In the most complex mix of geopolitical supply disruptions in modern history—over 100 days into the US-Iran conflict involving strikes, Hormuz transit risks, and broader Middle East tensions—the United States and China are effectively supplying a significant portion of global oil demand through their strategic and commercial reserves. They are doing so via sharply contrasting strategies.

The US is releasing oil from its Strategic Petroleum Reserve (SPR) directly into the global market. China is drawing down its massive stockpiles (strategic plus commercial) to meet domestic refining needs while largely avoiding high-priced spot purchases. This “tale of two SPRs” is capping price spikes in futures markets but masking deepening physical tightness that could unwind rapidly.US SPR: Rapid Drawdown to Supply the World

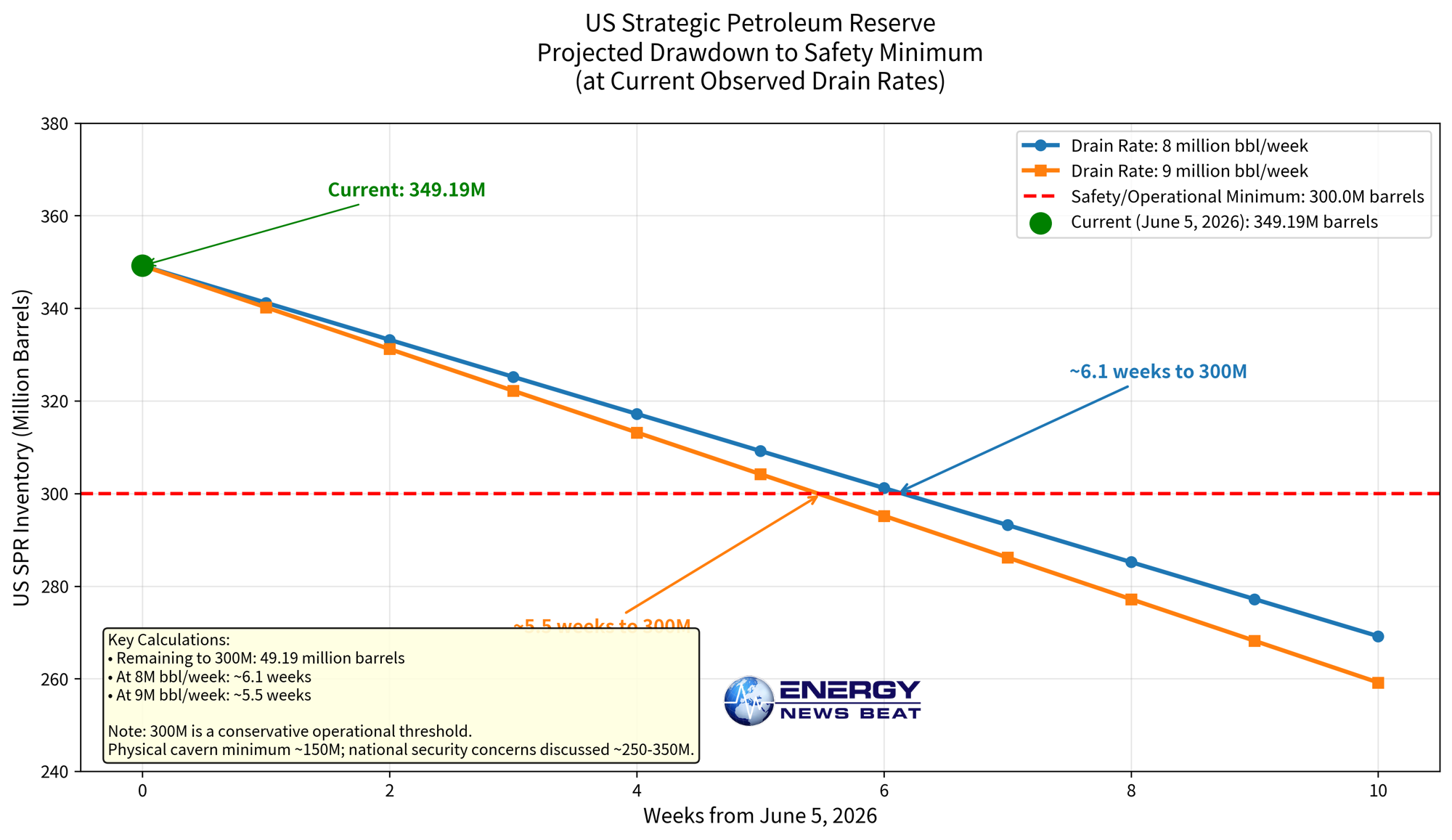

The US SPR stood at approximately 349.2 million barrels as of June 5, 2026 (down from ~415 million barrels pre-release in March). This follows President Trump’s authorization of a 172 million barrel release (part of a larger IEA-coordinated 400 million barrel global effort) to mitigate price spikes from the Iran conflict.

Recent weekly draws have averaged ~8 million barrels per week (roughly 1.1–1.3 million barrels per day), with one week showing a ~7.93 million barrel decline.

Calculation at current drain rate to a safety minimum:

Current level (June 5, 2026): 349.19 million barrels.

Assumed safety/operational minimum: 300 million barrels (a conservative threshold near or below recent multi-year lows; operational concerns arise well above the absolute physical cavern floor of ~150 million barrels, with national security/functional buffers discussed around 250–350 million barrels).

Remaining to 300 million barrels: ~49.19 million barrels.

At 8 million barrels/week: ~6.1 weeks.

