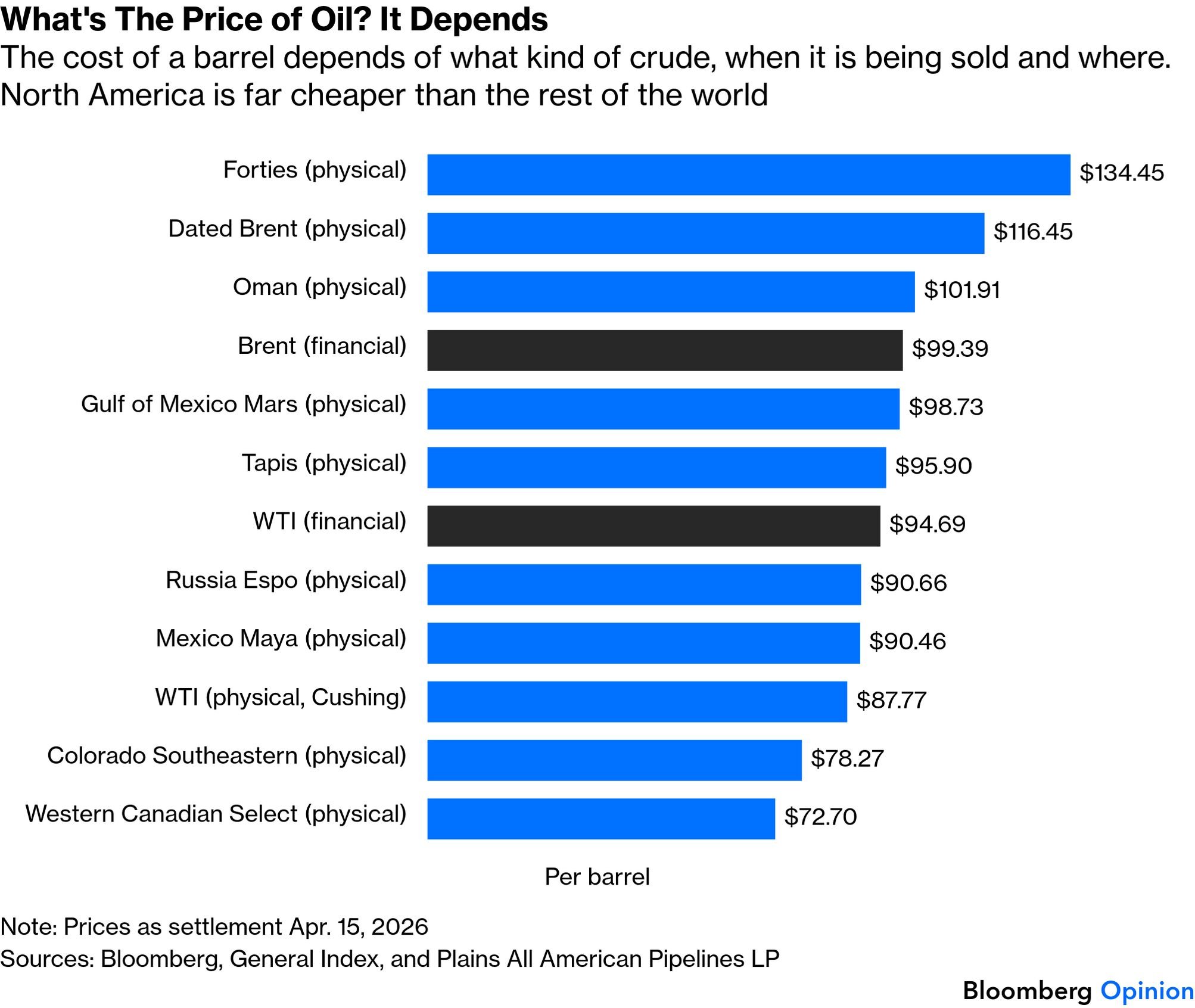

In the energy markets, there’s no single “oil price” anymore — and today’s fractured reality proves it. As highlighted in a sharp analysis posted this morning by commodity trader Jack Prandelli, the spreads tell the real story:

Forties (physical) → $134

Dated Brent (physical) → $116

Brent futures → $99

WTI → $87

Canadian crude → $72

That’s not one market. That’s fragmentation on steroids.

Paper vs. Physical: Two Completely Different Worlds“Paper” oil refers to financial contracts traded on exchanges — think Brent or WTI futures. These are what you see quoted on CNBC or Bloomberg screens. They’re liquid, standardized, and often reflect trader sentiment, hedging, and speculation about future supply and demand.“Physical” oil is the actual crude in the water or at the terminal — Dated Brent (the benchmark for real North Sea cargoes), Forties, Oman, or specific grades like those loading in Yanbu or the Gulf of Mexico. These prices are what refiners and end-users actually pay to get barrels delivered. Location, quality, logistics, and immediate availability matter far more than a futures ticker.

