In a stark warning delivered at S&P Global’s Middle East Petroleum & Gas Conference in London, Vitol board member Tom Baker pulled no punches: “In Europe and I think in the US, everyone is kind of asleep at the wheel and just carrying on life as normal.”

Vitol, one of the world’s largest independent oil traders, is sounding the alarm on a global oil supply crunch triggered by the ongoing blockade of the Strait of Hormuz. The disruption stems from the 2026 Iran war—U.S. and Israeli strikes that began February 28 and have effectively halted roughly 20% of global oil trade through the critical chokepoint.

The “rubber band” analogy fits perfectly: months of inventory draws, Strategic Petroleum Reserve (SPR) releases, and suppressed visible demand have stretched the market to its limit. When it snaps—whether through sudden peace, further escalation, or outright physical shortages—prices could surge violently before correcting. Here’s what that means for consumers, investors, and energy markets through the rest of 2026.

The Geopolitical Three-Way Tug-of-WarThe supply crunch persists because Washington, Tehran, and Jerusalem are operating on mismatched playbooks:

Trump Administration: Painting a “closed end” to the conflict. President Trump has repeatedly signaled optimism for a ceasefire, floated temporary lifts on Iranian oil sanctions to calm markets, asked Israel to halt strikes on Iranian energy infrastructure, and even discussed releasing more SPR barrels or restricting U.S. exports.

The White House is laser-focused on lowering prices ahead of any political fallout, with Treasury officials openly discussing options to tame the surge.

Iran: Not on the same page. Tehran has rejected U.S. proposals as “unacceptable,” demanded compensation for war damage, an end to naval blockades, full sanctions relief, and recognition of its sovereignty over the strait. Iranian officials have threatened to maintain the blockade and have suspended talks multiple times.

Israel: On a third, more aggressive playbook. Israeli leadership continues pushing for Iran’s permanent weakening and regime-change elements, with strikes on energy sites proceeding despite U.S. requests to pause.

This misalignment means the Hormuz blockade—now in its fourth month—has already drained global inventories at record pace and pushed the U.S. SPR near historic lows (down to ~357–374 million barrels).

Physical shortages could hit Europe “any day now,” according to strategists, with full recovery of stockpiles potentially delayed until late 2027 if the crunch drags on.

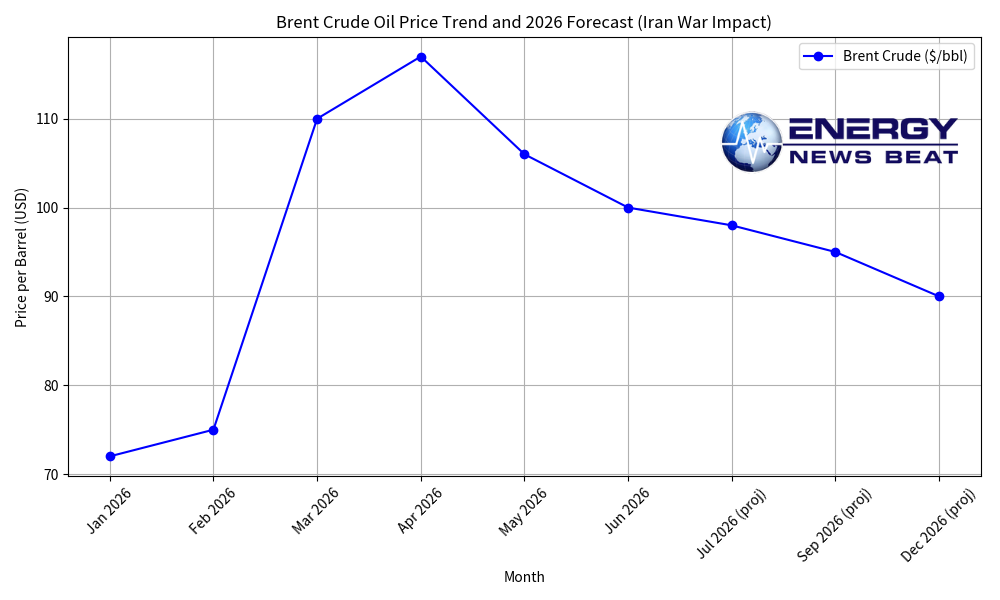

Chart: Brent Crude Oil Price Trend and 2026 Forecast

(Approximate monthly averages and projections based on EIA, bank forecasts, and market reports showing pre-war levels, April spike, current levels, and expected easing if disruption eases.)

Consumer Impact: The Hidden Tax at the Pump and on Bills

American and European households are already feeling the pinch. U.S. gasoline prices hover near $4.26/gallon nationally, with some analysts warning of $150–$160/barrel spikes if SPR draws accelerate further.

Higher jet fuel and diesel costs are rippling into airfares, trucking, and groceries.

In Europe, the crisis echoes 2022 but hits harder: the continent imports far less Middle East oil than in the 1970s, yet the sheer scale of the ~20 million bpd disruption (versus 4.5 million in 1973) is exposing vulnerabilities in LNG and refined products.

