It is a wild day on the News Desk, and we saw Brent hit $105, and the market tanked. This is not going to be over very quickly, as there is a lot to unwind in the oil and gas markets and supply chains.

We are seeing new proposed pipelines, and Energy Security is really taking front and center stage around the world.

For all the stories I covered today, you can go to the best Podcast Show Notes Page in the world. Energy News Beat. https://energynewsbeat.com/. Just saying, I have not seen another show notes page like this one for a podcast.

1. Oil and Energy Market Dynamics

The Podcast extensively covers how global oil markets are being affected by geopolitical tensions, particularly disruptions in the Middle East and the Strait of Hormuz. There’s discussion about establishing a new baseline for oil prices (around $90-$95 range) and the risk of demand destruction if prices remain elevated. The speaker also analyzes the disconnect between how oil/gas companies are performing versus refineries in the current market environment.

2. Energy Security and Self-Reliance

A significant focus is placed on countries building domestic refining and drilling capabilities to reduce dependence on imports. The transcript highlights U.S. efforts to increase energy independence and export capabilities, with specific examples like the Golden Pass LNG facility and Japan’s JAPEX expanding into the U.S. oil and gas market.

3. Geopolitical Developments

The discussion addresses potential permanent disruptions to Middle Eastern oil supplies and their global market impact. There’s also mention of U.S. government efforts to re-engage with Venezuela to boost oil production and exports.

4. Regulatory and Policy Changes

The podcast covers bipartisan efforts in Pennsylvania to maintain coal-fired power plants despite the broader shift toward natural gas and renewables. California’s refinery issues and the Jones Act’s impact on U.S. energy supply and pricing are also discussed.

5. Stock Market and Investment Analysis

Stu provides insights on the performance of various energy-related stocks, including oil and gas companies, refiners, and LNG players, identifying potential investment opportunities and risks in the current market.

1.Is $90 to $95 Oil Is the New Baseline for 2026

$90–$95 oil is no longer a spike — it is the new baseline. Here’s why the financial and physical realities point to sustained elevated prices well into 2026, even if the strait reopens soon.

Supply Constraints: How Long Can Oil Hold Above $90?

The core driver is a persistent supply deficit. In March 2026 alone, global oil supply fell 10.1 million bpd to 97 million bpd, with OPEC+ output dropping 9.4 million bpd. Gulf producers curtailed heavily as export routes vanished and storage filled: Iraq’s output plunged from 4.57 to 1.57 million bpd, Kuwait from 2.54 to 1.19 million bpd, Saudi Arabia from ~10.4 to 7.25 million bpd, and the UAE from 3.64 to 2.37 million bpd. Overall, ~9–11 million bpd of crude was effectively removed from the market relative to pre-war baselines.

Alternative pipelines (Saudi west coast, UAE Fujairah, Iraq-Turkey) boosted flows to ~7.2 million bpd from under 4 million bpd, but this only partially offset the ~13+ million bpd export loss.

If the Strait does not stabilize in the coming weeks, the shock intensifies. Analysts warn that prolonged closure into Q2 could push prices toward $120–$200/bbl scenarios, with physical shortages spreading from Asia to Europe.

Even partial reopening will not flip the switch. The IEA’s base case assumes a gradual resumption by mid-2026 but not back to pre-conflict levels; a “protracted” case sees deficits persisting, forcing even deeper demand cuts.

Tanker Repositioning: Weeks to Months of Lag

The tanker fleet is scattered. Thousands of vessels loitered west of Hormuz or diverted routes (adding 6,500+ nautical miles and 15+ days per Europe-Gulf loop). Even with safe passage restored, full normalization takes 6–8 weeks for repositioning, plus 2–5 weeks for insurers and owners to regain confidence.

Loaded tankers already en route to alternative destinations (e.g., U.S. for non-Gulf barrels) must be recalled or replaced. It can take up to a month for new cargoes to reach buyers after loading. Backlogs of ~3,200 vessels (including ~800 tankers) compound port congestion.

This logistical tail means the physical supply recovery lags any diplomatic breakthrough by months — keeping the market tight and prices supported at $90+ through much of 2026.Middle East Wells Shut Down: How Many, and How Long Until They Return?

Roughly 10+ million bpd of Gulf production was shut in by mid-March, with April estimates around 9+ million bpd across Saudi Arabia, UAE, Kuwait, Iraq, and others.

Restart is not instantaneous:

Unscathed wells can reach 50% output in ~2 weeks and 80% in another 2–3 weeks.

Many require weeks to months for full ramp-up due to pressure management and safety checks.

