In a market grappling with tumbling crude prices and an oversupply of oil, major oil companies are aligning with OPEC’s strategy by ramping up production. This week’s earnings reports from industry heavyweights like ExxonMobil, Chevron, Shell, BP, and TotalEnergies are expected to confirm these expansion plans, signaling a push forward despite short-term headwinds. As Brent crude hovers around lower levels due to modest global demand and robust supply growth, these firms are betting on a price recovery in the latter half of 2026.

Aligning with OPEC Amid Market Challenges

OPEC and its allies have been increasing output, contributing to a global surplus estimated at 1.9 million barrels per day from January to September 2025, with projections rising to 4 million barrels per day in 2026 according to the International Energy Agency.

In parallel, Big Oil is accelerating production through new projects and acquisitions. Analysts forecast a collective output growth of 3.9% for 2025 and 4.7% in 2026 among ExxonMobil, Chevron, Shell, BP, and TotalEnergies.

This strategy aims to capitalize on an anticipated upturn in oil prices next year, even as current conditions remain weak with Brent crude down 13% year-over-year in the third quarter.

The production boosts come at a time when the industry is facing sluggish demand, influenced by factors like moderate global economic growth and the rapid adoption of electric vehicles in China.

Additionally, new U.S. sanctions on Russian oil are unlikely to significantly disrupt markets, as Russia continues exports via alternative channels, and other OPEC members like Kuwait stand ready to fill any gaps.

Despite these pressures, oil giants are prioritizing long-term positioning over immediate cutbacks.

Third-quarter 2025 earnings are set to edge higher from the second quarter, buoyed by marginally better oil prices, stronger refining margins, and increased production.

However, results are generally expected to be down year-over-year, reflecting the broader decline in commodity prices since 2022 peaks.

Here’s a breakdown of key reporting dates and projections:

Shell and TotalEnergies (October 30, 2025): Shell is forecasted to post an 18% increase in adjusted net income from Q2, while TotalEnergies anticipates an 11% rise, both down from last year. Higher production and refining margins will support TotalEnergies’ results, but debt levels—up 89% in the first half of 2025—remain a concern.

ExxonMobil and Chevron (October 31, 2025): Exxon could see earnings boosted by up to $700 million from stronger refining, while Chevron is projected at $3.4 billion in adjusted profit. Chevron’s recent $55 billion acquisition of Hess is expected to contribute modestly this quarter, with full integration details forthcoming.

BP (November 4, 2025): Net profit is expected to drop about 10% year-over-year to just over $2 billion, offset by higher refining margins that could triple operating profits in its products division.

These reports follow a trend of declining adjusted earnings since Q3 2021, hitting pandemic-era lows.

U.S. natural gas prices, up 37% year-over-year, provide some relief, but the sector’s overall performance has lagged the broader market, with stocks like Exxon and Chevron returning only 14% since early 2024 compared to 46% for the S&P 500.

Bloomberg Writes:

Source: Bloomberg

After years of outsized profits as oil demand roared back following the pandemic, the world’s largest energy companies are feeling the pinch of crude prices that have dropped about 14% this year near to a four-year low. In response, they’re cutting jobs, reducing low-carbon investments and trimming share buybacks to channel funds toward the most valuable part of their business: oil and gas production.

“All the supply coming to the market is shrinking OPEC’s spare capacity — so there’s a light at end of the tunnel,” said Betty Jiang, an analyst at Barclays Plc. “Whether that’s second half of 2026 or 2027, the balance is going to tighten. It’s just a matter of when.”

Recent US sanctions on key Russian giants Rosneft PJSC and Lukoil PJSC provided respite from oil’s fall this year, with Brent crude rising 7.5% last week to more than $65 a barrel. But the oil market is oversupplied heading into 2026 and the Organization of the Petroleum Exporting Countries and its allies remain focused on adding more supply.

It may seem counterintuitive for the supermajors to add barrels to such a market, but executives have an eye on the future, when crude may not be so plentiful. Oil demand is still growing, albeit slowly, while US shale and supply from new fields in Guyana and Brazil are likely to decelerate in the latter half of the decade.

