ENB Pub Note: This is an outstanding article from Giacomo Prandelli’s Substack “The Merchants News”. He has been on the Energy News Beat Podcast, and we are looking to have him on again. He is a great author, and we recommend subscribing to his Substack. Lloyds of London appears to be the holdup now, and the Trump administration is not getting the solution or workaround implemented fast enough. The opening of Russian Sanctions on tankers that are on the water is a good temporary step, but Refineries around the globe are strained, and Ukraine attacking other EU countries is absolutely disgusting.

As of March 5, 2026, the Strait of Hormuz has basically stopped working as the world’s most important energy corridor.

After coordinated US and Israeli airstrikes on Iran on February 28th, Iranian Revolutionary Guard Corps senior official Ebrahim Jabari declared the strait closed, warning that any ship trying to get through would be set on fire.

Iran’s foreign minister has claimed there’s no plan to officially shut the waterway, but what’s actually happening tells a different story, tanker traffic has dropped 86% compared to the week before.

Multiple attacks have hit tankers trying to get through, with at least 5 vessels taking damage, people hurt, and one crew member confirmed dead on a tanker attacked near Omani waters. Major maritime insurers have started pulling war risk coverage for ships entering the Persian Gulf.

What about alternative routes? The numbers give a pretty bleak answer.

The Strait of Hormuz normally moves 18.6 million barrels per day(bpd), roughly 20% of global oil demand and 31% of all maritime crude shipments. Right now, exports have fallen to around 4 million bpd, with most of that being Iranian barrels since international tanker traffic has basically disappeared.

Here’s what the alternatives actually look like:

- Suez Canal: 4.6 million bpd capacity

- Bab al Mandab: 3.1 million bpd capacity

- East-West Pipeline (Saudi Arabia): limited capacity, land based

- Jask terminal (Iran): still not finished, not open

Even adding Suez and Bab al Mandab together only gets you 7.7 million barrels per day, 41% of what Hormuz normally moves. The other 59%, more than 10 million bpd, has nowhere to go. Saudi Arabia and the UAE have some pipeline capacity that skips Hormuz, but nowhere near enough to cover a long closure.

Every alternative has its own problems. Suez and Bab al Mandab are themselves choke points with security risks that have gotten worse since Houthi attacks began in 2023. Pipelines are fixed , you can’t reroute them or scale them up fast. Overland routes cost more, take longer, and drag in other countries’ politics. The Red Sea corridor is already sliding back into trouble as Houthi threats flare up again.

When Hormuz goes down, the global energy system doesn’t have a workaround. It has a chain of bottlenecks, each with limited capacity and its own risks. Actual resilience means understanding the math, planning for disruption, and accepting that some risks can’t be fully fixed but only managed.

So, Who Really Depends on the Strait of Hormuz?

Asia takes almost all of Hormuz oil flows, so any disruption hits Asian energy security first and hardest. China has the biggest single exposure, importing roughly 3.8 million bpd through the strait, more than 30% of its total oil imports. India is next at around 2 million bpd, Japan at roughly 1.7 million, and South Korea at about 1.6 million.

For LNG, the picture looks the same. Of the 82.3 million tonnes of LNG shipped through the Strait of Hormuz every year, more than 80% goes to Asian countries, with China and India buying the most. Qatar, the world’s 2nd largest LNG exporter at about 20% of global LNG exports, has to send everything through Hormuz to reach international markets. After Iranian drone attacks on Qatar’s Laffan Industrial City and Mesaieed Industrial City, Qatar, a major LNG supplier, shut down production.

The Strategic Reserve Reality

Every country in Asia is running the same clock right now.

They just have very different numbers.

Japan has 254 days of oil reserves, the most prepared country on earth. They built those reserves after getting cut off in 1973, a humiliation so bad they spent the next 50 years making sure it could never happen again. Refiners are already asking to open them. The government has said not yet.

China’s reserve situation points to a critical strategic bet made throughout 2025. Official reserve data is a state secret, but analysts think China holds between 900 million and 1.5 billion barrels in strategic and commercial stockpiles, enough to cover between 104 and 200 days of imports depending on who you ask.