Damaged infrastructure (refineries, processing plants, pipelines) from strikes could take months or years; historical precedents like the 1991 Gulf War show full recovery spanning years and billions in costs.

Some wells may never return at prior rates without major investment — especially if producers wait for long-term confidence in export routes. This creates a multi-quarter (if not multi-year) drag on supply, reinforcing the higher price floor.

Storage vs. Exports: The Imbalance That Keeps Pressure On

While the Middle East built floating storage (+100 million barrels) and onshore crude stocks (+20 million barrels) in March as exports stalled, the rest of the world drew inventories sharply: global observed stocks fell 85 million barrels, with non-Gulf stocks down 205 million barrels (-6.6 million bpd). Asian importer stocks dropped 31 million barrels.

This regional imbalance forces continued shut-ins until exports normalize. Once the Strait reopens, ME producers will first drain built-up storage before ramping output — delaying the global supply response. The IEA notes this dynamic already drove refinery run cuts of ~6 million bpd in Asia and the Middle East in April.

Demand Destruction: The Economic Headwind

High prices are already biting. The IEA slashed its 2026 demand forecast to a contraction of 80,000 bpd (from +730,000 bpd pre-crisis), with Q2 2026 seeing the sharpest year-on-year drop since COVID (-1.5 million bpd). March demand fell 800,000 bpd y/y; April is projected at -2.3 million bpd.

Refineries curtailed runs, petrochemical output plunged, and governments imposed rationing, remote-work mandates, and fuel-saving measures across Asia and beyond. At sustained $100–$130 levels, inflation rises (U.S. CPI +1 point or more; euro area GDP hit ~0.6%), crimping economic growth and oil consumption.

This self-correcting demand destruction helps balance the market but at the cost of slower global GDP — underscoring why $90–$95 becomes the “new normal” rather than a temporary spike. Markets now price in tighter balances persisting into late 2026 even under optimistic recovery scenarios.

This one is going to be tough. When it snaps, people will be shocked.

3.Energy Security Starts at Home: More Countries Are Building Refineries and Drilling Programs

This is cool, and Countries are looking at local production, refineries, and not relying on others.

4.Oil Disruption of the Strait of Hormuz May Be More Permanent Than a Few Weeks

5.Golden Pass LNG: QatarEnergy/ExxonMobil Joint Venture in Sabine Pass Makes First Shipment

Golden Pass LNG, a major joint venture between QatarEnergy (70%) and ExxonMobil (30%), has reached a historic milestone. On April 22, 2026, the company announced that its first liquefied natural gas (LNG) export cargo has departed from its Sabine Pass terminal in Texas. The 174,000-cubic-meter QatarEnergy-owned carrier Al Qaiyyah loaded the inaugural cargo at the facility and has now sailed. Reuters previously reported the destination as Italy, aligning with QatarEnergy’s offtake contracts.

This marks the culmination of years of development for one of North America’s largest new LNG export projects. First LNG production from Train 1 was achieved on March 30, 2026, setting the stage for sustained operations. The terminal is now transitioning from commissioning to commercial exports, with feedgas intake recently hitting record levels around 400–434 million cubic feet per day (MMcf/d) as the first train ramps up.

Project Details and Capacity

Golden Pass LNG features three liquefaction trains with a total nameplate capacity of approximately 18 million metric tons per annum (mtpa), equivalent to roughly 2.4–2.5 billion cubic feet per day (Bcf/d) of feedgas once fully operational. Train 1 alone is expected to contribute around 800 MMcf/d (~5–6 mtpa) initially, with Trains 2 and 3 following in 2027. The $10+ billion project includes five 155,000-cubic-meter storage tanks and two marine berths. Located in Sabine Pass (Port Arthur area), Texas, it leverages existing infrastructure originally built for imports before the U.S. shale boom turned the country into a net exporter.

What This Means for U.S. Investors, ExxonMobil, and Qatar

EnergyFor U.S. investors and the energy sector: The startup adds incremental U.S. LNG export capacity at a time of strong global demand. It boosts demand for domestic natural gas from key basins like the Haynesville and Permian, supporting producers, midstream companies, and jobs in Texas. With U.S. LNG now a cornerstone of global energy security—especially for Europe and Asia—this project reinforces America’s position as the world’s top LNG exporter and provides a hedge against international supply disruptions.

For ExxonMobil (30% stake): The milestone strengthens Exxon’s growing LNG portfolio and delivers new revenue streams from U.S.-sourced gas. As a low-cost, flexible supplier, Golden Pass enhances Exxon’s global competitiveness and long-term cash flow potential for shareholders.

