The global energy markets are in the midst of a historic shock. As the 2026 Strait of Hormuz crisis—triggered by the U.S.-Israel conflict with Iran—enters its fourth month, roughly 20% of the world’s seaborne oil and 20% of LNG flows have been disrupted. Prices spiked above $100 per barrel (peaking near $126), with Brent briefly hitting records not seen in years. Yet even as diplomats discuss ceasefires, one thing is becoming crystal clear: when the shooting stops, oil and LNG trading will never revert to the pre-war status quo.

In a wide-ranging interview yesterday on The Mario Nawfal Show, Goldman Sachs veteran and Abaxx Commodity Exchange Director Jeffrey Currie described the situation as “Oil’s Perfect Storm.” Hormuz closed, Gulf infrastructure bombed, Red Sea risks escalating, inventories draining at 5 million barrels per day, and seasonality flipping from a tailwind to a headwind this summer. Currie warned of a 10–11 million bpd effective supply shock—the largest in history—and cautioned that markets are underpricing the physical reality. “This summer is going to be a really tough one,” he said, pointing to Cushing tank bottoms, U.S. SPR integrity limits, and China’s strategic flexibility via EVs and stockpiles.

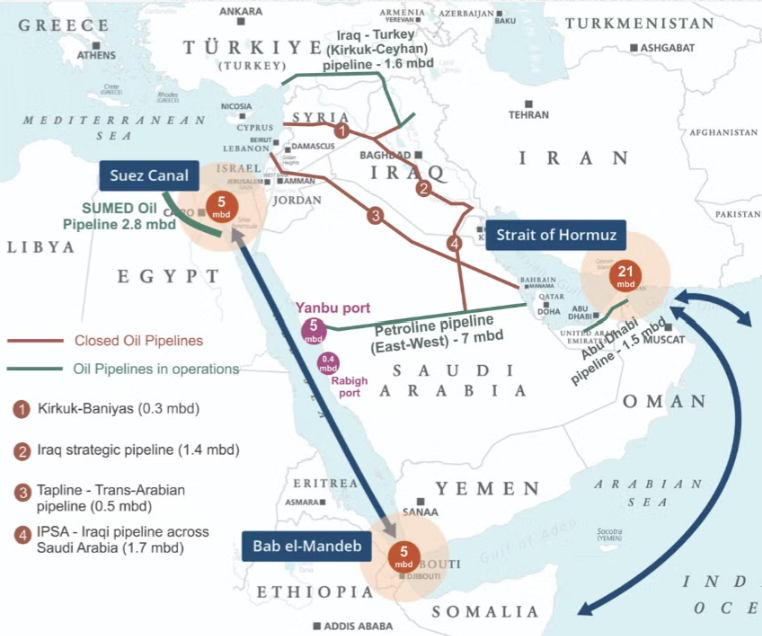

The OilPrice.com analysis published today echoes this view in stark terms: “Post-War Oil Trade Could Look Nothing Like It Did Before Hormuz.” Persian Gulf exporters are racing to make bypasses permanent. The era of single-chokepoint dependence is ending.

Pipeline Bypass Extensions: The New Arteries of Global Trade

Gulf producers learned the hard way that 20 million barrels per day cannot rely on a 21-mile-wide strait forever. Existing bypass pipelines (Saudi Arabia’s Petroline to the Red Sea and the UAE’s Habshan-Fujairah line) currently cover less than 30% of normal Hormuz flows. But major expansions are now accelerating.

UAE’s West-East Pipeline: Abu Dhabi National Oil Co. (ADNOC) has fast-tracked construction. Nearly 50% complete as of May 2026, the project will double export capacity through Fujairah on the Gulf of Oman by 2027. Crown Prince Sheik Khaled bin Mohamed bin Zayed directed the acceleration to “meet global demands” and secure exports against future disruptions.

Saudi and Iraqi moves: Riyadh is expanding Red Sea outlets, while Iraq is pushing to extend the Kirkuk-Ceyhan line and rehabilitate southern routes. Gulf states are mulling entirely new inland pipelines.

These are not temporary workarounds. They represent a structural shift: more crude and LNG will move by pipeline to eastern ports, bypassing Hormuz entirely. Tanker routes will shorten for some buyers, lengthen for others, and insurance models will permanently price in chokepoint risk. LNG exporters like Qatar are already exploring rail and alternative shipping options post-crisis.U.S. natural gas pipeline capacity is also surging—44.9 Bcf/d of new projects slated for 2026–2027, mostly in Texas and Louisiana—to feed LNG exports and domestic demand. This bolsters North America’s role as a swing supplier in a fragmented market.

