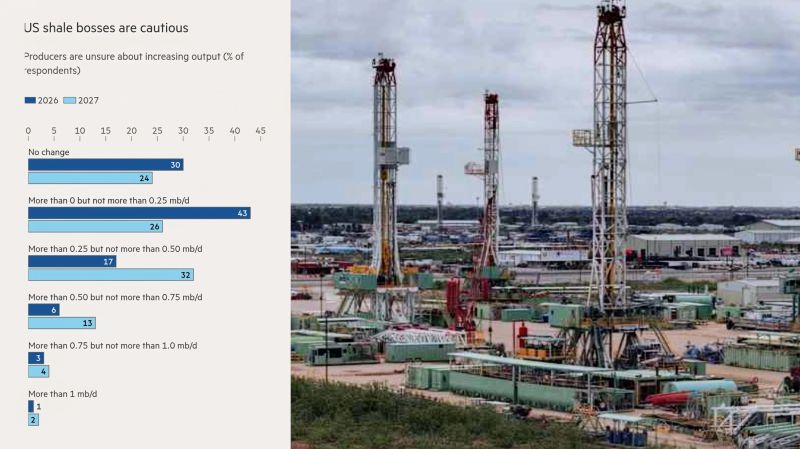

The FT writes, US shale bosses polled by the Federal Reserve Bank of Dallas said they did not expect to significantly increase production over the next two years as a result of the “chaos” caused by the Iran war.

According survey of more than 100 oil and gas companies, 43% of executives said they do not expect daily production to increase by more than 250,000 Bpd in 2026. For 2027, 32% of the executives said in the quarterly that they expected production to rise more than 250,000 b/d but not more than 500,000 b/d.

The survey reflects the apprehension in the US shale industry over quickly expanding production in response to the Iran war, despite attacks in the Gulf and the closure of the Strait of Hormuz hitting global energy supplies.

In additional comments published along with the survey, one executive said: “With all of the chaos, predicting anything in the energy sector is very difficult.”Another said that the difference between paper market prices and physical prices“ sends conflicting signals to operators who cannot plan rigs and capital budgets when prices swing wildly based on tweets”.

Most execs surveyed said they expect the Strait of Hormuz to return to normal levels by August 2026. About two-thirds of respondents said they expect 90% of trapped Gulf production to return to market eventually. While current crude prices have risen over $100 a barrel, prices for 2027 and 2028 remain below the threshold producers need to significantly increase output, analysts said.

“Most companies are taking a wait and see or do nothing approach to their 2026 budget,” Dan Pickering, founder of financial services firm Pickering Energy Partners.

Our Take 1: Notwithstanding the survey’s results, producer activity in the US responds more quickly than appreciated to prices that can be realized when new production actually comes on line. If that can be locked-in at a high enough price—for a long enough period of time—with financial hedges, the industry will hit the bait and future production be higher than expected. Count on it.

Our Take 2: That point matters because at some point the global storage draw—a half a billion barrels so far—that’s occurred since the Iran War is going to have to be refilled in advance of the refilling, putting pressure on futures prices father out on the curve. That will begin to induce more production outside of the Middle East, including in the US.

Our Take 3: That, and other market forces—and presumably an eventual resumption of transport in the Strait of Hormuz—will in time lead to a global production surplus of crude and greater long-term comfort with its diversified global supplies. That, in turn, will lead to lower prices and the return of demand growth. As always, the long game will be different than the short game.