For QatarEnergy (70% stake): This represents QatarEnergy’s largest investment in the United States and a key pillar of its international LNG expansion strategy. The project diversifies Qatar’s supply beyond its home base, secures long-term offtake (including to Europe), and solidifies its role as a global LNG leader.

6.Japan’s Japex to Expand Oil and Gas Production, Including in the U.S.

Japex should have called me, as I could have told them to buy other assets. This will be a problem, as Colorado is taking lessons from Gavin Newsom’s California on how to ruin the oil and gas industry. I loved looking up the assets in Welldatabase.

They are one of our new Sponsors, and we have some more cool things rolling out with them soon.

Spending this much money is one thing; having assets controlled in a Blue or Net Zero State is going to be problematic in getting your return on investment. But then again, what is $1.26 billion between friends?

7.Two Clean Coal Plants in Pennsylvania Are Staying Open Thanks to Trump and Shapiro

This was cool.

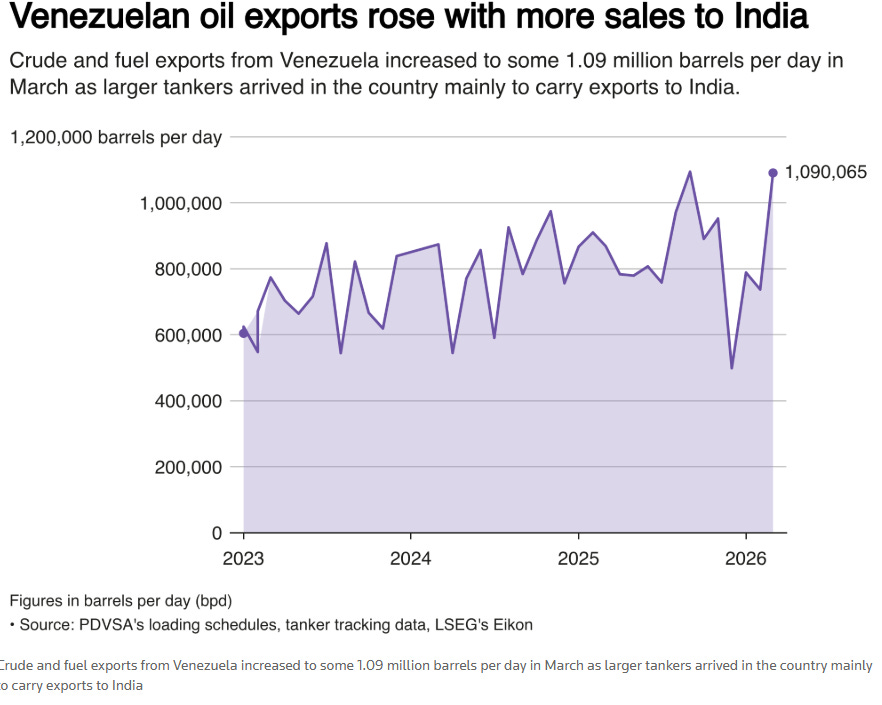

8.US Oil Executives Meet Venezuela President and What Does This Mean for Investors and Consumers?

In a notable development for global energy markets, a group of U.S. oil executives traveled to Caracas last week for direct talks with Venezuela’s acting President Delcy Rodríguez. The meeting, reported by Bloomberg, occurred as the Trump administration continues its aggressive push to revive Venezuela’s long-dormant oil sector following the January 2026 ouster of former President Nicolás Maduro.

Accompanying the executives was a top U.S. Energy Department official. The delegation included:

Doug Lawler, CEO of Continental Resources

Bryan Sheffield, founder of Formentera Partners (a Texas-based independent oil company) – I have reached out to him to see about getting on the podcast.

Kevin McCarthy, board member of Aspect Holdings LLC

The primary goal: secure assurances on investment safety and legal protections as U.S. companies explore re-entry into one of the world’s most oil-rich nations.

9.California is Within Weeks of a Shutdown

This is critical. The ships will be in from Asia, and the last ones should be off the water in about 2 to 3 weeks. Limited supplies of jet fuel, diesel, and gasoline will be available after that. We went from 97% energy independent in California to 60% Dependent, and 6 of the 7 remaining refineries are set to close.

This is a national security disaster about to happen.

Check out the Energy News Beat SubStack

A shout-out to Steve Reese and the Reese Energy Consulting group for sponsoring the Podcast https://reeseenergyconsulting.com/.

Data2: If you have any business systems, can you trust A? Well, they have the patent on validation. . https://data2.zoholandingpage.com/energy

And we have WellDatabase rolling in as a new sponsor. https://welldatabase.com/