At 9 million barrels/week (recent peak observed rate): ~5.5 weeks.

At the current pace, the SPR could approach or breach commonly cited critical low levels within 5–7 weeks (by mid-to-late July 2026), assuming the release program continues at observed rates. The maximum technical drawdown capability is 4.4 million barrels per day, but actual releases have been more measured.

This drawdown is explicitly intended to supply the global market and ease price pressure amid Middle East disruptions.

China’s Opposite Approach: Living Off Stockpiles

China holds the world’s largest combined strategic and commercial oil inventories—estimated at ~1.3–1.4 billion barrels as of late 2025/early 2026 (government SPR portion ~360 million barrels; commercial/refinery stocks making up the bulk). It added aggressively in 2025 at an average ~1.1 million barrels per day.

In stark contrast to the US:

Sinopec (China’s largest refiner) bought zero Saudi crude for a second straight month.

Saudi July allocations to China: only 12 million barrels (~387,000 barrels per day)—a record low.

Aramco cut its Official Selling Price (OSP) by $ 6 per barrel, yet Chinese buyers largely stayed away because prices remain well above pre-war levels.

China’s May crude imports hit a decade low; refiners are cutting runs at a loss.

China is deliberately drawing down its own stockpiles rather than paying “war premiums.” This buyer strike removes significant demand from the physical market, helping cap rallies. However, these inventories are finite. When Beijing eventually must re-enter the market for secure barrels (recent high-level meetings between China’s energy administration and Aramco officials signal this tension), it could trigger the next leg higher in prices.

Same tool (reserves), opposite strategies: The US floods the global market via SPR releases; China insulates itself by self-supplying from pre-built buffers.

Price Impact and the Paper vs. Physical Disconnect

Despite the most complicated supply disruption mix in history (Iran production risks, Hormuz concerns, broader regional effects), benchmark futures prices have remained relatively contained. As of June 11, 2026, Brent traded around $92/barrel and WTI near $89–91/barrel—far below what many expected given 100+ days of conflict.

Physical markets told a different story earlier in the conflict, with dated Brent and spot grades surging to record premiums (sometimes $30–60+ above futures). By early June, physical premiums had “fizzled out” as refineries recalibrated buying patterns and abating immediate shortfall fears took hold, according to Bloomberg reporting.

However, a notable paper (futures) vs. physical disconnect persists in analyses:Massive crude inventory draws (including SPR and Chinese commercial stocks) are occurring with muted price response.

Traders and observers (including economist Chris Martenson) highlight “wild trades” on the futures tape—e.g., sudden sales of 6 million barrels in a single minute causing price drops with limited follow-through reaction. This has fueled claims of market capture, government-leaning interventions (direct or indirect shorting to manage inflation), or simply overwhelming supply from reserves masking underlying tightness.

The Bloomberg piece notes physical crude grades ripped higher early in the war before easing, with few signs yet of a strong resurgence in premiums.

Who Wins If the Economists Are Right?

If analysts highlighting the unsustainable disconnect (physical tightness masked by reserve draws and possible futures-market dynamics) are correct, the current price suppression is temporary. Key triggers for a sharp re-rating include:

US SPR approaching operational lows (weeks away at current rates).

Chinese stockpiles are running low enough to force a return to the market.

Any escalation or prolonged Hormuz disruption would reduce effective supply further.

Physical delivery realities are catching up as commercial inventories tighten globally.

Potential winners:

Physical crude holders and producers are able to deliver real barrels at higher realized prices.

Those positioned for the eventual re-entry bid from China or a post-SPR exhaustion squeeze.

Long-term bulls who viewed the futures suppression as artificial.

Potential losers:

Consumers and downstream industries are facing a delayed but sharper price spike.

Futures shorts or those betting on prolonged containment.

Policymakers relying on reserve releases as a durable buffer (the SPR is not infinite, and refilling takes time—years at realistic rates).

This is not a simple supply/demand story. It is a high-stakes interplay of government reserve policy, buyer strikes, futures-market dynamics, and finite buffers colliding with real-world supply risks. The “tale of two SPRs” has bought time and moderated prices so far—but the clock is ticking on both the US drawdown and China’s stockpiles.

- Jack Prandelli X post (June 11, 2026): https://x.com/jackprandelli/status/2065002066091622441

- Mario Nawfal X post / Chris Martenson clip (June 11, 2026): https://x.com/MarioNawfal/status/2064955790876705242

- Bloomberg: “Physical Oil Markets Are Floundering Despite 100 Days of War” (June 10, 2026): https://www.bloomberg.com/news/articles/2026-06-10/physical-oil-markets-are-floundering-despite-100-days-of-war

- US SPR levels and releases: YCharts/EIA data (June 5, 2026: 349.19M barrels); Fortune (June 10, 2026); DOE announcements (March 2026 172M barrel release).

- China inventory estimates: EIA (April 2026); Oxford Energy Institute and other analyses (2025–2026 builds ~1.1M bpd).

- Oil prices (June 11, 2026): Trading Economics, CME, EIA spot data (~Brent $92, WTI ~$89–91).

- Additional context: Multiple reports on physical vs. futures disconnect (April–June 2026 analyses from Energy Aspects, Rystad, WSJ, etc.); API and industry commentary on SPR operational thresholds.

All information was cross-checked against primary data sources (EIA, DOE, market reports) and contemporaneous commentary as of June 11, 2026. Market conditions evolve rapidly—reserve levels, draw rates, and geopolitical developments should be monitored closely.