More importantly, China was buying aggressively throughout 2025, averaging around 530,000 to 1 million bpd while prices were hovering near $60. By December 2025, China’s onshore crude inventories hit a record high of 1.206 billion barrels.

This wasn’t random, China built a massive crude buffer in 2025, taking advantage of lower prices and setting itself up for exactly this kind of scenario. Energy security is the main driver for China’s stockpiling amid escalating geopolitical tensions.

India has cut gas to industry by 10 to 30%, not projected cuts, but actual cuts happening right now. The country has enough crude and refined fuel inventory to cover about 74 days of demand, though refining sector sources say current stocks could realistically last around 20 to 25 days.

South Korea imports 1.6 million bpd through Hormuz. That pipeline is now dry. The country has enough reserves for several months, but only if the disruption is short lived.

Japan has 3 weeks of LNG inventories. More than 90% of Japan’s imported crude comes from the Middle East, with a big share going through Hormuz. Japanese shipping giant Mitsui OSK Lines has stopped sending ships through.

Pakistan has no strategic reserve. Bangladesh has no strategic reserve. No buffer. No fallback. No plan B.

This is how the cascade works. When analysts say Asia is facing disruption, they’re averaging 254 days of Japanese preparedness against 0 days of Pakistani preparedness and calling it a regional crisis of moderate concern. That’s clearly multiple different crises hitting at different speeds, all at the same time.

The countries with reserves will start using them one by one, each release sending a price signal that speeds up the clock for the countries below them on the ladder. Japan releases, prices drop for a bit, then the release ends and prices go back up. South Korea releases, same thing. Then India. Then nobody has a buffer left and the war is still going.

Japan built 254 days of reserves because of what happened in 1973. On day seven of this war, they’re already being asked to open them.

The China Question, Did They Know Something?

China’s 2025 buying campaign now looks like strategic foresight rather than good timing. Throughout 2025, China imported a record 557.73 million tons of crude oil, averaging 11.55 million bpd, up 4.4% from the year before. December 2025 alone saw crude imports jump 17% compared to the previous year, with daily import volumes reaching levels nobody had seen before.

All this buying happened even as domestic demand growth was slowing, basically propping up oil prices throughout 2025 even while China’s economy was using less. Beijing took advantage of lower international prices and even steeper discounts on sanctioned supply from Iran, Venezuela, and Russia. China’s average crude cost was $10 per barrel cheaper than in 2024 because of sanctions discounts.

More tellingly, China’s teapot refineries, small independent refineries concentrated in Shandong province, became the dominant buyers of Iranian crude. These privately owned refineries handled 77% of Iran’s 1.6 million barrels per day of exports in 2024, attracted by heavy discounts and operating through a web of shell companies and a “dark fleet” of tankers.

By February 2026, Tehran started loading oil tankers faster than it had in years, sensing that revenues might drop as Washington stepped up its military presence. Another 42 million barrels of Iranian crude was sitting on tankers in Asia by late January. China now has access to this floating storage, 191 million barrels total, with roughly 127 million barrels currently in the East, including the Malacca Strait, Singapore Strait, South China Sea, East China Sea, and Yellow Sea.

Iranian attacks on commercial ships have also blocked Iran’s own deliveries to China, its only real customer. But China put itself in a good position. It has almost 3 months of room between national reserves and commercial refinery stocks. It has 191 million barrels of Iranian and Russian crude sitting in floating storage, most of it far from the Strait of Hormuz and close to Chinese ports. And it has good reasons to push for more Russian crude through existing pipelines.

Did China know something?

The timing, aggressive buying throughout 2025 at low prices, mandates to state-owned companies, record storage construction, then a conflict erupting in late February 2026 that closes Hormuz, looks a lot more like a plan than a coincidence.

The Geopolitical Complication

The supply picture gets even messier when you factor in sanctions and crisis management. In October 2025, the US Treasury sanctioned Russia’s 2 largest oil companies (Rosneft and Lukoil) going after the energy revenue that funds the Kremlin’s war. These sanctions forced Indian refiners, who had become major buyers of discounted Russian crude, to scramble for other sources.

