In a rapidly evolving global energy landscape, recent U.S. actions in Venezuela, combined with broader monetary and diplomatic strategies, are reshaping oil and gas markets. These shifts aim not only to stabilize prices and bolster the U.S. dollar but also to foster peace by undermining adversarial networks that fund conflicts like the war in Ukraine. Drawing from recent developments, including Treasury Secretary Scott Bessent’s controls on Venezuelan oil sales and Interior Secretary Doug Burgum’s push for critical minerals access, this article explores how these changes could cut funding to illicit “dark fleet” tankers, pressure Russia toward peace, and align with Saudi Arabia and OPEC to strengthen traditional market structures.

Oil Stands to rise in the short term:

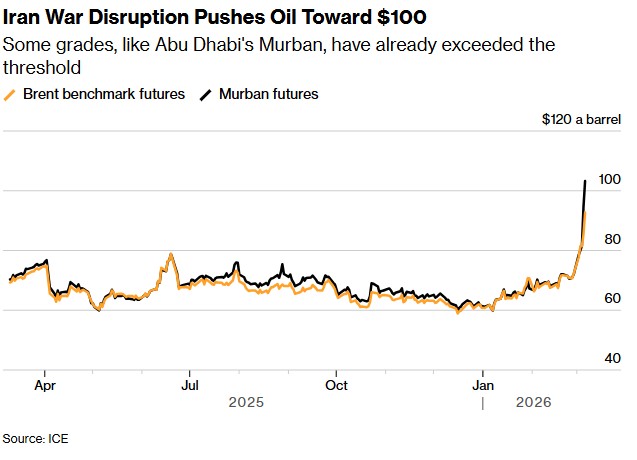

We could see two things happen quickly. 1: More sanctions lifted from Russian oil quickly, and a stabilization through the U.S. Treasury, and 2: Short-term spikes to over $100 as the length of the Iran conflict matters. More countries are shutting down oil, natural gas, and LNG production due to the tanker bottleneck.

Michael Tanner and Stu Turley will be covering this on the Energy News Beat Stand up today.

Summarizing the Key Analysis: Dismantling Adversarial Energy Networks

A detailed thread posted on X by user @lamps_apple on March 8, 2026, provides a comprehensive overview of how U.S. interventions in Venezuela, Cuba, and Iran have targeted a shadow alliance known as CRINK (China, Russia, Iran, North Korea). The post, framed as “Phase 2” of a strategic explanation, argues that these operations were not isolated but precision strikes against a parallel economic system designed to erode U.S. dominance. Key elements include:Shadow Economy and Yuan Settlements: Iran, Venezuela, and Russia supplied discounted oil to China via a “dark fleet” of tankers evading sanctions, with payments settled in Chinese yuan rather than U.S. dollars. This bypassed the dollar-based system, aiming to weaken the petrodollar’s global reserve status.

Critical Minerals and Supply Chains: Venezuela’s vast reserves of rare earths, lithium, and other minerals—previously dominated by Chinese investments—were highlighted as part of Beijing’s strategy to control 90% of global processing. U.S. actions have redirected these toward Western investment.

Military and Economic Impacts: The raid on Venezuelan President Nicolás Maduro, strikes on Iran’s nuclear program, and oil blockade on Cuba dismantled forward bases for Russian intelligence, Chinese surveillance, and Iranian proxies. This exposed vulnerabilities in Russian and Chinese arms exports, as their systems failed under U.S. pressure.

Broader Geopolitical Win: By severing these pipelines, the U.S. has forced China back to dollar-denominated markets, delayed the Belt and Road Initiative, and isolated North Korea. The post posits this as the realization of the “Donroe Doctrine”—swift interventions without nation-building—creating a structural reality where threats regenerate slowly, if at all.

This analysis paints a picture of energy markets as battlegrounds for great-power competition, with U.S. moves restoring dollar hegemony and market stability.

