In the volatile landscape of global energy markets, oil prices are poised for a significant upward trajectory amid escalating geopolitical tensions in the Middle East. As of March 6, 2026, Brent crude has already surged above $89 per barrel, driven by a confluence of factors including disrupted shipping routes, production halts, and a burgeoning crisis in maritime insurance. At the heart of this turmoil is the Strait of Hormuz—a critical chokepoint through which roughly a fifth of the world’s oil and gas transits. The ongoing 2026 Iran war, marked by U.S.-Israeli strikes on Iranian targets and retaliatory actions, has not only heightened physical risks but also triggered a meltdown in the insurance sector. This article delves into the key details surrounding tanker hesitations, insurance availability, bottlenecks in the strait, recent attacks, and Qatar’s stark warning of $150 oil.

The Insurance Crisis: Hesitations, Delays, and Skyrocketing Premiums

The insurance predicament has emerged as a pivotal driver of the current energy squeeze. Maritime insurers, led by heavyweights at Lloyd’s of London, have responded to the intensified conflict by expanding “high-risk” designations across the Persian Gulf, Gulf of Oman, and adjacent waters.

This has led to widespread cancellations of war-risk policies or dramatic premium hikes, effectively paralyzing commercial shipping. War-risk premiums for transits through the Strait of Hormuz have jumped from 0.05–0.15% of a vessel’s hull value to 0.3–0.7% or higher, adding hundreds of thousands of dollars per voyage.

For a $100 million vessel, this could mean costs exceeding $700,000 for a single trip—up from pre-escalation levels.

Tankers are showing clear hesitation to rely on the emerging “American system” for insurance, which refers to the U.S. government’s initiative through the International Development Finance Corporation (DFC) to provide political risk guarantees at “very reasonable” rates.

Announced by President Trump as part of his strategy to secure the strait, this move aims to displace traditional players like Lloyd’s by leveraging U.S. naval dominance.

However, industry experts express skepticism: the program is untested, and naval escorts could inadvertently heighten risks by drawing more attacks.

As one Lloyd’s insider noted, “If the American Navy is providing the security, why should London reap the premiums?” Yet, shipowners remain wary, citing potential bureaucratic delays and the political optics of aligning with U.S. guarantees amid a multi-front war.

Confirmed reports indicate that insurance is still being sold, but selectively and at exorbitant rates. Lloyd’s of London is not outright delaying approvals but has activated “major event response” protocols, issuing 72-hour cancellation notices to reassess risks.

Several mutual marine insurers, including Gard, Skuld, NorthStandard, the London P&I Club, and the American Club, have canceled coverage for Gulf operations.

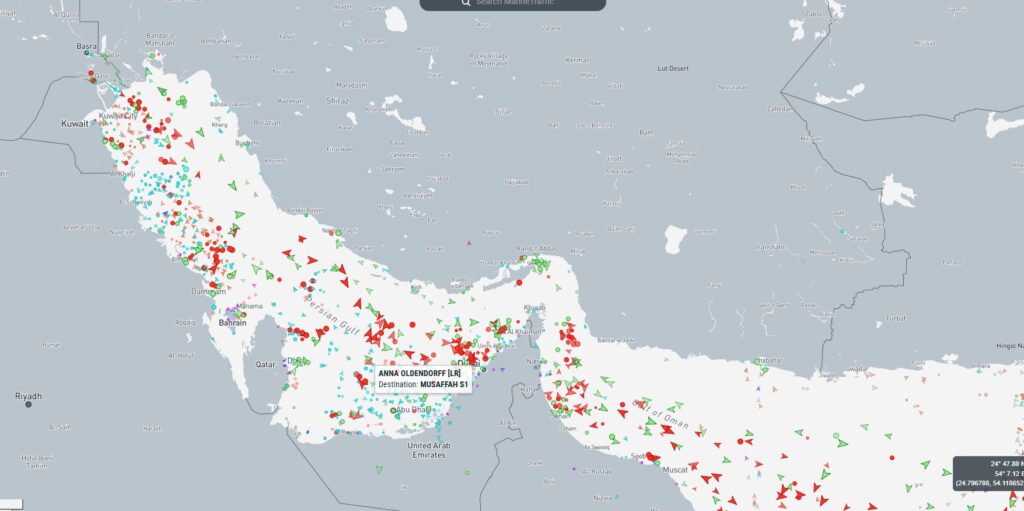

This has created a “de facto closure” of the strait, with over 150 vessels, including oil and LNG tankers, anchored and unable to proceed.

Underwriters are engaging with the U.S. government on collaborative solutions, but the hold-up stems from rapidly evolving threat assessments rather than deliberate obstruction.

