This risks a tight winter as the injection season winds down, with inventories projected to be just 76% full by late October.

According to a Financial Times report citing industry analysis (primarily Wood Mackenzie), Europe faces the prospect of entering the 2026/27 heating season with its lowest natural gas storage levels in at least 15 years.

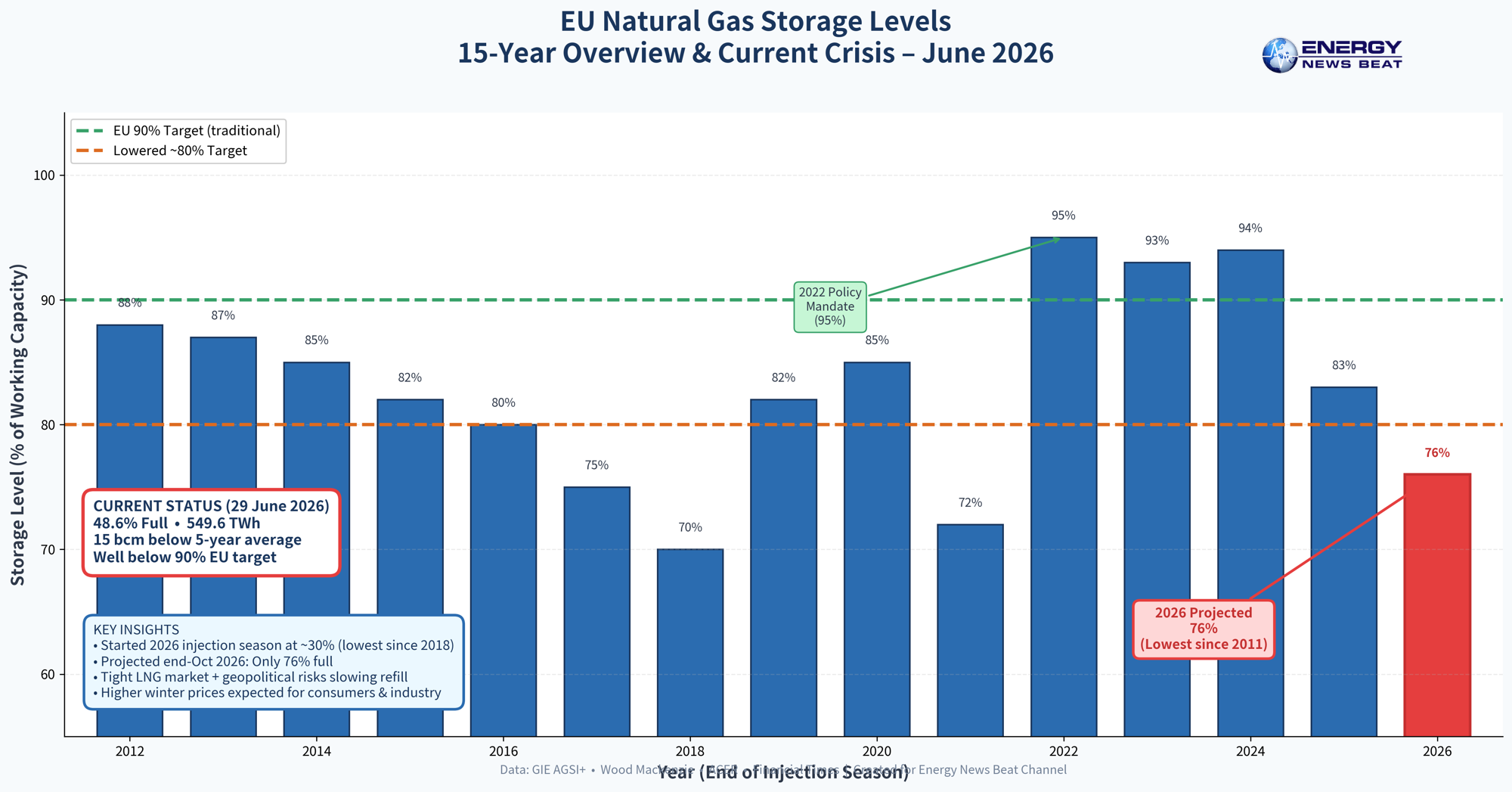

Current Storage Levels (as of late June 2026)As of June 29, 2026, EU aggregate storage stood at 48.62% full (549.6 TWh out of ~1,130.5 TWh working capacity), according to Gas Infrastructure Europe (GIE) AGSI+ data.

This is significantly below the five-year average (roughly 15 bcm lower as of mid-June) and about 10.6 bcm below the same point last year. Europe entered the 2026 injection season (April–October) with unusually low stocks — around 31 bcm or ~28–30% full by early April — following high withdrawals during the 2025/26 winter.