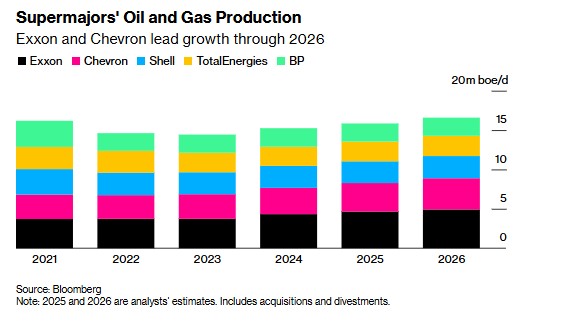

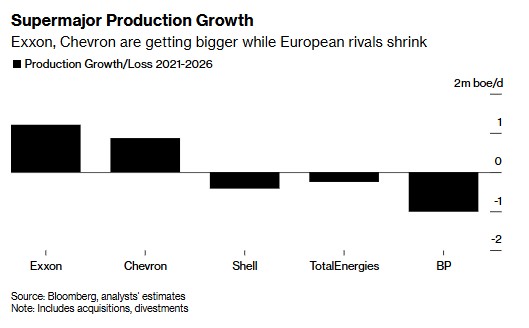

The growth is coming from three main sources. The first is investments made within the past few years that are now bearing fruit, like Chevron’s Ballymore project in the US Gulf. The second source is new projects, such as Exxon’s Uaru development in Guyana. And the third is acquisitions, which add to companies’ individual production without adding barrels to global supply. The biggest examples are Exxon buying Pioneer Natural Resources Co. and Chevron buying Hess Corp.

The US majors are advancing on all three of those fronts while Shell and BP are focusing on the first two for now. That’s because their lower value stock makes deals more difficult to pull off. The trend stands in stark contrast to the downturn in oil prices during the pandemic, when companies cut capital spending and slowed majors projects because oil demand fell fast and they were unsure when it would return.

Source: Bloomberg

Selling more barrels will also help mitigate lower prices in the short run. The five supermajors will likely post combined profits of $21.76 billion for the third quarter, according to analysts’ estimates compiled by Bloomberg. That’s 7% higher than the previous three months, helped by better refining margins. But it’s less than half the levels of 2022. The industry has hiked dividends and buybacks since then, making the payouts harder to sustain.

“This has been the most well-telegraphed oil glut in history, which suggests that it won’t be that bad,” James West, managing director of energy and power research at Melius Research. “The supermajors have been preparing it for a while, but there is going to be pressure on free cash flow.”

Missing the AI Energy Boom and Cost-Cutting Measures

One notable missed opportunity for Big Oil is the surging energy demand from AI data centers. While tech giants’ investments have spiked power needs, benefits have flowed more to utilities than oil and gas producers. Natural gas prices in the U.S. haven’t risen sharply due to ample domestic supply, and global LNG expansions from the U.S. and Qatar are poised to depress prices further.

In response to fading “monster profits,” companies are focusing on cost reductions and shareholder returns. Last year, the top firms paid out a record $120 billion in dividends and buybacks—56% of operating cashflow—up from 30-40% in prior decades.

Shell recently announced a $3.5 billion buyback, while others like Exxon (3-4% workforce cut), Chevron (potential 20% headcount reduction), BP, and Shell are retrenching to free up cash.

TotalEnergies has cut buybacks, trimmed capex, and sold assets like a solar portfolio to manage debt.

What Investors Should Look For This Week

As these earnings unfold, investors will scrutinize several key areas to gauge the sector’s resilience and future trajectory:

Production and 2026 Guidance: Confirmation of output growth plans amid the supply glut, including how firms plan to navigate a potential 4 million bpd surplus next year.

Capital Spending and Cost Management: Potential capex cuts, such as Exxon’s possible reductions in early-stage opportunities (currently $2.5 billion annually), and updates on divestments like BP’s $20 billion strategy including the Castrol sale.

Shareholder Returns: Details on dividends and buybacks, with BP offering a higher yield compared to peers like Shell, Exxon, and TotalEnergies.

Debt and Financial Health: For TotalEnergies, responses to rising debt and its impact on returns; broader commentary on tariff costs and natural gas outlooks amid AI-driven demand.

M&A and Integration: Progress on deals like Chevron-Hess, and any signals of further acquisition pursuits from Exxon.

Long-Term Outlook: Despite short-term gloom, signs of bullishness, such as Exxon’s steady $27-29 billion capex for 2025.

While the industry remains in a funk, these reports could provide clues on whether Big Oil’s production push with OPEC will pay off in a recovering market. Investors eyeing stocks like Exxon or Chevron for 2026 may find value in their disciplined approaches, but caution is advised amid ongoing volatility.

Daily Standup Weekly Top Stories EPA’s Final Rule for Oil and Natural Gas Operations Will Sharply Reduce Methane and Other Harmful Pollution. December 2, 2023 Stu Turley ENB Pub Note: We will review these regulations and […]

French energy giant TotalEnergies has entered into deals to supply liquefied natural gas (LNG) to Indian Oil and Korea South-East Power. TotalEnergies said on Tuesday these contracts allow the firm to secure medium-term outlets for […]

In a stunning blow to global climate finance efforts, the Net-Zero Banking Alliance (NZBA), once hailed as a cornerstone for the banking sector’s push toward carbon emission reductions, has voted to cease operations effective immediately. […]

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.