As the Strait of Hormuz reopens following the mid-June U.S.-Iran ceasefire and sanctions waiver on Iranian oil sales (valid until August 21, 2026), Middle East crude flows are recovering, and tanker traffic is picking up. However, a key market twist has emerged: Asian refiners, who aggressively sourced non-Middle Eastern crude during the disruption, now have excess Middle East cargoes and are offering them to the U.S. West Coast — including rare deliveries to California and Hawaii.

This redirection signals easing immediate supply pressure in Asia but also underscores lingering supply chain frictions from the 2026 Hormuz crisis.

Background: The 2026 Hormuz Disruption

Tensions escalated in late February 2026, leading to a sharp drop in traffic through the Strait of Hormuz — the critical chokepoint for roughly 20% of global seaborne oil trade (mostly destined for Asia). Normal daily transits averaged around 130–140 vessels. During the peak disruption, tanker movements collapsed by as much as 92%, with flows reduced to a trickle of 5–10 ships per day or fewer at times.

Asian refiners scrambled for alternatives from the U.S., Russia, West Africa, and Latin America. This drove a surge in U.S. crude exports and sent waves of empty Very Large Crude Carriers (VLCCs) across the oceans to the U.S. Gulf Coast.

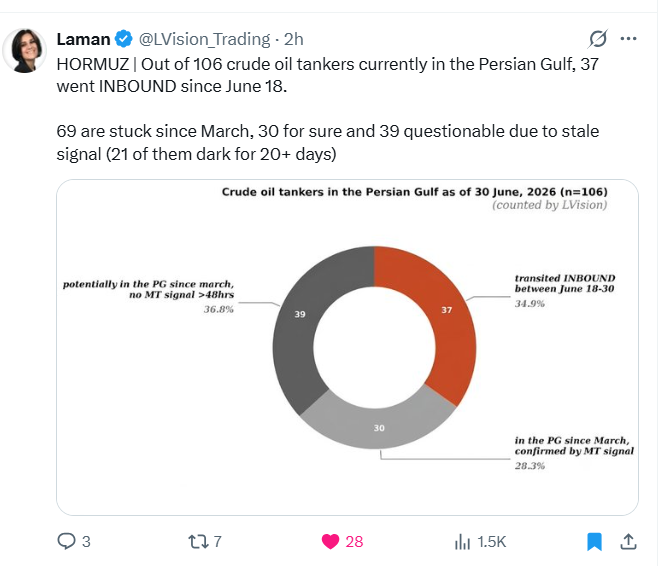

Hormuz Traffic Recovery Underway

Since the U.S.-Iran deal around June 18, 2026, traffic has rebounded from near-standstill levels:

Pre-war average: ~138 vessels per day.

Post-deal examples: 42 commodity carriers on one recent Saturday (Kpler); 37 on another day (record since the conflict began); daily averages rising toward 20–30 transits in late June, with peaks including 55 merchant ships carrying over 17 million barrels on one Saturday (U.S. Central Command).

Tanker-specific activity: 20+ oil tankers on stronger days (highest since early June); Iranian crude loadings resuming from Kharg Island; Qatari LNG tankers returning; multiple VLCCs exiting with Saudi and other Gulf crudes.

Middle East production has rebounded to 14.6–15 million barrels per day (bpd). Iranian exports have surged, with over 25 million barrels of Iranian oil reported passing through the strait in one recent period.

Hundreds of tankers and cargo vessels remain in or near the Gulf (many stationary), and full normalization will take time due to route preferences (Iranian northern vs. Omani southern lanes), insurance, and risk assessments.

Asian Refiners Redirect Middle East Crude to the U.S.

Asian buyers secured substantial non-Middle East volumes for summer delivery during the crisis. With Hormuz flows recovering and Middle East supply rising, they now have limited need for additional spot Middle East cargoes.As a result, some Asian refiners are offering excess Middle East crude to U.S. buyers on the West Coast. This is notable because:

Hawaii had not imported Middle East crude since 2018.