Strategic Reserves: The Great Diversification Race

The crisis has exposed the fragility of just-in-time energy. In response, nations are not only releasing reserves—they are racing to build bigger ones.

China holds the world’s largest strategic inventories (~1.4 billion barrels, including commercial stocks as of late 2025) and continues aggressive filling. Its hybrid government-commercial model gives Beijing unmatched flexibility.

The U.S. released 172 million barrels as part of the IEA’s record 400-million-barrel coordinated drawdown but has committed to replenishing and expanding.

Japan, India, South Korea, and EU nations (Germany, France, Spain, Italy) are expanding or replenishing stocks. Even non-traditional players in Africa and Asia are studying SPR models.

As more countries build 90–200+ day reserves, buying patterns will change permanently. Importers will lock in long-term contracts with diversified suppliers to replenish stockpiles—favoring pipeline-fed volumes from the Gulf, U.S. LNG, Brazilian pre-salt, and Canadian oil sands. Trading blocs are forming: BRICS-aligned buyers (China, India, Russia partners) versus traditional OECD importers. Who you buy from will increasingly signal geopolitical alignment, not just price.

Price Outlook: From Spike to New Normal

During the crisis, physical markets have traded far tighter than paper futures. Currie notes inventories are being drawn to cover the shock while seasonality (summer driving/cooling + potential El Niño) turns hostile. Cushing could hit tank bottoms soon, risking WTI spikes.

Post-war scenarios:

Rapid reopening + deal: Prices could drop sharply ($20+ initially) toward $65–$70/bbl as oversupply returns temporarily. But Currie warns long-dated oil must reprice structurally higher due to rebuilt infrastructure costs and diversified (less efficient) routes.

Prolonged or partial disruption: Summer 2026 pain intensifies. $100–$130+ remains possible if Red Sea or additional infrastructure is hit.

New baseline: Higher baseline volatility, elevated freight/insurance costs, and a premium for “secure” (non-Hormuz) barrels. LNG spot prices will stay structurally higher in Asia/Europe until new supply and terminals come online.

The “abundance illusion” Currie referenced—flooding markets with SPRs while ignoring physical constraints—is over.

Hard assets (oil, gas, metals) regain their halo.

A New Map for Energy Trade

Post-war oil and LNG trading will feature:

More pipelines, fewer tankers through Hormuz.

Diversified suppliers and strategic reserve-driven contracts.

Emerging trading blocs shaped by security, not just economics.

Higher structural costs and volatility are priced in.

And in Asia, Africa, and the Americas, drilling programs are expanding with a vengeance.

OPEC quietly lifted more oil production quotas, but it won’t matter until the pipelines are open. Countries

The Hormuz crisis didn’t just disrupt supply—it rewrote the rules. As Currie put it, the grasshoppers partied while the ants (China and others) built optionality for decades. The world is waking up.

Energy News Beat will continue tracking these shifts daily. The post-war energy order is already under construction.

Appendix: Sources and Links

- Mario Nawfal Interview with Jeffrey Currie (June 7, 2026): https://x.com/MarioNawfal/status/2063680522971193553

- “Post-War Oil Trade Could Look Nothing Like It Did Before Hormuz,” OilPrice.com: https://oilprice.com/Energy/Crude-Oil/Post-War-Oil-Trade-Could-Look-Nothing-Like-It-Did-Before-Hormuz.html

- UAE West-East Pipeline acceleration (Reuters, May 15, 2026): https://www.reuters.com/business/energy/uae-accelerate-oil-pipeline-project-help-bypass-hormuz-2026-05-15/

- UAE pipeline 50% complete (CNBC, May 20, 2026): https://www.cnbc.com/2026/05/20/uae-pipeline-strait-hormuz-iran-war-oil.html

- Hormuz Bypass Capacity Limits (Forbes, March 23, 2026): https://www.forbes.com/sites/guneyyildiz/2026/03/23/hormuz-bypass-capacity-falls-catastrophically-short-the-pipelines-cover-less-than-30/

- EIA on U.S. Gas Pipeline Additions (May 26, 2026): https://www.eia.gov/todayinenergy/detail.php?id=67707

- Global Strategic Reserves (EIA, April 20, 2026): https://www.eia.gov/todayinenergy/detail.php?id=67504

- IEA Coordinated Release & U.S. SPR (U.S. Dept. of Energy, March 11, 2026): https://www.energy.gov/articles/united-states-release-172-million-barrels-oil-strategic-petroleum-reserve

Energy News Beat – Unfiltered Energy Intelligence. Subscribe for daily updates.