Monetary Controls on Venezuela: Oil and Critical Minerals Under U.S. Oversight

Treasury Secretary Scott Bessent has implemented stringent controls on Venezuela’s oil sector following Maduro’s capture in January 2026. The U.S. has lifted select sanctions to facilitate oil sales, but with operational oversight: proceeds are funneled into U.S.-managed accounts in Qatar, ensuring they benefit reconstruction rather than sanctioned entities.

By late February, sales approached $2 billion from 40 million barrels, handled by firms like Vitol and Trafigura.

Crucially, Treasury licenses prohibit transactions involving vessels or entities linked to China, Russia, Iran, North Korea, or Cuba, effectively severing shadow pipelines that anchored yuan settlements.

Bessent has also mobilized nearly $5 billion in frozen IMF Special Drawing Rights for economic rebuilding, convertible to dollars.

Complementing this, Interior Secretary Doug Burgum visited Caracas last week (March 4-5, 2026) to advance U.S. access to Venezuela’s critical minerals. Accompanied by representatives from over two dozen American mining firms, Burgum secured commitments from Acting President Delcy Rodríguez for mining law reforms and security assurances against guerrilla threats in mineral-rich areas like the Orinoco Mining Arc.

This includes deposits of coltan, rare earths, lithium, and gold—key to breaking China’s 90% dominance in global processing.

The visit aligns with a $12 billion U.S. critical minerals stockpile initiative, emphasizing Venezuela as a Western Hemisphere alternative to Beijing’s supply chains.

These controls echo President Trump’s response to U.K. Prime Minister Keir Starmer’s criticisms. When Starmer questioned whether U.S. actions in Venezuela violated international law or lacked a coherent plan, Trump reportedly pointed to the swift dismantling of Maduro’s regime as evidence of his strategy’s effectiveness, quipping, “Have you seen Venezuela?”

Starmer, while affirming support for international law and denying U.K. involvement, avoided outright condemnation, highlighting the operation’s success in ending Maduro’s rule without broader escalation.

The Iran Impact on Oil Markets

Sanctions on Iran’s oil industry, primarily led by the United States and reinforced by international measures like UN snapback mechanisms, have profoundly shaped the country’s economy, energy production, and global trade dynamics. These restrictions, reimposed in 2018 after the U.S. withdrawal from the Joint Comprehensive Plan of Action (JCPOA), target Iran’s energy exports to curb funding for its nuclear program, regional activities, and other adversarial behaviors. Below, I break down the key impacts based on recent data and trends as of early 2026.1.

Direct Effects on Iran’s Oil Production and Exports

Export Volume Reductions: Following the 2018 reimposition of U.S. sanctions, Iran’s oil exports plummeted by over 60% from pre-2018 levels of around 2.2 million barrels per day (mbpd) to a low of about 0.4 mbpd in 2020.

By 2025, however, Iran demonstrated resilience through evasion tactics, stabilizing exports at approximately 1.5-1.6 mbpd, with peaks reaching 2.15 mbpd in October 2025.

This recovery relied on discounted sales to China (which buys over 90% of Iranian oil), shadow fleets, and deceptive shipping practices.

Revenue Losses: Oil accounts for roughly 25% of Iran’s GDP and a significant portion of government revenue.

The sanctions have led to annual losses in the tens of billions of dollars, with exports sold at steep discounts ($8-10 per barrel below Brent crude in late 2025).

In October 2025 alone, exports generated $3.9-4.2 billion in gross revenue, but at reduced margins due to evasion costs.

Production Trends: Iran’s crude oil production averaged around 3.15 mbpd in mid-2025, the highest since 2018, but sanctions limit investment in infrastructure, deterring foreign partnerships and capping long-term growth.

|

Metric

|

Pre-2018 Levels

|

Post-Sanctions Low (2020)

|

2025 Average/Peak

|

|---|---|---|---|

|

Oil Exports (mbpd)

|

~2.2

|

~0.4

|

1.5-1.6 / 2.15 (Oct)

|

|

Production (mbpd)

|

~3.8

|

~2.0

|

~3.15 (Aug peak)

|

|

Revenue Impact

|

Baseline

|

-60-80% drop

|

$3.9-4.2B/month (discounted)

|

2. Economic and Domestic Impacts on IranCurrency and Inflation Crisis: The rial has depreciated dramatically, fueling hyperinflation (often exceeding 40%). Reduced oil revenues force the government to print money or borrow from the central bank, creating a vicious cycle of economic instability.

