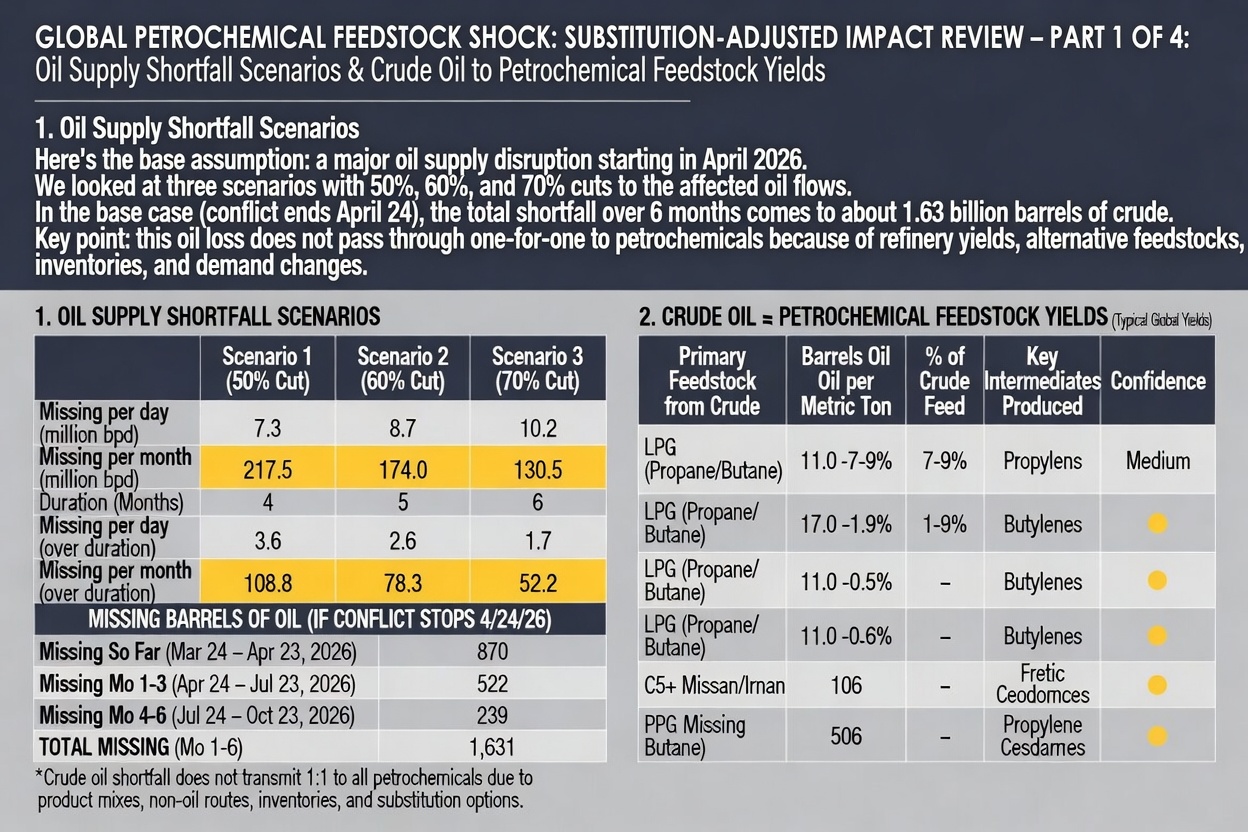

As the Strait of Hormuz remains effectively closed following the escalation of the U.S.-Israel-Iran conflict in late February 2026, the world is witnessing what energy experts are calling the largest supply shock in history. Traffic through the strait has plummeted by over 95%, choking off roughly 20% of global oil and LNG flows, along with critical petrochemical feedstocks, fertilizers, and related commodities.