California had not received it since late 2025.

U.S. inventories (Cushing and SPR) are at multi-decade lows, creating demand pull. Ironically, Asia had been a major buyer of U.S. crude earlier in 2026; now the flow is partially reversing for certain grades. WTI has traded at a premium to key Middle East benchmarks like Murban, further reducing Asia’s appetite for U.S. barrels while making redirected Middle East crude attractive for the U.S. market.

Empty Tankers and the Longer Supply Chain Problem

During the disruption, the global tanker fleet dispersed significantly. Reports documented over 100 empty tankers (including dozens of VLCCs capable of carrying ~2 million barrels each) heading to the U.S. Gulf Coast to load American crude.

With the reopening, some tankers have U-turned in the Indian Ocean to reposition toward the Middle East (e.g., vessels originally bound for Africa redirecting to Fujairah). However, not all are returning quickly. Tankers that traveled far to the U.S. or Atlantic face long ballast voyages back. Repositioning the fleet — including crew changes, insurance adjustments, and risk pricing — is a multi-week process.

Saudi Aramco and analysts have highlighted tanker repositioning as one of the biggest bottlenecks to restoring full flows. Even with Hormuz open, it can take over a month for newly loaded oil to reach end markets. Hundreds of vessels remain clustered in the region, and inbound empty tankers serve as a leading indicator of future supply.

This points to a longer-term supply adjustment problem: The crisis caused structural shifts in tanker positioning and buyer sourcing. Full reversion to pre-2026 patterns will be gradual, even as physical flows ease. Asia’s prior commitments to alternative crudes mean Middle East supply may not be fully absorbed immediately, contributing to the current redirection dynamic.

Market Implications

Near-term: Gradual increase in available Middle East barrels should ease spot market tightness in Asia and support downward pressure on prices (Brent has already reacted to recovery signals).

U.S. angle: Low inventories and redirected cargoes provide a buffer; the U.S. benefits from both strong export positioning earlier and selective imports now.

Risks: Lingering geopolitical uncertainty, mine clearance operations, and insurance premiums could keep confidence “shaky.” Any renewed tensions could quickly reverse gains.

Oil shipments are easing, but the tanker fleet’s repositioning and diversified sourcing mean the market is still working through the after-effects of the Hormuz disruption.

The biggest calls by some as a glut are totally unfounded. There is no glut. There will be more repositioning of tankers, and really getting a feel for long-term storage refilled. We are not out of the woods yet.

Appendix: Sources and Links

- OilPrice.com: “Asian Refiners Redirect Middle East Crude to the U.S. as Hormuz Flows Recover” (June 30, 2026) — https://oilprice.com/Latest-Energy-News/World-News/Asian-Refiners-Redirect-Middle-East-Crude-to-the-US-as-Hormuz-Flows-Recover.html

- Reuters: Tanker traffic through Hormuz picks up (June 22, 2026) — https://www.reuters.com/world/middle-east/shipping-slows-after-iran-says-it-has-again-shut-strait-hormuz-2026-06-21/

- BBC: Dozens of ships head through Strait of Hormuz after US-Iran deal — https://www.bbc.com/news/articles/cx23rnzdgl8o

- Bloomberg / gCaptain: Oil Tankers U-Turn, Rush to Middle East Before Hormuz Reopening (June 17, 2026)

- Kpler, Vortexa, MarineTraffic, AXSMarine, and U.S. Central Command shipping data (various June 2026 reports)

- EIA historical context on Hormuz flows (pre-2026 baseline)

- Additional coverage from CNBC, BNN Bloomberg, and Al Arabiya on traffic records post-deal

Data visualizations sourced from public tracking platforms (Kpler, MarineTraffic) and news outlets as referenced. Traffic figures are approximate and subject to AIS gaps or underreporting.Energy News Beat Channel — Tracking global energy flows in real time.