Sanctions are estimated to account for about half of Iran’s economic collapse, exacerbating issues like high unemployment and poverty.

Government Budget and Social Programs: With oil revenues funding up to a quarter of the budget, cuts have led to reduced subsidies on fuel and social services, potentially eroding public support for the regime.

This has also limited funding for military and proxy activities, though Iran continues to prioritize them.

Humanitarian Toll: Sanctions have crippled access to global finance, making imports of essentials like medicine and food more expensive, indirectly affecting civilian livelihoods.

Critics argue this has “destroyed” ordinary Iranians’ lives, despite U.S. claims of targeting the regime.

3. Global Oil Market and Geopolitical RamificationsPrice Volatility: Disruptions, such as reduced tanker traffic through the Strait of Hormuz (down 92% in some reports), can spike global crude prices.

However, U.S. shale production and LNG exports have helped cap Brent prices, mitigating broader supply shocks.

Fears of escalation, like U.S. strikes on Iranian facilities, have caused overnight price surges.

Enforcement Challenges and Evasion: Despite U.S. designations of over 50 entities and vessels in 2025, Iran’s “dark fleet” and Chinese teapot refineries continue to enable exports.

The UN snapback mechanism (triggered in 2025) increases costs for shipping, insurance, and finance but is unlikely to drop exports below 1.0-1.2 mbpd without stricter enforcement on China.

Broader Geopolitical Effects: Sanctions have isolated Iran financially, with the FATF blacklisting in 2020 compounding issues.

They also built up frozen assets abroad, used as leverage in past nuclear talks.

Recent U.S. actions under the Trump administration aim to further sever these lifelines, exposing enablers like Chinese terminals and UAE shippers.

4. Resilience and Future Outlook

Iran has adapted by deepening ties with non-Western buyers, using alternative payment systems, and expanding its shadow network. While sanctions have undeniably weakened the economy—contributing to a “collapsed” state per some analyses—they have not fully halted exports.

Escalations, such as the 2025 Israel-Iran conflict, could intensify impacts, potentially reducing revenues to $45-60 million daily if exports fall further.

For global markets, this means ongoing risks of supply disruptions but also opportunities for U.S. energy dominance to stabilize prices.

These impacts highlight sanctions as a double-edged tool: effective in pressuring Iran economically but resilient against full compliance due to evasion strategies. For energy stakeholders like podcast hosts, monitoring enforcement on China’s role will be key to predicting future trends.

Rolling Out the Monetary System: Targeting Dark Fleets and Stabilizing Trade

The Venezuela model infers a broader U.S. monetary rollout aimed at global oil markets. By prohibiting sanctioned vessels in Venezuelan trades, the U.S. is extending pressure on the “dark fleet”—a shadow network of aging tankers using deceptive practices like AIS spoofing and flag-hopping to evade sanctions on Russian, Iranian, and formerly Venezuelan oil.

This fleet, estimated at over 1,300 ships (10% of global tankers), facilitates evasion and funds adversarial regimes.

To counter this, the Trump administration launched a $20 billion reinsurance program through the U.S. International Development Finance Corporation (DFC) in early March 2026, amid disruptions in the Persian Gulf from the Iran conflict.

This provides political risk insurance and naval escorts for legitimate tankers, filling gaps where private insurers have withdrawn due to war risks.

By offering affordable coverage tied to U.S. compliance, it sidelines dark fleets, which face higher sanctions risks and lack access to this protection.