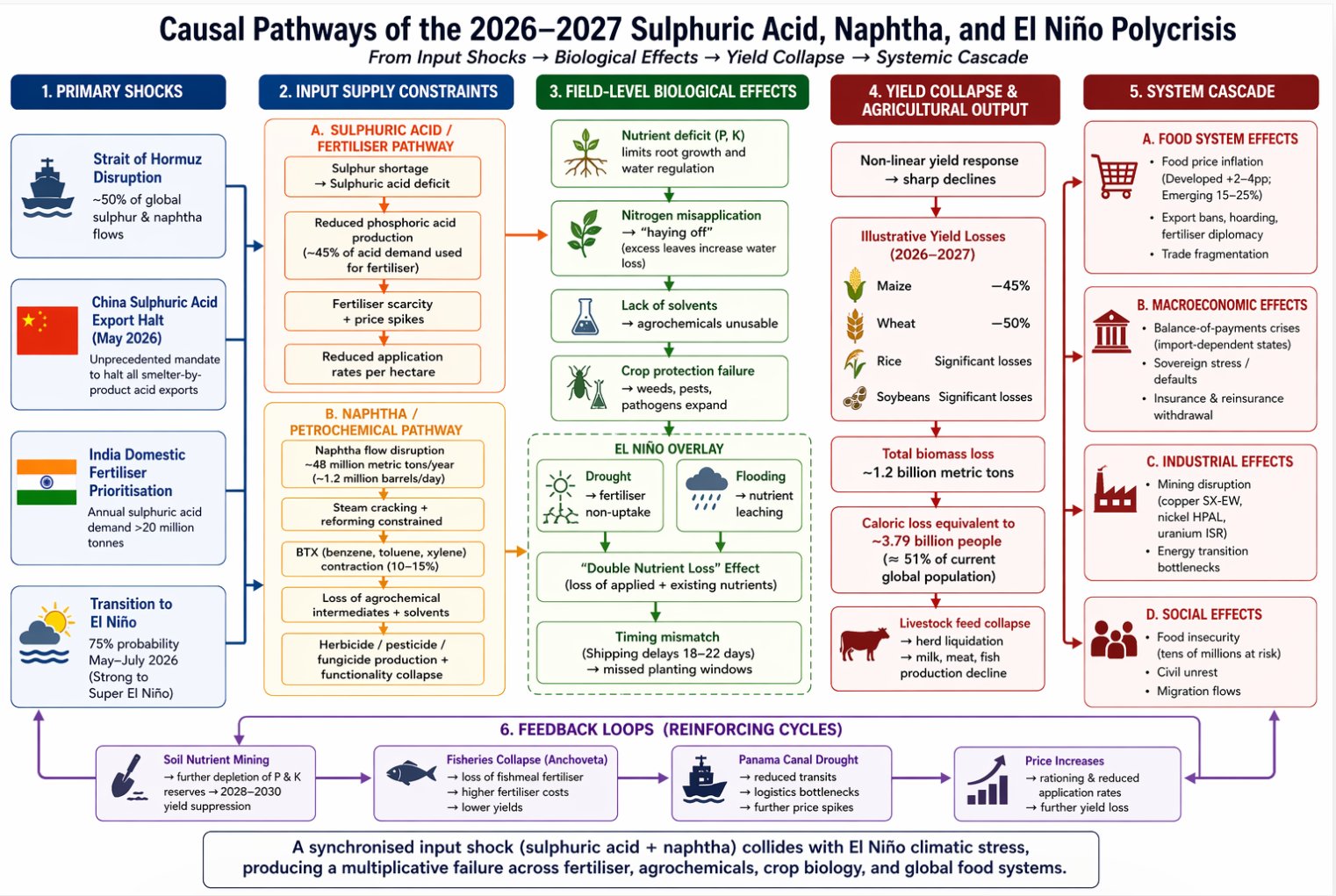

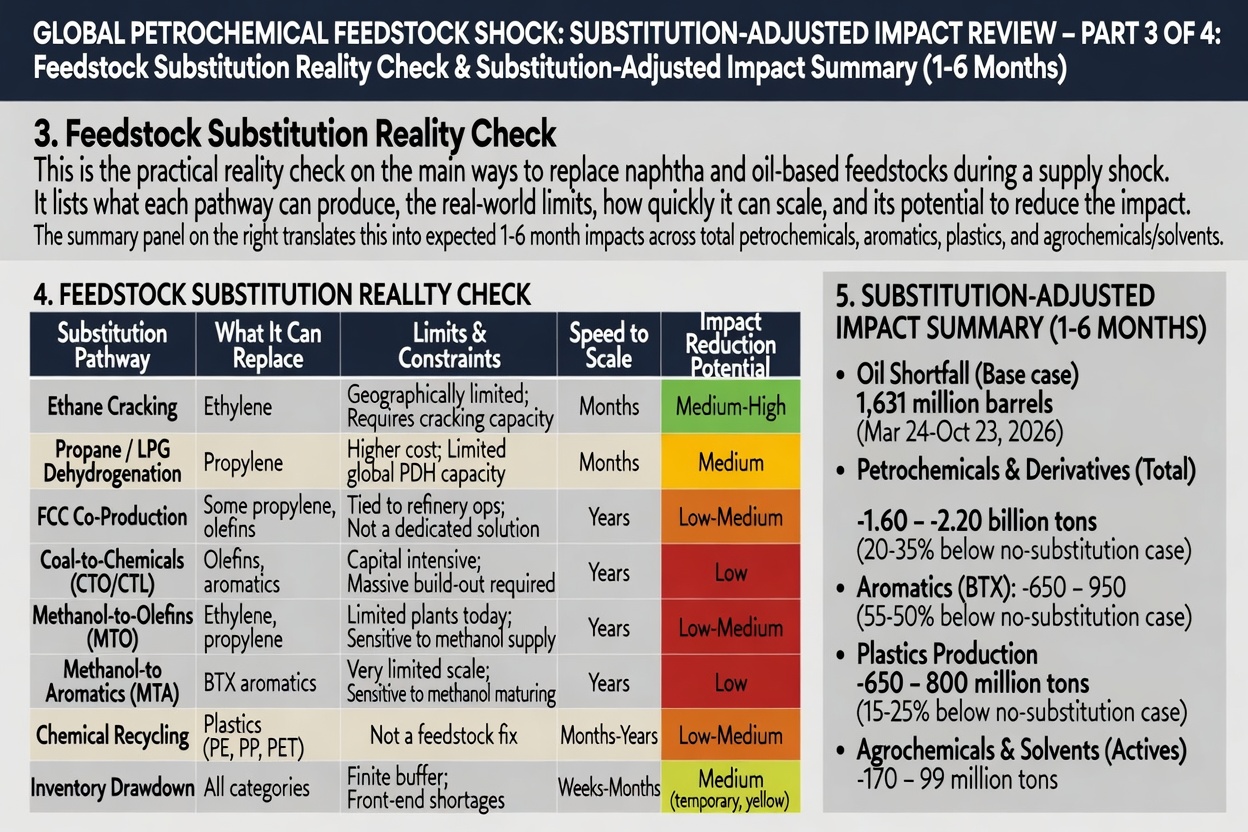

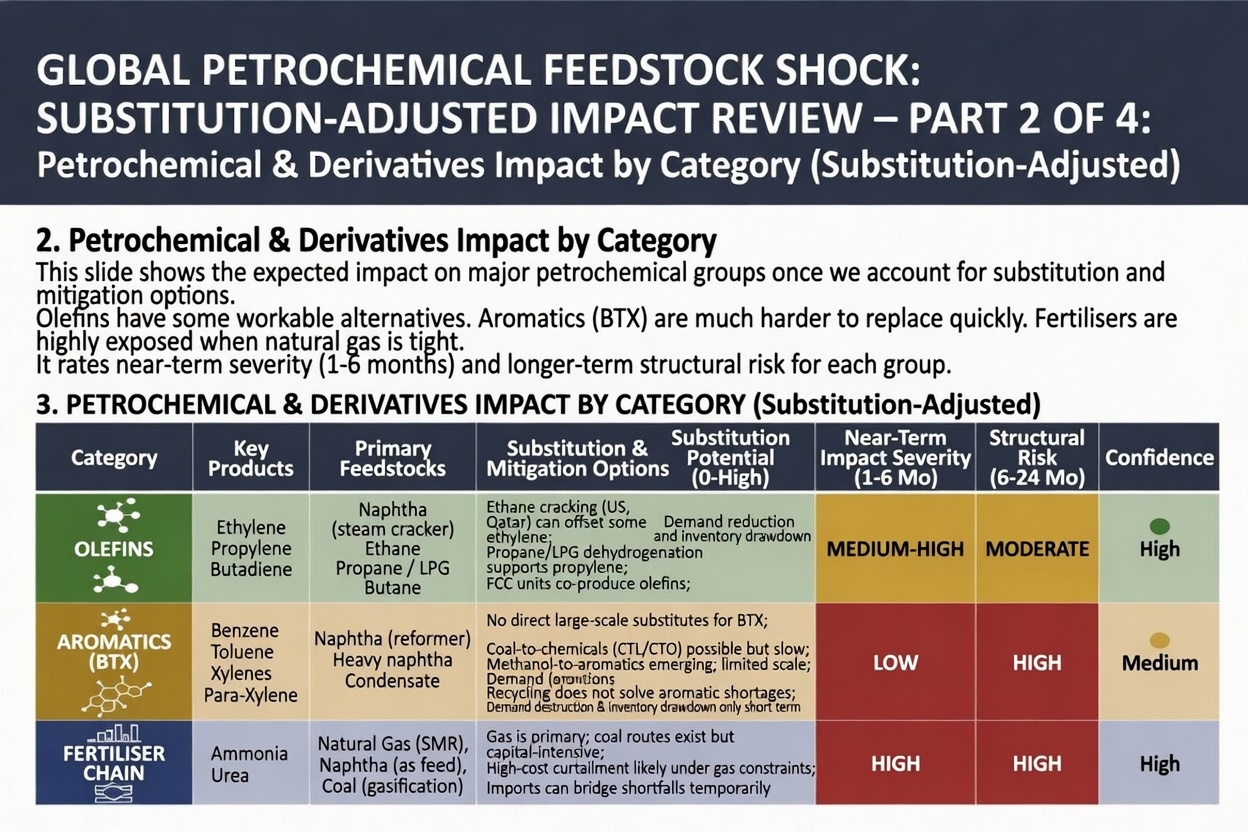

This is not merely an energy crisis—it is a petrochemical feedstocks shock rippling through global supply chains. As outlined in Craig Tindale’s powerful X thread (posted April 25, 2026), the disruption is triggering a “PolyCRISIS Framework 2026-27” that connects feedstock shortages to cascading effects in agriculture, manufacturing, finance, and beyond. Tindale’s slides detail the PetroChemical Feedstock Shock (Notional Adjust for Substitution), After Substitution Impact Review, Global Petrochemical Causal Pathway, Sulfur Acid to Fertilizer Shock, Naphtha/BTC Agrochemical Shock, and amplifiers like Super El Niño and misguided central-bank responses (including the Federal Reserve and RBA frameworks). He also highlights Tindale’s Trap—a $12.3 trillion blind spot accelerating de-industrialization in places like Australia.

The Scale of the Shock: Why This Is Different