India’s Russian oil imports dropped by nearly a 1/3 after the sanctions hit, with companies like Reliance Industries, HPCL, HPCL Mittal Energy, and Mangalore Refinery halting purchases. The only holdout was Rosneft-backed Nayara Energy, which stayed heavily dependent on Russian crude after EU sanctions effectively cut it off from everywhere else.

Then Hormuz blew up. On March 5, 2026 ,1 week into the strait’s effective closure the US Treasury issued a temporary 30-day waiver letting Indian refineries buy millions of barrels of Russian crude already loaded on tankers as of March 5, with deliveries allowed through April 4, 2026. Treasury Secretary Scott Bessent framed it around President Trump’s energy agenda, saying the waiver would “enable oil to keep flowing into the global market”.

This is a massive win for Putin. The timing says everything, months of pressure to cut off Russian oil purchases, then an immediate turn the moment Middle Eastern supplies disappear. The waiver covers all oil already loaded on tankers by March 5 essentially giving a green light to purchases that would otherwise break sanctions.

For India, it’s temporary relief. For Russia, it’s proof the revenue stream still works. For the global oil market, it shows that energy security beats sanctions policy when supply actually gets tight. The real question is what happens on April 4 when the waiver expires and Hormuz might still be closed?

Why Iranian Crude Can’t Be Replaced?

Everyone talks about Iranian oil in barrels. Nobody talks about what’s actually inside them. That difference is why Western refineries have been running shadow networks through Dubai for many years to get it, even through sanctions.

Crude oil isn’t one thing. It’s a range of hydrocarbons with different molecular weights, and the mix determines how easily it turns into the products refineries actually want to sell: gasoline, diesel, jet fuel, heating oil. The number that captures this is API gravity. Higher API gravity means lighter crude with shorter carbon chains cheaper to crack, cheaper to refine, and better at producing the lighter end products that sell for more.

Iranian Light crude comes in at 33 to 36 degrees API gravity with sulfur content between 1.36 and 1.5 percent. That’s the refinery sweet spot. Light enough to produce high fractions of gasoline and middle distillates without huge processing costs, but heavy enough to give the full range of products that complex refineries are built to handle. Petroleum engineers call it an optimal blend crude.

Venezuelan Merey heavy crude sits at roughly 16 degrees API gravity. Refining it profitably needs a coking unit, a hydrocracker, and serious desulfurization equipment. The economics work for refineries built specifically around Venezuelan feedstock. But it’s not a substitute for Iranian crude. It’s a completely different product that needs different industrial infrastructure. Venezuela’s main crude sits at the wrong end of the quality spectrum, global benchmarks like WTI and Brent are light, flexible barrels that work in most refineries with minimal processing.

US West Texas Intermediate runs at 40 degrees API, it’s so light that it doesn’t produce the heavier middle distillates a complex refinery needs to run at full capacity. European and Asian refineries built around medium crudes can’t just switch to WTI without blending it with heavier crudes to get the right molecular mix for their equipment.

Iranian oil fits where both US shale and Venezuelan heavy don’t. It’s the crude that moves through the middle of the global refining system without needing either the heavy end equipment for Venezuelan crude or the blending operations for ultra light shale. That’s why it consistently sells at a premium above comparable grades. It’s why Indian refineries kept buying Iranian/arab crude through every round of sanctions and worked out the logistics to keep that flow going. It’s why the Dubai shadow banking and trading network that the UAE is now thinking about shutting down existed in the first place.

The Strait of Hormuz doesn’t just carry oil..It carries the specific kind of oil the global refining system was built to run on. Closing it cuts supply and removes the grade of crude the system handles most efficiently and forces every refinery in the world to run less efficiently on whatever it can find instead.

That’s the premium baked into the current oil price.

How Long Can This Last?

I don’t have a crystal ball, but here’s what I see for oil prices and I want to give you what I think is the single most interesting and coherent investment idea that emerges directly from this crisis:

Oil markets are pricing in a supply shock that is very real. Brent is trading in the mid $80s and the direction of travel depends entirely on one variable, how long this lasts?

The base case is a short disruption, temporary inventory draws, prices fading back toward the mid-$60s by year end, is plausible. But the risk case is live and getting more serious by the day. Iraq has already shut in roughly 1.5 million bpd simply because storage is full and there’s nowhere to send the oil. Ras Tanura, one of the most critical oil facilities in the world, is reportedly offline. Infrastructure damage doesn’t reverse quickly, and that’s the part of this story the market may still be underpricing.