Households face elevated heating and power bills, especially if winter storage refill becomes expensive.

The rubber-band snap could deliver a short, sharp inflation shock—good for no one except perhaps oil-producing states.

Investor Impact: Opportunity Amid Volatility

Energy producers and midstream companies stand to benefit from sustained high prices in the near term. U.S. shale, Gulf of Mexico, and Canadian producers are seeing windfall margins, while LNG exporters (especially new U.S. Gulf Coast capacity) could capture arbitrage if European and Asian spot prices remain elevated.

However, the backwardation in oil futures (near-term prices far above 2026 contracts) signals that traders expect eventual normalization—potentially a rapid price collapse once Hormuz reopens.

Investors in oil-field services, refiners, and integrated majors should hedge aggressively; those in renewables or efficiency plays may see renewed policy tailwinds if high prices accelerate the energy transition narrative.

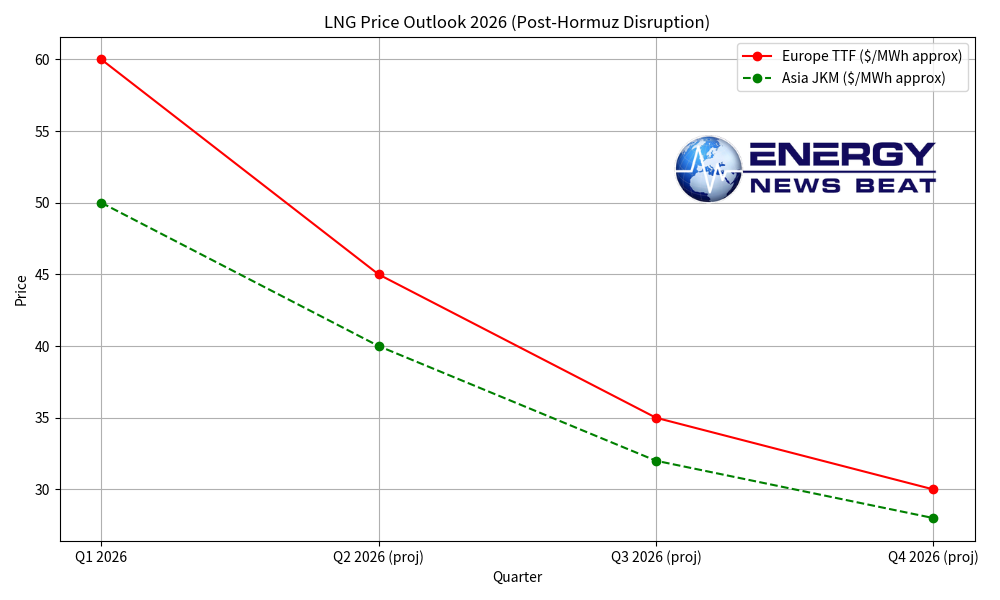

Chart: LNG Price Outlook 2026

(Europe TTF and Asia JKM benchmarks—initial Hormuz-driven spike followed by expected softening from new U.S./global supply.)

Oil and LNG Price Outlook: Remainder of 2026Oil (Brent): Expect continued volatility in the $90–$110/bbl range through summer, with EIA projecting ~$106 in Q2 before easing to $89 in Q4 if production rebounds.

Bank forecasts cluster around $90–$100 average for the year (HSBC, UBS, Barclays), with upside risks if the blockade persists and downside if a deal materializes quickly.

WTI will trade at a discount but follow similar dynamics. A “snap” resolution could see prices drop toward the mid-$70s–$80s by year-end.

LNG: Short-term strength from Qatari and other Middle East disruptions, but global supply is ramping fast (+7% or 40+ bcm in 2026, led by North America).

Spot prices (JKM/TTF) are forecast to soften toward $9–$10/MMBtu average, with Europe–Asia convergence by late decade. New U.S. export capacity will help refill storage, but any prolonged Hormuz issues keep winter 2026–27 contracts elevated.

Bottom line: The rubber band is stretched tight. Vitol’s wake-up call is timely—Europe and the U.S. may be “asleep at the wheel,” but markets never sleep. Investors and consumers alike should prepare for a volatile ride through the second half of 2026. Resolution timing will dictate whether this crunch becomes a brief spike or a multi-quarter headache.

- Bloomberg original article (Vitol comments): https://www.bloomberg.com/news/articles/2026-06-02/vitol-says-europe-and-us-aren-t-facing-up-to-oil-supply-crunch

- EIA Short-Term Energy Outlook (June 2026): https://www.eia.gov/outlooks/steo/

- Additional context from Reuters, CNBC, Axios, Wikipedia summaries of 2026 Iran war fuel crisis, Hart Energy, and bank research notes (HSBC, UBS, Barclays, JPMorgan).

- Charts generated from aggregated public data and forecasts cited above.

Energy News Beat delivers independent, data-driven analysis for energy professionals and investors. Stay tuned for podcast follow-ups.