The Strait of Hormuz normally carries about one-fifth of the world’s oil, a quarter of its LNG, and massive volumes of petrochemical precursors and fertilizers. Gulf producers account for ~46% of global seaborne urea trade, ~49-50% of sulfur (key for sulfuric acid and phosphate fertilizers), ~33% of methanol, and significant naphtha and LPG exports. With physical blockages, force majeure declarations, damaged infrastructure, and war-risk insurance withdrawals, substitution is limited and slow.

Even after notional adjustments for substitution (e.g., rerouting via alternative pipelines or sourcing from the U.S./Russia), the “After Substitution Impact Review” in Tindale’s framework shows severe net shortages. Plants are curtailing output across Asia, fertilizer inventories are plunging ahead of key planting windows, and petrochemical prices (polyethylene, polypropylene, MEG) have surged 30-40% in weeks.

This is the largest supply shock ever experienced in energy markets—no historical parallel matches the scale or duration of this physical disruption.

Impacts on Key Industries

Agriculture & Food Security

The Sulfur Acid-to-Fertilizer Shock and the Naphtha/BTC Agrochemical Shock are devastating. The Gulf supplies ~20-33% of global seaborne fertilizers (urea up to 46% of trade). Sulfur shortages cripple sulfuric acid production, essential for phosphate fertilizers and copper mining. Nitrogen fertilizers (ammonia/urea) rely on natural gas/LNG feedstock now stranded.

With Super El Niño amplifying weather stress on crops, global food prices are rising fast: wheat +4.2%, fruits/vegetables +5.2%, with worst-case spikes in vulnerable nations (Zambia +31%, Sri Lanka +15%, Pakistan +11%). Farmers in India (mid-July paddy window), Brazil, and China face skyrocketing input costs, threatening yields and profitability.

Petrochemicals, Plastics & Manufacturing

Naphtha and LPG feedstocks for ethylene, propylene, and plastics are in short supply. Asian crackers (Japan ~42% naphtha from ME, South Korea cutting runs by up to 50%) are shutting or slowing. Plastics, packaging, textiles, coatings, and resins—all derived from these—face shortages and price spikes. Downstream hits autos, electronics, pharma, and consumer goods.