The world can absorb a 1 week shock. It cannot comfortably absorb a month. Every additional week compounds the damage reserve depletion, production shut ins, and a crude quality mismatch that can’t be solved by simply redirecting supply. Flooding the wrong refineries with the wrong grades is a real problem.

If disruptions extend beyond 3-4 weeks, $100 oil is the base case and if this drags into a 2nd month, the cascade through the system becomes very difficult to reverse quickly.

On day 7, Japan’s refiners are already requesting access to 254 days of strategic reserves built after 1973. That should be a wake up call for every energy desk in the world. The base case may still be orderly. The risk case is not.

I also find a company I see as uniquely and almost perfectly positioned to benefit from exactly this moment.

This is not as a speculative bet or a pre production story, but as a company already in motion with the infrastructure, the market access, and the margin profile to convert this geopolitical crisis into measurable, compounding cash flow.

That company is Vista Energy (VIST)

Here’s why:

The production story is already happening and accelerating

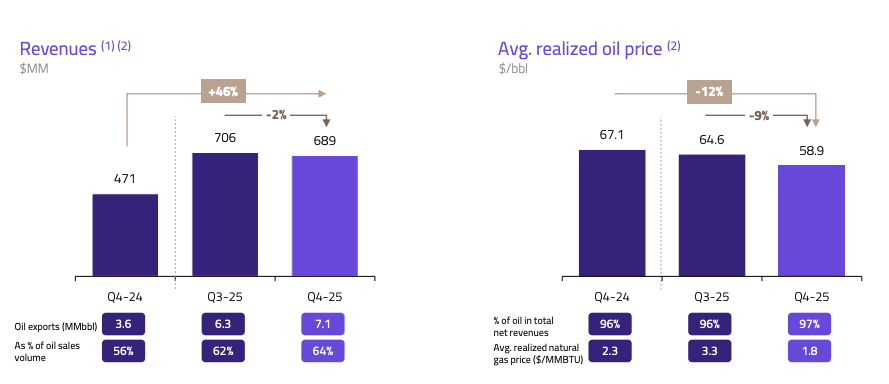

- Vista is producing 118,000 boe/d (q4 2025) and has committed $4.5 billion to reach 180,000 by 2028, 60% growth in 3 years, fully funded, already underway

- Critically, they are achieving this with fewer rigs than last year, down from 37 in 2024 to 30 in 2025 while production increased. That tells me that execution is improving, not deteriorating. Vaca Muerta wells are now outperforming comparable US shale plays including Eagle Ford and Bakken on a per-well productivity basis

- 70% of production is oil, which means the current price environment flows almost entirely to the bottom line. Every dollar Brent moves above their breakeven of $36-45 per barrel lands directly in free cash flow

The infrastructure problem is solved

- The VMOS pipeline is a 440 kilometer system connecting Vaca Muerta production directly to the Atlantic coast port of Punta Colorada. This single piece of infrastructure changes everything. Argentine oil previously sold at a $10-15 discount to Brent because of domestic logistics constraints and refinery capacity limits. With VMOS, that discount has collapsed to $3-5. That’s $7-10 per barrel recaptured structurally, permanently, not as a function of the current crisis

- Vista holds a 20% stake in VMOS alongside YPF, Pan American Energy, and Pampa Energía. That ownership gives them guaranteed export capacity as volumes scale, not just access to a shared queue. The company has been explicit: future Vaca Muerta production will be almost exclusively for export markets

- Pipeline capacity already reached 410,000 barrels per day by late 2025, up from 190,000 at launch in 2023. The ramp is real

Asian market access is proven, not theoretical

- The first Vaca Muerta cargo arrived in China in July 2025. Vessels departed from Bahía Blanca and arrived in Qingdao. The logistics work. The route is established. The question now is purely one of scale

- This matters enormously in the current environment. The teapot refineries that absorbed the vast majority of Iranian crude exports are now scrambling for alternative supply. These are independent Chinese refiners that lack the complex coking and desulfurization units required for heavy sour crudes, they need medium-sweet, low-sulfur barrels in the 30-40° API range. Vaca Muerta’s ultra-low sulfur content of 0.1-0.5% makes it a premium blending component even where the API grade isn’t a perfect match. These refiners can work with it, and right now they are motivated to find supply wherever it exists

