The Strait of Hormuz has long been the world’s most critical energy chokepoint—handling roughly 20 million barrels per day (b/d) of oil and a significant share of global LNG before the 2026 crisis. But Iran’s de facto closure of the strait since late February 2026, amid escalating conflict, has forced a permanent rethink. Even if shipping resumes, the “Hormuz Squeeze” has accelerated diversification that markets will not reverse. Saudi Arabia, the UAE, and Iraq are fast-tracking bypass infrastructure. Non-Middle East producers in Latin America, the U.S., and beyond are ramping up exploration and LNG exports. And consuming nations are reevaluating energy security through a harder lens of resilience over reliance.

The Wall Street Journal captured this shift early: Gulf states are investing heavily in pipelines, rail, storage, trucking, and new ports to bypass the strait. What began as a crisis response is becoming structural change.

Iran’s Enduring Grip: No Nuclear Deal, No Surrender of Control

Under the scenario outlined—where Iran retains full control of the Strait of Hormuz and refuses any meaningful nuclear monitoring, material surrender, or de-escalation—the risk premium on Gulf exports becomes permanent. A recent X post by Mario Nawfal highlighted backchannel diplomacy: Iran relayed three conditions to Washington via Pakistan, including a veiled nuclear demonstration threat (“a detonation of a nuclear device on Iranian soil… as an irreversible sovereign demonstration of capability to control escalation dominance”). The immediate silence from Washington underscored the new reality: Iran’s nuclear ambitions and strategic leverage are non-negotiable.

This locks in long-term market fragmentation. Oil and LNG flows that once relied on the strait now carry a persistent geopolitical surcharge. Buyers will pay premiums for non-Gulf barrels, and producers outside the region will capture market share.

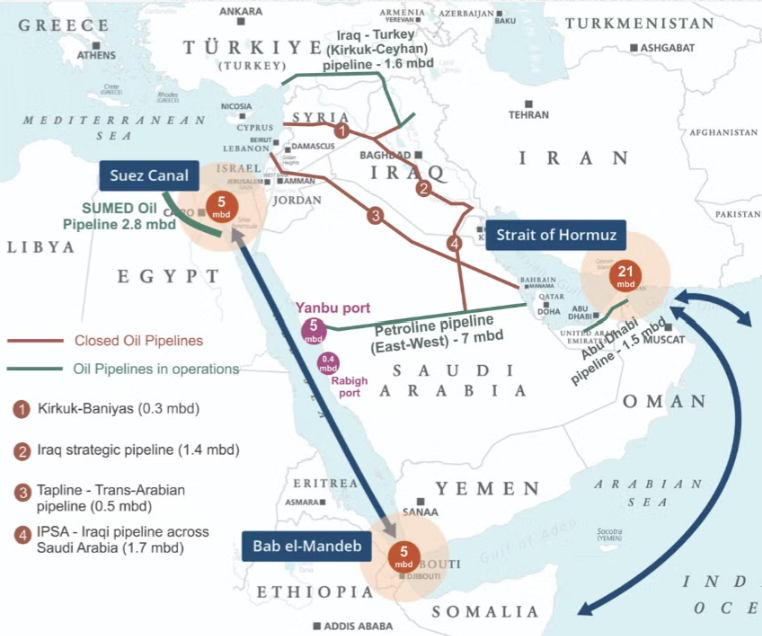

Pipelines: The New Bypass Highways

Gulf exporters have dusted off—and accelerated—decades-old contingency plans:

Saudi Arabia’s East-West Pipeline (Petroline) runs 1,200 km from Abqaiq to Yanbu on the Red Sea. Capacity up to 7 million b/d (with ~5 million b/d exportable). Flows have surged since the closure, rerouting crude away from Hormuz. From Yanbu, oil can reach Europe via the SUMED pipeline through Egypt.

UAE’s Abu Dhabi Crude Oil Pipeline (ADCOP): Links Habshan fields to Fujairah on the Gulf of Oman (~1.5–1.8 million b/d). Already handling over half of UAE exports pre-crisis; flows to Fujairah jumped post-closure. A second parallel pipeline is now ~50% complete and on track for 2027 completion, effectively doubling bypass capacity.

Iraq’s Routes: The Kirkuk–Ceyhan pipeline to Turkey’s Mediterranean coast has ramped to 250–650 kb/d and could hit 1.6 million b/d. A new Basra–Haditha line (planned 2.25–2.5 million b/d) is in early construction, targeting 2026–2027 flows.