Recent actions, like delisting a sanctioned tanker after compliance, demonstrate selective enforcement to encourage legitimate trade.

This system rolls out through phased Treasury guidance, international coordination (e.g., with the EU on maritime bans), and integration with existing sanctions frameworks.

It cuts dark fleet funding by raising operational costs—war-risk premiums have surged from 0.2% to over 1% of vessel value—and disrupting payments via financial institutions wary of U.S. penalties.

Potential to End the War in Ukraine

These market changes could accelerate an end to the Ukraine war by eroding Russia’s oil revenues, which fund up to 50% of its military budget.

Ukraine’s drone strikes have damaged 38% of Russia’s refining capacity, causing domestic shortages and a 26% export drop in September 2025.

U.S.-backed insurance and sanctions amplify this by targeting Russia’s dark fleet reliance, forcing sales at discounts and reducing war chest inflows.

A peace deal could normalize Russian supplies, narrowing discounts and rerouting exports, but the interim pressure—combined with low gas exports and economic strain—may push Moscow to negotiate.

Recent talks, including U.S.-Russia discussions, suggest progress; unwinding sanctions post-deal would stabilize global prices below $60/barrel, easing inflation while rewarding peace.

Saudi Arabia and OPEC: Partners in Strengthening Markets and the Dollar

Saudi Arabia and OPEC play a pivotal role in these shifts, coordinating to maintain market share and support the U.S. dollar. Despite rumors of petrodollar erosion, Saudi oil remains predominantly dollar-denominated, with the riyal pegged to the USD and revenues recycled into U.S. Treasurys.

In 2024, Saudi Arabia earned $179 billion in oil exports, 33% of OPEC’s total.

OPEC+ has hiked output (e.g., 137,000 bpd in October 2025) to counter oversupply fears, boosting Saudi market share while aligning with U.S. calls for lower prices.

This builds political capital, as seen in arms deals and investments totaling $600 billion.

By stabilizing prices and resisting full yuan shifts (despite some diversification), Saudi Arabia reinforces the petrodollar, countering CRINK’s de-dollarization efforts.

Future cooperation could include joint stockpiles or production pacts to secure energy for peace, ensuring the dollar’s primacy in oil trades.

These transformations signal a proactive U.S. approach: leveraging energy markets for geopolitical gains, from Venezuela’s revival to Ukraine’s resolution. As oil and gas evolve toward stability, the U.S. dollar stands fortified, potentially ushering in an era of peace through economic strength. Through monetary controls, the United States will be able to effectively cut down on sanctions around the world by working with Saudi Arabia and OPEC to examine global oil markets. Once the proxy fighters and narco terrorists are removed from the oil and even gas pipelines, the world will be a safer place.

This is not about Iran. This is about the global and economic realignment away from China. For too long, we have seen the UK, China, and other countries align against the United States. The key for Americans is what to do once President Trump realigns the world.

On a side note, we cannot let the necos ruin the peace that President Trump is trying to bring to the table. It appears that our Congress is part of the problem by not passing something as simple as voter ID. Who are they actually answering to? It does not appear that they care about the 80% of Americans who want voter ID.

Sources: arabcenterdc.org, reuters.com, eia.gov, cnbc.com, spglobal.com, insurancenewsnet.com, thehill.com, X by user @lamps_apple, stimson.org, middleeasteye.net, congress.gov

We covered this and 6 other stories on the Energy News Beat Stand Up Below:

1.The Oil and Gas Markets are Changing for Peace and Supporting the US Dollar

4.Russia Following the Money: Shifting Gas and Oil Sales to Asia

5.The U.S. Merchant Marine Fleet Needs an Update

6.Iran-Linked Ships Transit as Others Wait for Insurance

7.US Oil Rig Count UP as WTI Moves UP to $92.21

Get your CEO on the #1 Energy Podcast in the United States: https://energynewsbeat.co/energy-news-beat-media-kit/

Is oil and gas right for your portfolio? https://energynewsbeat.co/invest/