As the Iran conflict escalates with U.S. and Israeli strikes targeting Iranian energy infrastructure, the Iran-backed Houthis in Yemen have issued a stark warning: they are prepared to close the Bab el-Mandeb Strait, effectively blocking oil exports through the Red Sea. Houthi Deputy Foreign Minister Hussein al-Ezzi stated, “If Sana’a decides to close the Bab al-Mandab, then all of mankind and jinn will be utterly powerless to open it.”

This threat opens a dangerous second front in global energy chokepoints. With Iran already disrupting the Strait of Hormuz—the world’s most critical oil transit route carrying roughly 20 million barrels per day (bpd) pre-war—the Red Sea route has become Saudi Arabia’s primary alternative for keeping oil flowing to Europe and Asia. But the Houthis control the southern gateway to the Red Sea, and their past attacks (2023–2025) have already halved traffic through the Bab el-Mandeb Strait. A full blockade now would compound the crisis at the exact moment Saudi Arabia’s East-West Pipeline is operating at maximum capacity to bypass Hormuz.

The Critical Role of the Bab el-Mandeb Strait and Red Sea Route

The Bab el-Mandeb Strait, just 18 miles wide at its narrowest, connects the Red Sea to the Gulf of Aden and serves as the southern entrance for tankers heading to or from the Suez Canal. In normal times, it handles roughly 9 million bpd of oil and petroleum products. Tankers loaded at Saudi Arabia’s Yanbu port on the Red Sea must pass through Bab el-Mandeb southbound to reach Asian markets or continue north through Suez to Europe.

With the Strait of Hormuz largely offline due to the Iran war, Saudi Arabia has quadrupled crude loadings from Yanbu. The kingdom’s East-West Pipeline (Petroline) — which runs 746 miles from the eastern oil fields to Yanbu — has been restored to its full operational capacity of approximately 7 million bpd following recent damage from attacks. Of that volume, roughly 2 million bpd goes to domestic refineries on the West Coast, leaving 4–5 million bpd available for export via Yanbu terminals (practical loading capacity is estimated at 3–4.5 million bpd under current wartime conditions).

Any Houthi blockade of Bab el-Mandeb would directly strand these Red Sea exports. There is no viable short-term alternative: rerouting around the Cape of Good Hope adds thousands of miles, weeks of transit time, and massive additional fuel and insurance costs.

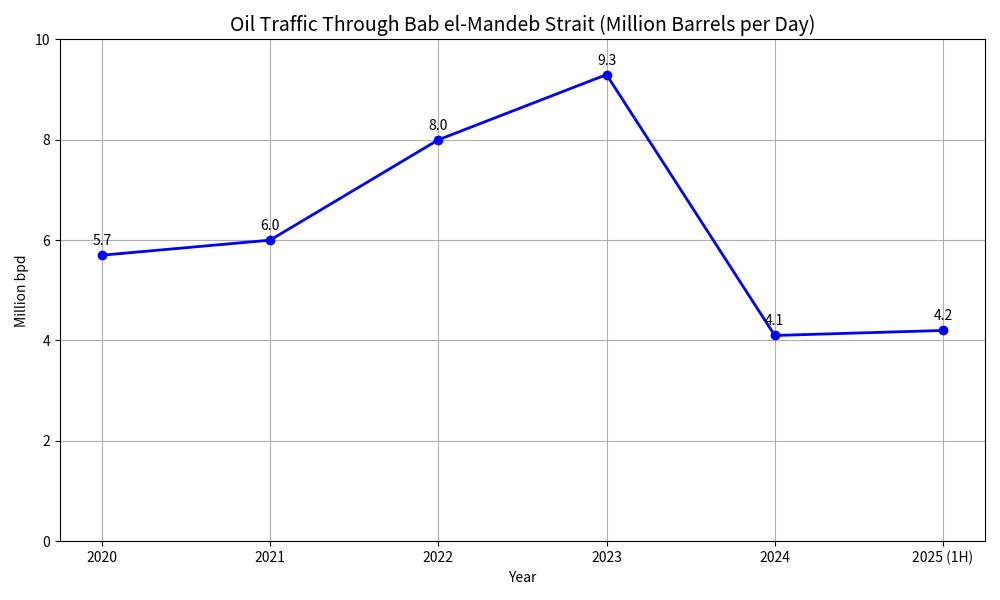

Last Five Years of Oil Traffic Through the Red Sea (Bab el-Mandeb Strait)Historical data from the U.S. Energy Information Administration (EIA) shows just how dramatically Red Sea oil flows have fluctuated — and how vulnerable they remain:

A view of current Tanker Traffic.

Bab el-Mandeb Strait Total Oil Flows (million bpd) 2020: 5.7

2021: 6.0

2022: 8.0

2023: 9.3 (pre-Houthi attack peak)

2024: 4.1 (sharp drop after attacks began)

1H 2025: 4.2

For context, the linked Suez Canal/SUMED pipeline system carried 4.9 million bpd in the first half of 2025 — also roughly half of 2023 levels.

In early 2026, the Saudi ramp-up pushed Yanbu crude exports to record levels of approximately 4.0–4.3 million bpd in March alone, helping offset Hormuz losses.