Financial Markets & Broader Economy

Oil prices have surged (Brent well above $100/bbl at peaks), driving inflation. Central banks (Fed, RBA) risk amplifying the crisis by tightening policy against supply-driven inflation (Federal Reserve Amplification and RBA Framework in Tindale’s slides). Global GDP growth faces 0.2–1.3% hits depending on duration; recession risks are elevated. Stock markets have sold off; bond yields spiked. Tindale’s PolyCRISIS and Tindale’s Trap warn of de-industrialization in import-dependent economies like Australia.

Other sectors (aviation, shipping, metals) face higher fuel, freight, and input costs.

Regions Hurt the Most—and By What Products

Asia (Hardest Hit Overall): China, India, Japan, South Korea, Taiwan, and Southeast Asia rely heavily on Gulf naphtha/LPG (~35-64% of key fertilizer/chemical imports). India (18% of urea imports), China (methanol/MEG buyer), and East Asia (petchem plants curtailing) face dual energy + feedstock shocks. Food inflation compounds existing vulnerabilities.

Global South / Developing Economies: Africa (Zambia), South Asia (Pakistan, Sri Lanka), and Latin America (Brazil) suffer acute fertilizer-driven food price spikes and reduced agricultural output.

Europe: Secondary but significant hits to energy, fertilizers, and supply chains; higher costs feed into manufacturing and households.

Australia: Tindale’s focus—material supply shock drains capital, erodes productive capacity, and accelerates de-industrialization (Tindale’s Trap).

U.S./Americas: Higher fertilizer and plastic costs hit farmers and consumers, though domestic energy production offers some buffer.

Investor and Consumer Implications

Investors: Winners: Upstream energy producers, oil majors, certain fertilizer and commodity firms (physical assets and real supply win in shortages).

Risks: Downstream manufacturers, consumer staples, airlines, and broad equities face margin compression and demand destruction. Inflation hedges (gold, certain commodities) may outperform. Watch for arbitrage opportunities as China consolidates some petchem capacity via Russian feedstocks. Prolonged closure favors producers with alternative routes or inventories.

Tindale warns central-bank missteps could create a “blind spot” for portfolios unprepared for the poly-crisis amplification.

Consumers:

Expect higher prices at the pump, grocery store (food + packaging), and for everyday goods (plastics in everything from phones to clothing). Cost-of-living pressures will intensify, especially in import-dependent regions, potentially sparking social and political strain.

The Path Ahead

Tindale’s framework shows this shock is self-reinforcing: feedstock shortages → higher input costs → reduced productive capacity → central-bank tightening → deeper de-industrialization and food stress, all amplified by weather and policy. The Strait’s reopening timeline remains uncertain; infrastructure repair could take months to years.Markets and policymakers must now grapple with the reality that you cannot print feedstocks. The PetroChemical Feedstocks Shock is not just unfolding—it is reshaping global trade, agriculture, and finance for 2026 and beyond.

Appendix: Resources and Links

- Craig Tindale’s X Post (April 25, 2026): https://x.com/ctindale/status/2047911835840749798 (includes full slide deck titles and PowerPoint reference).

- Atlantic Council: “The Strait of Hormuz closure forces a choice…” (April 2026). https://www.atlanticcouncil.org/dispatches/the-strait-of-hormuz-closure-forces-a-choice-ration-oil-now-or-pay-a-steep-price-later/

- PBS News: “Hormuz standoff the ‘largest supply shock’ ever…” https://www.pbs.org/newshour/show/hormuz-standoff-the-largest-supply-shock-ever-experienced-says-global-energy-expert

- World Economic Forum: “9 commodities impacted by the Strait of Hormuz crisis” (April 1, 2026). https://www.weforum.org/stories/2026/04/beyond-oil-lng-commodities-impacted-closure-hormuz-strait/

- UNCTAD: “Strait of Hormuz disruptions: Implications for global trade…” https://unctad.org/publication/strait-hormuz-disruptions-implications-global-trade-and-development

- Kiel Institute Policy Brief: Economic modeling of Hormuz closure. https://www.kielinstitut.de/fileadmin/Dateiverwaltung/IfW-Publications/fis-import/01b7c020-27e6-4096-8cc5-e037738d2058-KPB_206.pdf

- Additional context from Reuters, Bloomberg, Argus Media, and Dallas Fed reports on price impacts and regional exposure (March–April 2026).

Energy News Beat will continue monitoring developments and updating analysis as the PolyCRISIS evolves.