The massive premium on physical barrels (sometimes $30–$40 above futures) isn’t theoretical. It’s the direct result of supply getting trapped behind chokepoints. Right now, the Strait of Hormuz disruption has locked in millions of barrels in the Persian Gulf, forcing Europe and Asia to bid aggressively for whatever real crude they can secure. North American oversupply keeps WTI and Canadian grades cheap locally, while physical North Sea and Middle East grades command huge location premiums.

As Prandelli put it: “Physical barrels ≠ paper price. Location is everything. Logistics > benchmarks.” In a crisis, oil stops being global. It becomes regional, physical, and political.

This Morning’s New Risk: Houthis Threaten to Close Bab el-Mandeb

Just as markets were digesting the ongoing Hormuz mess, fresh headlines hit: Yemen’s Houthis warned they could shut the Bab el-Mandeb Strait if the U.S. (under President Trump) continues what they call “obstructing peace.” Houthi Deputy Foreign Minister Hussein al-Ezzi posted on X that if Sana’a decides to close it, “all of mankind and jinn will be utterly powerless to open it.”

The Bab el-Mandeb — the narrow chokepoint between the Red Sea and the Gulf of Aden — normally carries about 4–6 million barrels per day of oil and products heading to Europe via Suez or to Asia. It’s already been a flashpoint for Houthi attacks in prior years.

Saudi Arabia’s Pipeline Bypass — Now at Risk

Saudi Arabia has been using its East-West Pipeline (Petroline) at full capacity — 7 million barrels per day — to reroute crude from the Gulf fields to the Red Sea terminal at Yanbu. This was the kingdom’s critical workaround for the Hormuz closure, allowing roughly 5 million bpd of exports (plus domestic refinery supply) to keep flowing.

But here’s the catch: tankers loading at Yanbu still have to sail south through the Bab el-Mandeb Strait to reach global markets. A Houthi closure (or even credible threat of sustained attacks) would turn Saudi’s bypass into a dead end. Oil could be forced to reroute all the way around the Cape of Good Hope — adding weeks of sailing time, skyrocketing freight costs, and effectively removing millions of barrels from prompt supply. Saudi officials have reportedly secured quiet commitments from the Houthis not to hit their ships, but today’s rhetoric puts that understanding under extreme pressure.

Where Do Oil Prices Go From Here?

Higher — and likely much more volatile. The twin-chokepoint risk (Hormuz already disrupted + Bab el-Mandeb now threatened) removes Saudi Arabia’s main contingency plan and tightens physical supply even further. Futures will jump on the headlines, but physical premiums could widen dramatically as refiners scramble for any available cargo. Expect more regional fragmentation: North American grades stay relatively suppressed, while Europe/Asia-payable barrels command ever-larger location and logistics premia.

Ripple Effects Hit Asia’s Diesel and Gasoline Markets

Asia, the world’s biggest importer of Middle East crude, is already feeling the secondary shock. Refined product prices — especially diesel (gasoil) and gasoline — have surged far beyond crude in percentage terms. Singapore gasoil cracks and jet fuel margins spiked as Red Sea shipping worries compounded the crude tightness. Even after some retreat on earlier ceasefire hopes, products remain elevated: gasoil still ~59% higher than late February levels in recent snapshots.

Countries across Asia are responding with the usual toolkit: price caps or subsidies (China’s “red oil” industrial diesel has more than doubled in Hong Kong’s tax-free bunkering market), export curbs on diesel, forced shorter work weeks in some nations, and outright demand destruction as high prices bite into transport and industrial activity.

Bottom line: the “oil price” you see quoted is just one slice of a much more complicated, stressed, and regionalized market. Physical reality is diverging sharply from paper benchmarks, and today’s Houthi threat just poured more gasoline on an already volatile fire. For producers, refiners, and consumers alike, location, logistics, and geopolitics are now dictating the true cost of every barrel.

- Jack Prandelli X post (April 20, 2026): https://x.com/jackprandelli/status/2046161418278354952

- Bloomberg Opinion chart (prices as of Apr 15 settlement, referenced in post context): Embedded image from the above post

- Houthis threaten Bab el-Mandeb closure: Times of India (1 day ago) https://timesofindia.indiatimes.com/world/middle-east/no-force-can-reopen-it-houthis-threaten-bab-al-mandeb-closure-after-iran-shuts-hormuz/articleshow/130367491.cms

- Additional Houthi/Bab el-Mandeb coverage: Daily K2, Mathrubhumi English, Habtoor Research (all April 19–20, 2026)

- Saudi East-West Pipeline at 7 mbpd: Fortune (April 12, 2026) https://fortune.com/2026/03/28/saudi-arabia-east-west-oil-pipeline-strait-hormuz-bypass-7-million-barrels-yanbu-red-sea/ and Reuters/Kpler data

- Paper vs. Physical gap analysis: Yahoo Finance / EBC (April 2026 reports)

- Asia refined products impact: Reuters (April 9, 2026) https://www.reuters.com/markets/commodities/refined-fuel-prices-retreat-asia-still-show-supply-stress-2026-04-09/ and StoneX Insights

- General oil price context: Fortune, EIA, Barchart, Energy Intelligence (mid-April 2026 updates)

Energy News Beat – Staying ahead of the real barrels.