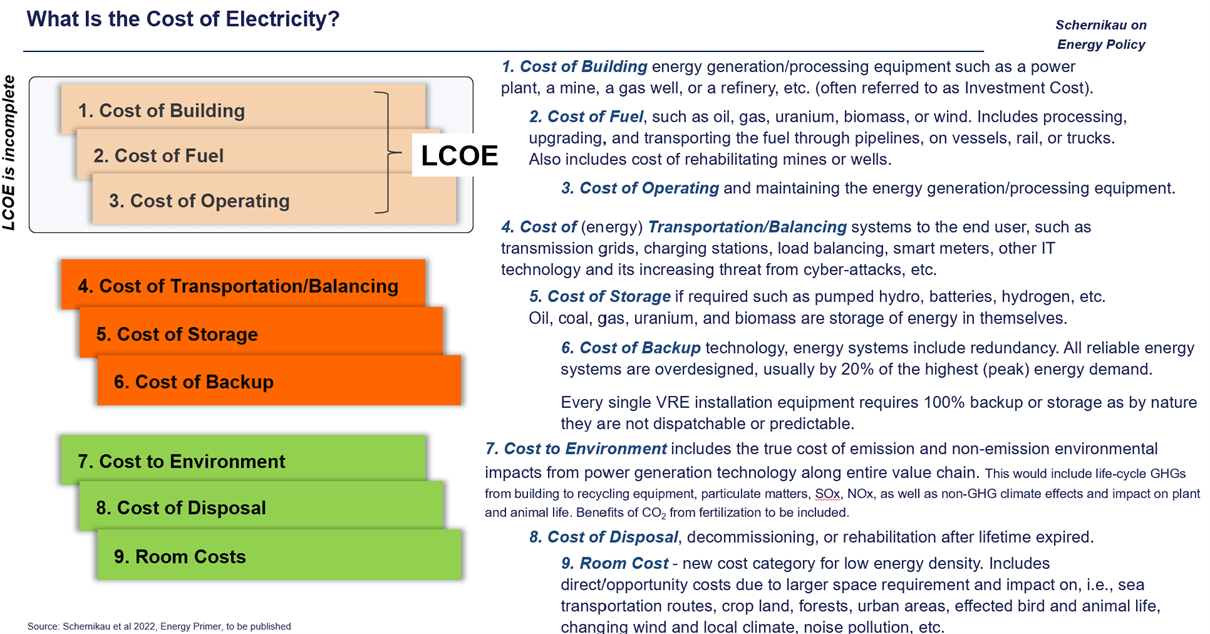

The standard Levelized Cost of Energy (LCOE) has dominated energy policy discussions for years. Policymakers, media, and even some industry reports cite it to claim that wind and solar are now the “cheapest” forms of new electricity generation. But as Germany’s Energiewende and certain U.S. states demonstrate, this metric is dangerously incomplete. It ignores the full system costs of integrating variable renewable energy (VRE) — balancing, backup, grid upgrades, storage, overbuilding, curtailment, and reduced capacity value. Two recent pieces from The Unpopular Truth series lay this out clearly: the April 25, 2026, article “Rethinking the cost of electricity” and the related Substack discussion on the unpopular truth about energy. They argue for shifting to a Full Cost of Electricity (FCOE) or Levelized Full System Cost of Electricity (LFSCOE) framework. These metrics capture the real cost to society and the grid.

OECD and UNECE reports back this up: higher VRE shares always increase system costs through balancing, network upgrades, and the need for reliable backup.

Lazard’s own LCOE+ analysis now includes “firming” costs (storage or peakers) and shows that while standalone wind and solar look cheap, unsubsidized, adding reliability drives costs up significantly.

Germany’s Energiewende: A Cautionary Tale of Overbuild and Hidden Costs

Germany leads Europe in wind and solar deployment. By the end of 2025, it had roughly 68 GW of wind (onshore + offshore) and over 116 GW of solar (DC). Renewables generated ~56% of public electricity in 2025. Yet household electricity prices remain among Europe’s highest, and wholesale prices stay volatile with growing negative-price hours and curtailment.

Dr. Schernikau’s simplified 2026 model for Germany (conservatively adding just €75/MWh in system costs and adjusting for power-price capture rates) shows solar at ~€374/MWh full-system equivalent — roughly three times the cost of domestic lignite. Wind follows closely behind. Even without full FCOE adjustments (overbuild, decommissioning, eROI, etc.), VRE costs rise with penetration because each new turbine or panel delivers less reliable energy.

Germany’s installed wind + solar capacity already exceeds peak demand by ~2.5× in many hours. Curtailment surged again in 2025 (solar curtailment nearly doubled year-over-year in some regions like Bavaria), costing hundreds of millions in compensation while grid upgrades lag.

Dr. Lars Schernikau has been a guest on the Energy News Beat Podcast, and his work is exemplary. Figure 11 hits home in the United States. We have an $89 Billion dollar liabilty that is a starting point for the wind farms for land reclamation, and I cannot find one that has been funded. There are currently an estimated 75,727 wind turbines on the US grid, and they are going to start failing as soon as the subsidies run out.