These pipelines cannot fully replace the Strait’s ~20 million b/d capacity, but they provide 4.7–5.5 million b/d of immediate relief and growing redundancy.

Tanker traffic has shifted dramatically: vessels now queue around Africa or reroute via Red Sea ports.

Accelerated Exploration Away from Middle East Choke Points

The squeeze has supercharged upstream investment outside the Gulf:

Latin America leads non-OPEC growth. Brazil’s pre-salt fields (Buzios, Mero) and new FPSOs pushed output toward 4 million b/d in 2025, with more additions in 2026. Guyana’s Stabroek Block (ExxonMobil-led) hit over 900 kb/d by late 2025 and eyes 1.7 million b/d by 2030. Argentina’s Vaca Muerta shale is booming, with oil output forecast to reach 810 kb/d in 2026. Together, these three countries account for half of projected global crude growth in 2026.

U.S. shale and offshore continue steady expansion, feeding both domestic needs and LNG feedgas.

Africa (Namibia, Angola deepwater) and other basins see renewed interest as “safe” barrels command premiums.

These barrels bypass Hormuz entirely—no tankers needed through contested waters.

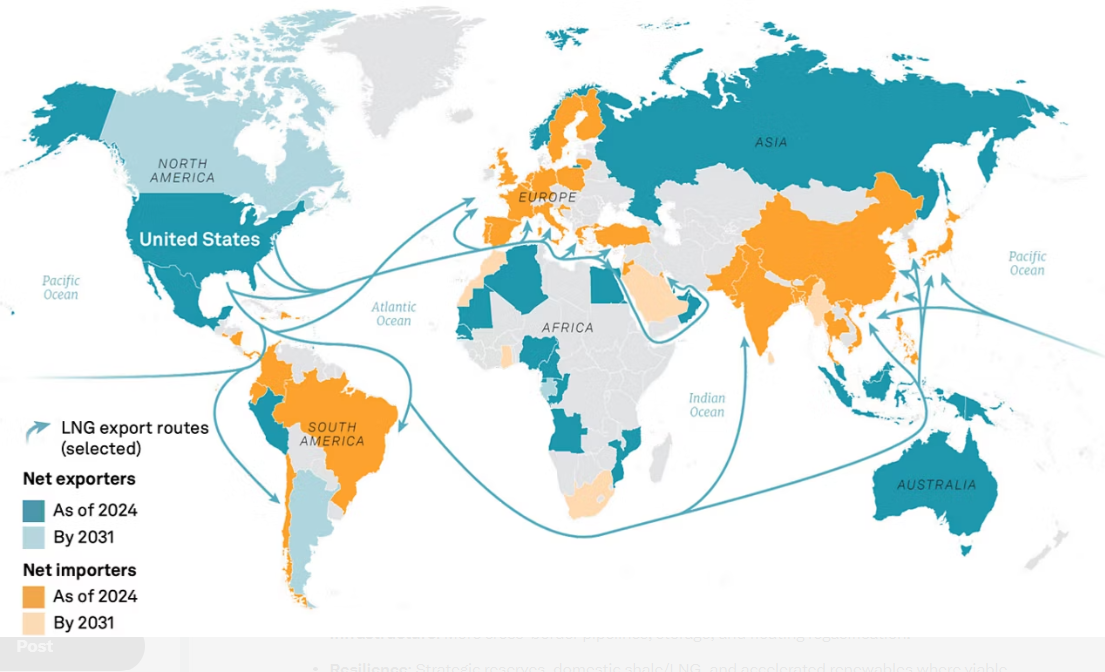

LNG Markets: From Qatar Shock to Atlantic Basin Dominance

Qatar—historically the Gulf’s LNG powerhouse—has been hit hardest. Iranian strikes damaged Ras Laffan, sidelining ~17% of its capacity (12.8 million tons per year) for 3–5 years. Production halted at parts of the complex, and a strait closure blocked shipping. Europe and Asia face multi-year supply gaps.