Historical trend (end of injection season, late Oct/Nov 1 % full, approximate based on GIE/AGSI+, EIA, ACER, and market reports):

- Pre-2022 average (2011–2021): ~80–89%

- 2022: ~95% (policy-driven surge after Russian supply cuts)

- 2023–2024: 90–95% (strong refill amid high prices and mandates)

- 2025: Lower, around 83% by early October (after a harsher winter)

- 2026 projection: ~76% — the lowest since at least 2011

The post-2022 highs were exceptional due to mandatory filling targets (originally aiming for 90% by Nov 1). Levels are now reverting lower amid structural supply changes and a tight global LNG market.

Will Europe Secure Enough LNG/Natural Gas for Winter?

It will be challenging and likely expensive.

Europe has largely replaced lost Russian pipeline gas with LNG and increased flows from Norway, Algeria, and Azerbaijan. However, the injection season faces headwinds:Tight global LNG market — Recent geopolitical tensions (US-Israel-Iran conflict) disrupted shipments through the Strait of Hormuz (historically ~20% of global LNG supply) and reduced output from Qatar and the UAE.

Current injection pace points to only ~75–78% full by end-October if trends continue — below comfortable levels and short of the traditional 90% target (some flexibility or lowered effective targets have been discussed).

Main LNG suppliers to Europe (2025–early 2026 data):

United States: Dominant supplier, accounting for ~57–63% of EU LNG imports (on track for two-thirds in 2026). US exports have flexibility and are ramping up.

Russia: Still ~13–17% of LNG imports (via existing terminals), though pipeline flows are minimal and a full ban on Russian LNG is slated for January 2027.

Others: Nigeria, Qatar (reduced), Trinidad & Tobago, etc.

Europe can attract more US LNG with higher prices (the market is global and price-sensitive). However, competition from Asia and any further Middle East disruptions could limit volumes. Pipeline gas from Norway remains the largest overall supplier, supplemented by Algeria and Azerbaijan.

Analysts note that reaching even 80% would require sustained strong LNG inflows. A mild winter or demand destruction (industrial slowdown) could ease pressure, but a cold snap would expose the thinner buffer.

What This Means for Consumers

Higher energy costs are the most immediate impact. TTF (Dutch Title Transfer Facility) benchmark prices — the key European reference — stood around 43–44 EUR/MWh in late June 2026, with winter contracts trading at a premium.

- Households: Higher heating bills this winter, especially in gas-dependent countries like Germany, Italy, the Netherlands, and France.

- Energy poverty risks could rise.

- Industry: Increased costs for manufacturing, chemicals, fertilizers, and power generation — potentially leading to reduced output or relocation pressures.

- Electricity prices: Gas often sets marginal power prices in Europe, so knock-on effects are likely.

Governments may intervene with subsidies or demand-reduction measures, as seen in 2022, but the fiscal space varies.

What This Means for Investors

Mixed but generally supportive for upstream and LNG players; caution for European downstream.Bullish: US LNG exporters (e.g., Cheniere, others expanding capacity) — higher European demand and prices support exports. European storage operators and flexible suppliers could benefit. LNG shipping and regasification infrastructure plays.

Cautious/volatile: European utilities and energy-intensive industries face margin pressure if costs cannot be fully passed through. Broader equity markets could see volatility from energy price spikes.

Opportunities: Companies positioned in US LNG, Norwegian gas, or demand-side flexibility (e.g., efficiency tech, renewables acceleration).

Longer term, this reinforces Europe’s push toward diversification, renewables, efficiency, and (controversially) nuclear or other baseload options.OutlookEurope is not facing an immediate physical shortage, but the buffer is thinner than in recent years. Success depends on:

- Continued strong US LNG deliveries

- Mild-to-normal weather

- No major new supply disruptions

- Effective demand management

Prices are likely to stay elevated or rise further into winter, acting as the main balancing mechanism. The situation highlights ongoing vulnerabilities in Europe’s post-Russian-gas energy system.

Appendix: Sources and Links

- Financial Times: “Europe risks starting winter with gas stocks at 15-year low” (June 2026) — https://www.ft.com/content/06304ad6-3841-4d5a-933a-6e750f536eaf

- GIE AGSI+ (current storage data): https://agsi.gie.eu/

- Wood Mackenzie analysis (via multiple reports referencing end-Oct 2026 forecast)

- Energy Policy Columbia / various analyses on 2026 injection start levels

- IEEFA: Europe LNG import sources (US dominance) — https://ieefa.org/

- Bruegel European natural gas imports dataset

- ACER Gas Key Developments winter reports

- Trading Economics / ICE for TTF prices

- Consilium/EU infographics on storage and imports

All data current as of June 30, 2026. Storage and market conditions can shift rapidly with weather, geopolitics, or new supply data. For the latest figures, check GIE AGSI+ directly.