The question has to be asked: how many times were “Name Plate Upgrades” used instead of repairs, and how much additional funding was used during the Obama and Biden era? That answer is tough to get, and on the few that I have found, it is a staggeringly hidden cost to consumers and the national debt.

The United States: Policy Choices Drive Price Divergence

The U.S. tells a similar story at the state level. In 2025, wind and solar hit record generation (17% utility-scale nationally, closer to 19% including small-scale solar), with Texas, California, and the Midwest leading.

Yet consumer prices reveal stark differences:

California (aggressive renewable mandates, high solar penetration): ~33.75 ¢/kWh residential (2026 data).

New York (similar clean-energy push, nuclear phase-outs in the past): ~27.07 ¢/kWh residential.

Texas (ERCOT market-driven, abundant wind + solar + natural gas backup): ~16.18 ¢/kWh residential — roughly half of California’s rate and below the national average.

Texas has massive nameplate capacity (~40 GW wind + growing solar exceeding 30 GW) but maintains lower prices because dispatchable gas provides firming, and the market rewards actual delivery during peak demand. California and New York face higher transmission/distribution costs, policy-driven overbuild, and lower effective capacity factors (ELCC for solar often 10-20% of nameplate; wind 15-30%).

Nameplate capacity is “overbought” across high-VRE regions. To deliver the same reliable gigawatt-hours as a gas or nuclear plant, operators must install 3–5× (or more) nameplate VRE capacity plus storage. Curtailment rises as penetration grows — exactly what Germany and parts of California and Texas are experiencing today.

Wind + Solar + Storage: The Path to Grid Resiliency?

Pairing wind and solar with storage improves complementarity (solar peaks during the day, wind often in the evening/night). Hybrids can cut some interconnection and firming costs by 10% or more versus standalone projects.

Lazard’s 2025 LCOE+ shows utility-scale solar + 4-hour storage at $50–131/MWh and onshore wind + storage at $44–123/MWh — still higher than many conventional options when full firming is required.

For true 24/7/365 resiliency (99.999% uptime demanded by data centers and industry), long-duration storage or overbuild becomes prohibitively expensive. Studies show system costs skyrocket as you approach 100% VRE without firm backup. Overbuilding + curtailment is often the cheapest way to handle variability, but it still inflates the effective cost per delivered kWh.

As Subsidies Fade, Will VRE Remain Competitive?

The U.S. Inflation Reduction Act (IRA) tax credits (PTC/ITC and successors) have driven the boom. Many are now phasing out faster than originally planned: residential credits expired end-2025, production/investment credits for new wind/solar projects face accelerated sunsets (construction deadlines tightening into 2026–2027).

Without subsidies, the true economics shift. Lazard notes renewables remain competitive on a standalone LCOE basis, but once firming/storage/grid costs enter the equation — and subsidies disappear — the gap narrows or reverses in many markets. Germany’s experience (high costs despite massive deployment) is the preview. Texas’s market-based approach shows that abundant gas backup keeps prices low even with a high VRE nameplate.

Conclusion: It’s Time for Honest Metrics

LCOE was useful for dispatchable plants. For a modern grid dominated by variable sources, it misleads policymakers and distorts investment. We must adopt FCOE or LFSCOE — metrics that include the full societal cost of reliable, resilient power. Germany’s painful lesson and the U.S. state-by-state price divergence prove the point: ignoring system costs raises consumer bills, risks blackouts, and slows industrial growth.

Throw in Behind-The-Meter growth, and you are going to see some significant changes. Looking at Texas alone, ERCOT has staggering numbers of energy applications for power plans for data centers, and they need to be built as close to the power source as possible to eliminate consumers paying for the transmission lines.

Energy News Beat will continue tracking the real numbers. Affordable, reliable electricity isn’t optional — it’s the foundation of modern society. Let’s measure it correctly.

Check out the Energy News Beat Substack for additional information. https://theenergynewsbeat.substack.com/p/it-is-time-to-redefine-the-levelized

Appendix: Sources and Links

- Dr. Lars Schernikau, “Rethinking the cost of electricity,” The Unpopular Truth, April 25, 2026: https://unpopular-truth.com/2026/04/25/rethinking-the-cost-of-electricity/

- Energy News Beat Substack discussion on the unpopular truth about energy: https://theenergynewsbeat.substack.com/p/the-unpopular-truth-about-energy

- Lazard’s Levelized Cost of Energy+ (LCOE+) 2025 Report (June 2025): https://www.lazard.com/media/uounhon4/lazards-lcoeplus-june-2025-_vf.pdf

- IRENA Renewable Power Generation Costs 2024 (published 2025).

- U.S. EIA Electric Power Monthly (February 2026 data on state retail prices).

- Fraunhofer ISE / Agora Energiewende / BNetzA reports on German generation, curtailment, and prices (2025 data).

- Schernikau et al., peer-reviewed FCOE paper (SSRN/Elsevier).

- Additional data: NREL, EPRI, and state ISO reports on ELCC, curtailment, and overbuild.

- The Unpopular Truth: https://a.co/d/02uhFMHZ

This article reflects independent analysis drawing on the cited sources and public data as of April 2026. Energy policy should prioritize truth-seeking over ideology.