Historical parallels abound: during the 1980s Tanker War, over 500 vessels were attacked, but insurance markets adapted. Today, however, prior strains from Houthi attacks in the Red Sea (2023–2025) have already depleted war-risk capacity, making the current spike more acute.

Bottlenecks in the Strait: Insurance Isn’t the Only Hurdle

While the insurance fiasco is a primary bottleneck, it’s far from the only one impeding ship movements through the Strait of Hormuz. Physical security threats have compounded the issue, with at least three tankers damaged and one seafarer killed in weekend attacks attributed to Iran’s Islamic Revolutionary Guards Corps (IRGC).

Reports confirm projectiles striking vessels, including a containership hit in the strait’s southern end.

The U.S. Navy has neutralized some Iranian threats, but the presence of strike groups like USS Gerald R. Ford adds to the congestion and risk perception.

By March 3, 2026, active tanker transits had dropped to zero, creating a backlog that exacerbates storage issues onshore.

Kuwait has already begun shutting in production at some oilfields due to overflowing storage, with discussions underway for deeper cuts to match domestic needs.

Europe’s gas prices are also spiking, signaling broader supply chain ripples.

Escalating Attacks: A Resurgent Threat from Multiple FrontsAttacks have indeed intensified. In the Gulf, IRGC missiles struck U.K. and U.S.-linked tankers, setting some ablaze.

Meanwhile, Yemen’s Houthis—aligned with Iran—have announced a resumption of strikes in the Red Sea, ending a brief pause tied to a Gaza ceasefire.

As of March 4, 2026, no major Red Sea incidents have materialized due to internal Houthi debates, but threats target U.S. and Israeli-flagged ships.

A U.S. warship reportedly downed Houthi drones, and the group claims attacks on the USS Harry Truman carrier.

This dual-front crisis—Gulf and Red Sea—recalls 2024 peaks when Red Sea war-risk premiums hit 1% of vessel value, adding $1+ per barrel to oil costs.

Shipping volumes in the Red Sea plummeted 65% by mid-2025, forcing reroutes around Africa that inflated freight rates by 50–100%.

Qatar’s $150 Oil Warning: A Dire Forecast Amid Force Majeure Fears

Qatar’s Energy Minister Saad al-Kaabi issued a chilling warning on March 6, 2026: if the war persists, all Gulf exporters could halt production “within days,” invoking force majeure clauses.

He predicts oil surging to $150 per barrel in two to three weeks if the Strait remains inaccessible, triggering global shortages, factory shutdowns, and economic downturns.

“This will bring down the economies of the world,” al-Kaabi told the Financial Times, emphasizing the chain reaction from disrupted energy flows.

The rationale? With tankers idled by insurance woes and attacks, producers like Qatar, Saudi Arabia, and the UAE face overflowing storage and no export outlets. Kuwait’s shutdowns are an early sign.

At $150 oil, inflation would spike worldwide, eroding GDP growth and amplifying the war’s economic fallout.Key Issues: A Perfect Storm for Energy MarketsThe crisis boils down to several intertwined challenges:

|

Issue

|

Description

|

Impact

|

|---|---|---|

|

Insurance Meltdown

|

Cancellations and premium surges from Lloyd’s and others; U.S. alternative met with hesitation.

|

De facto strait closure; added $3–8/bbl in costs. @OilandEnergy

|

|

Physical Attacks

|

IRGC strikes in Gulf; Houthi threats in Red Sea.

|

Vessel damage, seafarer risks, naval escalations.

|

|

Production Halts

|

Kuwait shutting fields; potential Gulf-wide force majeure.

|

Immediate supply cuts, storage overflows.

|

|

Geopolitical Tensions

|

U.S.-Israel vs. Iran proxy war.

|

Broader disruptions, including to 20% of global oil/gas.

|

|

Economic Ripples

|

Higher freight/insurance; rerouting delays.

|

Inflation resurgence, global GDP drag.

|

These factors have already pushed oil to 23-month highs, with analysts forecasting sustained volatility.

The 30 Day delay of Sanctions on Russian Oil in Transit May Help for a few days.

The Trump adminstration 30 day waiver on Russian oil already in tankers is a help for India or China to take advantage. It will be interesting to see if California also takes advantage, and we will be watching.

Outlook: Navigating the Uncertainty

As the insurance problem grows, oil prices are undeniably set to rise, potentially testing $100+ in the near term. The U.S. push for alternative coverage could stabilize flows if adopted, but hesitations persist amid ongoing attacks. Qatar’s warning underscores the fragility: without de-escalation, $150 oil isn’t hyperbole—it’s a plausible nightmare. For energy stakeholders, from podcast hosts to policymakers, monitoring insurance markets and strait transits will be crucial in the weeks ahead. The world watches as this crisis unfolds, with profound implications for global stability.

Sources: morningstar.com, oilprice.com, insurancebusinessmag.com,

Be the first to comment