published a special SITREP on the topic (Rare Earths – A National Security and Environmental Threat). Generals (ret.) Chinn, Robeson, Kearney, Marks, and Walsh all weighed in on the subject. Michael Rodriguez (Head of ESG) also brought up several salient points which helped form our macro outlook. We will update and refine this outlook in the coming weeks, but this is a great primer and it is (somewhat sadly) easy to see how we got from where we were two years ago to where we are today.

In February of this year, we “upped the ante” with World War v3.1. While rare earths and critical minerals were a part of that discussion, the main section worth reviewing is “The Semiconductor Industry Viewed Through a Geopolitical Lens”.

I would put Academy’s track record on predicting the path of U.S./China relations up against anyone’s. The geopolitical insights and experience of the Geopolitical Intelligence Group have been crucial in staying a step ahead of many. However, I do lament that by the time the consensus view catches up with

Academy’s view, the relationship with China will likely have deteriorated further. Unfortunately, that seems to be occurring again as chips, rare earths, and critical minerals are without a doubt a national security issue with strong bipartisan support.

The February 2021 and February 2023 reports, while dated, are great starting points and worth reviewing even by those who have already been focused this subject.

While we will be following up more on chips, rare earths, and critical minerals, this also seems like a good time to highlight our From Made in China to Made by China theme. If there is one risk that I think is real (and the market is completely discounting) it is the ongoing shift of China going from making our products to making/selling their own products. That goes hand in hand with their increasing success at getting some level of trading to occur directly in yuan instead of dollars. For those of you who have listened to our calls or watched our webinars, you know that we are not doubting the dollar as the reserve currency, but do see the dollar as the “world wide web” and the yuan as the “dark web”. The scale sounds about right, but maybe it attributes too many negative connotations to trade using the yuan (or maybe not enough depending on your view).

Artificial intelligence is the hottest topic helping markets (rightfully so in many ways).

The chip and commodity wars arguably are not getting enough attention.

My view of this is:

Competing with China will be inflationary as we need to secure access to these resources (some of it domestically) and build out processing facilities (domestically or with countries we completely trust).

Jobs will be created as part of the process of securing our supply chains, but it will take time, money, and likely the ability to absorb some inflation.

Whatever relationship you “hope” that we will return to with China is unlikely to occur. Considering AI, quantum computing, and sustainability (to name a few issues), the stakes are too high and the powers that be in both countries know this and will thwart each other’s attempts to gain the upper hand. It doesn’t mean that we can’t have trade, but whatever relationship we are going to have with China will be something new that is yet to be defined and will be crucial for our economy, companies, and society.

Maybe for investors, these things will take years to play out and don’t change things much today. However, for companies, those that have gotten ahead of the curve are prospering (and there is still time to react for those that have not). The difficulties that we could face with China regarding chips, rare earths, and critical minerals may lead to some expensive and even seemingly conservative decisions, but those decisions will pay off in the long run.

Have a great Sunday, hopefully you are having good weather and I did briefly wonder why China was banning geraniums – such pretty flowers.

Loading…