Enter the new LNG export hubs:

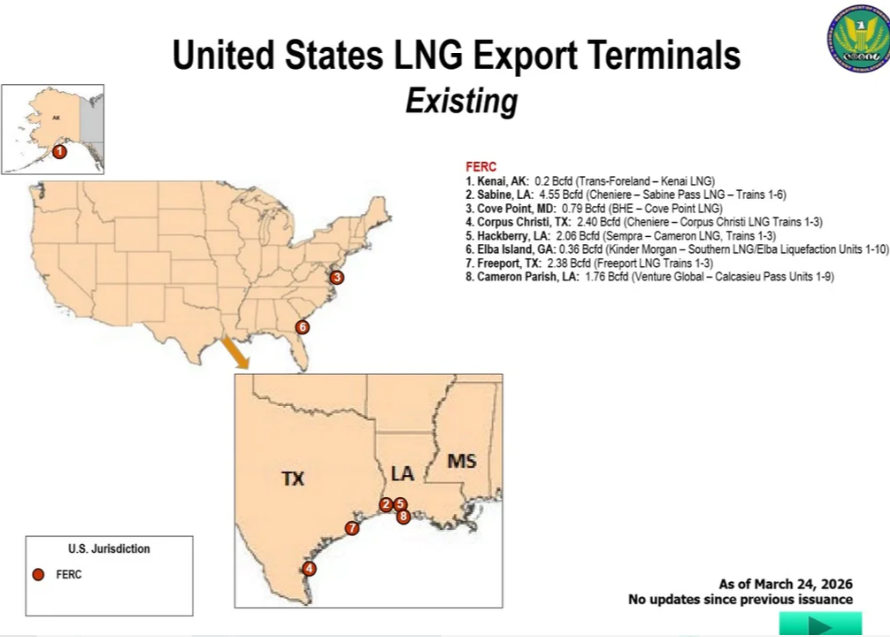

United States: The undisputed leader. Existing terminals (Sabine Pass, Corpus Christi, etc.) plus new ones like Plaquemines (Phases 1–2), Golden Pass, CP2, and Corpus Christi Stage 3 are flooding the market. U.S. capacity is exploding, with exports projected to grow sharply in 2025–2026. Atlantic routes avoid Hormuz entirely.

Canada: LNG Canada doubling output; Pacific Coast projects advancing.

Australia and others: Steady but now gaining share as Gulf LNG falters.

By 2030, non-Middle East LNG (led by the U.S.) will dominate flexible supply, shifting trade patterns permanently toward the Atlantic and away from vulnerable chokepoints.

Energy Security in a New Light

The Hormuz Squeeze forces a paradigm shift. Nations can no longer treat Gulf supply as reliable baseload. Strategies now emphasize:Diversification: Prioritize U.S./Latin American oil and LNG over Gulf volumes.

Infrastructure: More cross-border pipelines, storage, and floating regasification.

Resilience: Strategic reserves, domestic shale/LNG, and accelerated renewables where viable.

Geopolitical hedging: Long-term contracts with “safe” producers; renewed focus on overland pipelines (e.g., Central Asia to China/Europe).

Europe, Asia, and even China are already pivoting—ramping U.S. LNG, eyeing Latin American barrels, and exploring non-Gulf routes. The era of cheap, concentrated Gulf supply is ending. Markets are fragmenting into more resilient, multi-polar networks.

The Long-Term Outlook: A Redrawn Map

With Iran’s control of Hormuz and nuclear ambitions intact, the global oil and gas map is redrawn for good. Prices carry a permanent risk premium. Non-Gulf producers thrive. Pipelines become strategic arteries. LNG trade shifts westward. And energy security is no longer about volume alone—it’s about avoiding single points of failure.

The Hormuz Squeeze didn’t just disrupt flows. It accelerated the future.

- WSJ: “The Hormuz Squeeze Is Redrawing the Oil Map for Good” – https://www.wsj.com/world/middle-east/the-hormuz-squeeze-is-redrawing-the-oil-map-for-good-cf33d8c0?st=FrcuGU

- Mario Nawfal X post (nuclear context): https://x.com/MarioNawfal/status/2062787755177128415

- UAE pipeline updates: CNBC (May 2026), Reuters (May 2026), Guardian (May 2026)

- Saudi/UAE/Iraq bypass pipelines: Al Jazeera (Mar 2026), EIA World Oil Transit Chokepoints, NextBigFuture (May 2026)

- Latin America oil growth: EIA (Dec 2025), Oxford Energy

- Qatar LNG damage: Reuters (Mar 2026), Oxford Institute for Energy Studies

- U.S. LNG expansion: FERC, Global LNG Hub (Mar 2026), EIA

- Pipeline/LNG maps: The Conversation, Independent, Global LNG Hub, S&P Global (images via search)

Energy News Beat will continue tracking these shifts. The map has changed—permanently.