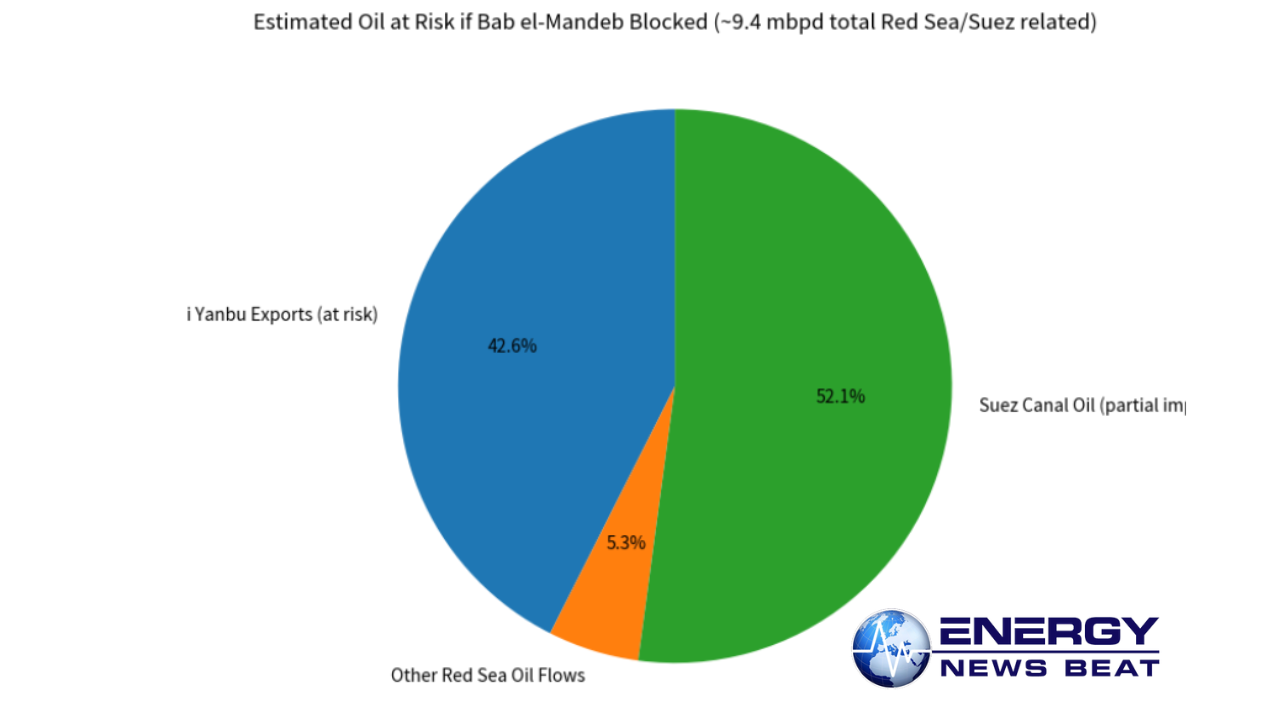

How Much Oil Is at Immediate Risk?

If the Houthis follow through and block the Bab el-Mandeb Strait:

Saudi Yanbu exports: ~4.0 million bpd (currently at or near terminal limits)

Other Bab el-Mandeb crude and product flows: ~0.2–1.0 million bpd (including remaining Russian and other volumes)

Partial Suez Canal impact: Up to 4.9 million bpd could face rerouting pressure

Total potential disruption: 4–9+ million bpd of oil and products moving through or dependent on the Red Sea route. Combined with the ongoing Hormuz crisis, this represents a historic supply shock — potentially removing 20–25% of global seaborne crude oil from efficient transit.

Impact on Already Stressed Oil Markets

Global oil markets are already reeling from the Iran war. Brent crude has surged well above pre-war levels, with analysts warning of further spikes to $140–150+/bbl if Red Sea oil exports are cut off.

Supply tightness: Europe and Asia lose quick access to Saudi barrels. Refiners will scramble for alternative crude, driving up spot prices and tanker rates.

Rerouting costs: Cape of Good Hope detours add 10–14 days and 30–50% higher bunker fuel consumption. Insurance premiums for Red Sea transits have already skyrocketed in past crises.

Downstream effects: Higher crude and freight costs will ripple into gasoline, diesel, and jet fuel prices worldwide. Asian buyers (India, China) and European refiners are most exposed.

Broader economic pressure: Inflationary shock on top of war-related disruptions, with potential knock-on effects for global GDP growth and shipping-dependent supply chains.

The East-West Pipeline running at full capacity was supposed to be Saudi Arabia’s insurance policy against Hormuz closure. Instead, it has concentrated risk in the Red Sea — now squarely in Houthi crosshairs.

What Comes Next?

The Houthis have proven they can disrupt shipping with drones, missiles, and small boats. A sustained blockade would turn the Red Sea into a no-go zone for oil tankers, forcing the world to adapt to permanently higher energy costs and longer supply lines.

Energy markets are watching closely. Any confirmed Houthi action against Yanbu-bound or Red Sea tankers could trigger an immediate price spike and renewed calls for naval protection of the route.

- EIA World Oil Transit Chokepoints (latest data): https://www.eia.gov/international/analysis/special-topics/World_Oil_Transit_Chokepoints

- OilPrice.com – “Houthis Threaten to Block Red Sea Oil Exports as the Iran War Escalates”: https://oilprice.com/Latest-Energy-News/World-News/Houthis-Threaten-to-Block-Red-Sea-Oil-Exports-as-Iran-War-Escalates.html

- Reuters – Saudi Arabia restores East-West pipeline to 7 million bpd: https://www.reuters.com/business/energy/saudi-arabia-restores-full-capacity-east-west-oil-pipeline-7-million-bpd-after-2026-04-12/

- Kpler analysis on Yanbu flows and Bab el-Mandeb: https://www.kpler.com/blog/chokepoint-risks-could-tighten-crude-supply-as-houthis-enter-the-conflict

- Bloomberg and Fortune reports on pipeline and Red Sea risks (March–April 2026)

- Al Jazeera and other regional coverage of Houthi/Iran statements

All data is current as of April 20, 2026. Markets move fast — stay tuned to Energy News Beat for updates.