QatarEnergy is preparing for a swift ramp-up of liquefied natural gas (LNG) production at its massive Ras Laffan Industrial City complex once safe shipping resumes through the Strait of Hormuz, according to people familiar with the matter.

The world’s largest LNG exporter aims to restore most of its export capacity within two months of the strait reopening. QatarEnergy has informed buyers that it expects to reach approximately 50% of capacity within one month after safe passage is restored, and roughly 80% within two months.

This development follows a US-Iran peace framework and ceasefire that includes mine clearance operations, paving the way for normalization of energy flows across the Gulf after months of disruption.

Background: Iranian Attacks and Production Halt

The restart comes after a turbulent period. In early March 2026, Iranian missile and drone strikes hit Qatar’s Ras Laffan Industrial City, causing extensive damage to LNG infrastructure. Iranian attacks damaged two of Qatar’s 14 LNG trains and one gas-to-liquids (GTL) facility.

This knocked out 17% of Qatar’s LNG export capacity — equivalent to about 12.8 million tons per year (mtpa) of LNG. QatarEnergy CEO Saad al-Kaabi stated that repairs to the damaged LNG trains could take three to five years, while the GTL facility might be back online sooner (up to one year).

Qatar normally accounts for nearly 20% of global LNG supply. Production was fully halted, and force majeure was declared on LNG shipments and long-term contracts due to both the physical damage and the closure/blockade of the Strait of Hormuz, through which Qatari exports must pass.

The “20%” context: The user’s reference to the “20% that still needs repair” likely points to Qatar’s overall share of global LNG supply. Within that, roughly 17% of Qatar’s own capacity (or about 3–4% of global LNG) suffered direct damage requiring multi-year repairs. The remaining ~83% of Qatar’s operable capacity can now ramp up relatively quickly once shipping routes are secure.

Impact on the Damaged Portion: The rapid restart applies primarily to the undamaged trains. The 12.8 mtpa of damaged capacity will remain offline for years, creating a structural shortfall in Qatari supply that could persist into the early 2030s. This has already led to an estimated $20 billion in annual lost revenue for Qatar and forced delays or pauses in parts of the ambitious North Field expansion projects.

Buyers in Europe (e.g., Italy’s Edison, Belgium’s EDFT) and Asia (South Korea’s KOGAS, China via Shell) have been directly affected by the force majeure declarations tied to the damaged trains.

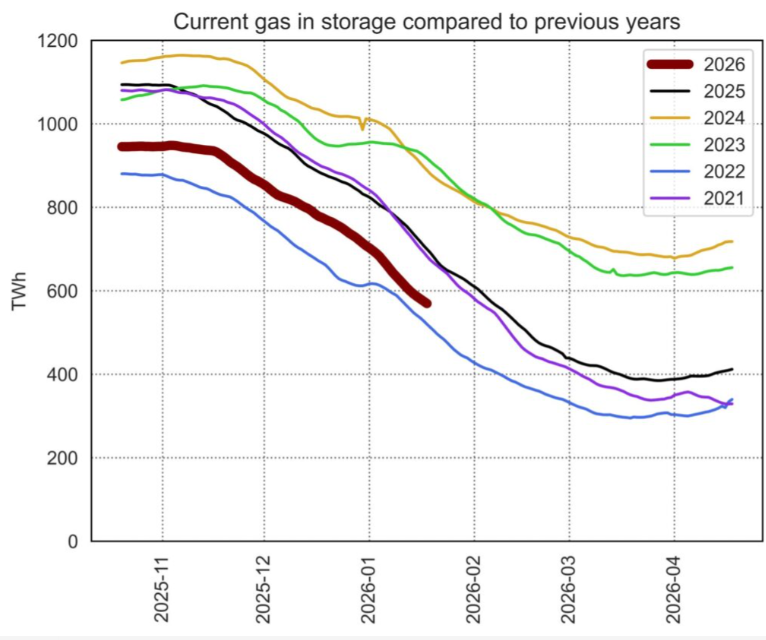

Will Europe Fill Its Natural Gas Supplies This Summer?

Europe enters the critical summer injection season with storage levels significantly below normal — around 28–37% full in recent assessments, compared to a typical 50% seasonal benchmark.

EU officials and the Gas Coordination Group have indicated that reaching 80% storage fill by the end of summer remains achievable if market conditions stabilize, which would provide reasonable security for the 2026/27 winter.

Qatar’s partial restart helps, but its direct role for Europe is limited:

Qatar typically supplies only about 8% of EU LNG imports (or roughly 4% of total EU gas imports in recent years).

The bigger benefit is global market relief. More Qatari LNG cargoes entering the market will ease competition for spot cargoes from the US, Australia, and other suppliers, potentially moderating prices and improving availability for European buyers.

Europe will still need to source the equivalent of hundreds of extra LNG cargoes this summer compared to normal years to meet storage targets. Lower global tightness from Qatari supply recovery should make this more feasible than during the peak disruption period, when prices spiked sharply (up 40–65% in Europe and Asia at times).

How Will Global LNG Markets Be Impacted?

Short-term (next 1–3 months): Positive. The return of significant Qatari volumes (potentially ramping toward 80% of operable capacity) will add meaningful supply to a market that lost nearly 20% of global LNG exports for months. This should help ease spot price pressure, support storage injections in Europe and Asia, and reduce volatility.

Medium- to long-term: More mixed/negative for supply balance. The permanent loss of ~12.8 mtpa from Qatar for 3–5 years represents a notable structural gap. Qatar was also in the midst of major expansions (targeting 126–142 mtpa overall), some of which face delays.

This benefits competing exporters, particularly the United States, which has been ramping up flexible LNG supply. Global buyers may accelerate diversification away from Middle East dependence. Prices could remain structurally higher than pre-crisis forecasts until new capacity elsewhere comes online or repairs are completed.

Shipping through the Strait of Hormuz is the immediate bottleneck being resolved. Once tankers can move freely again, the market should see a noticeable supply wave from Qatar in the coming weeks and months.

Outlook and Sources

Qatar’s ability to ramp production quickly on its undamaged infrastructure is a testament to the resilience of its operations, but the long repair timeline for the damaged 17% of capacity underscores the lasting scars from the conflict.

For Europe, the summer refill will be challenging but more manageable with improving global supply. Global LNG markets should see short-term stabilization followed by a tighter structural balance for several years.

- Bloomberg: “Qatar Plans to Rapidly Restart LNG Production After Hormuz Opens” (June 16, 2026) — https://www.bloomberg.com/news/articles/2026-06-16/qatar-plans-to-rapidly-restart-lng-production-after-hormuz-opens

bloomberg.com

- Reuters: “Iran attacks wipe out 17% of Qatar’s LNG capacity for up to five years” (March 19–20, 2026) — https://www.reuters.com/business/energy/iran-attack-damage-wipes-out-17-qatars-lng-capacity-three-five-years-qatarenergy-2026-03-19/

reuters.com

- Additional reporting from Oilprice.com, Bruegel, Wood Mackenzie, and ACER on European storage and market impacts (2026).

This situation remains fluid as mine clearance and full normalization of Hormuz transit continue. Energy News Beat Channel will monitor developments closely.