- Vista’s management has explicitly identified Asia as the target market for incremental production, and the IMO 2020 low-sulfur regulations continue to structurally tighten demand for exactly the crude profile Vaca Muerta produces

The financial leverage to higher oil prices is significant

- At current Brent around $82, Vista is generating approximately $37-46 per barrel in margin above breakeven. If disruptions extend and Brent moves toward $100 which is not a tail scenario at this point, it is a live possibility that margin expands to $55-64 per barrel across a growing production base

- Revenue is projected to grow from $2.17 billion in 2025 to $3.8 billion by 2028, a 75% increase driven by production growth and export pricing. EBITDA is expected to grow from $1.6 billion to $2.8 billion over the same period. Free cash flow of approximately $1.5 billion per year between 2026 and 2028 funds the growth program while leaving room to return capital to shareholders

- The incremental math is straightforward: 46,000 barrels per day of additional oil production by 2028 at a conservative $40/barrel margin equals roughly $670 million in additional annual EBITDA from volume growth alone, before any price upside

The valuation gap is the structural opportunity

- Vista trades at roughly 4-5x 2026 estimated EBITDA and approximately 2.5-3x 2028 projected EBITDA. US shale peers trade at 5-6x. That discount exists because of Argentina country risk the legacy of capital controls, export taxes, and forced domestic sales that defined the Kirchner years

- That risk has materially diminished. President Milei’s administration has systematically eliminated export taxes on oil and gas, dismantled capital controls, and liberalized FX markets since December 2023. The policy environment has structurally changed, and the market has not fully repriced that change yet

- If Vista closes even half the valuation gap to US peers by 2028, the return is over 100% before accounting for any crisis premium. If it closes the full gap, the stock re rates from a $6-7 billion market cap to $14-16 billion

What could go wrong ?

- Hormuz resolves quickly and Iranian barrels flood back into Asian markets. The crisis premium evaporates. The base case still works at $66-70 Brent, but the urgency of the thesis fades

- Argentina reverts to interventionist policy. Export taxes and FX controls would directly impair the margin expansion story and the export premium Vista is counting on. This is the risk I watch most closely

- Crude quality forces discounts. Asian refiners under less pressure may resist paying up for lighter grades when they ideally want the heavier Iranian blend. The mismatch doesn’t kill the thesis but it could compress the premium

- China demand softens or Beijing releases strategic reserves aggressively, taking pressure off the market precisely when Argentine barrels are arriving in volume

- Execution slips on the $4.5 billion capital program. Delivering 60% production growth requires flawless drilling and infrastructure coordination. Any material delay pushes the cash flow realization timeline

The base case here does not require $100 oil. It does not require the Hormuz crisis to last another month. It requires Vista to keep doing what it is already doing growing production, moving oil through a pipeline that already works, selling into a market that is already buying at prices the market is already trading today, in a policy environment that has already changed. The crisis doesn’t build this investment case. It accelerates it, amplifies it, and puts a spotlight on a company that was already quietly becoming one of the most interesting energy growth stories outside of North America.

The downside is cushioned by a low entry valuation and an existing, cash generating production base. The upside is a company growing 60% in output, expanding margins structurally, and selling into the exact market that has the most acute supply problem in the world right now. That asymmetry is what makes it compelling to me.

Thank you for reading it!

We truly appreciate your interest in staying informed about the latest global trends and insights.

Please let us know if you liked it, what we can improve, and if you think this newsletter could help a friend, please send it to them!

Stay update and take care!

The Merchant’s News

GP

This piece is for informational purposes and reflects the author’s own analysis and views. It is not investment advice and does not constitute a solicitation to buy or sell any security. Investors should conduct independent due diligence and consult qualified advisers before making investment decisions. Past performance is not indicative of future results.

Get your CEO on the #1 Energy Podcast in the United States: https://energynewsbeat.co/energy-news-beat-media-kit/

Is oil and gas right for your portfolio? https://energynewsbeat.co/invest/

Be the first to comment