Russia’s domestic fuel shortage has escalated dramatically in July 2026, moving beyond diesel queues at gas stations to kerosene shortages, grounded or limited flights, and export bans on key refined products. Ukrainian drone strikes on refineries and the shadow fleet tankers are removing substantial refined product supply from both domestic and global markets.

This is no longer just a Russian problem. The loss of Russian refined product exports, combined with other global supply pressures, is tightening product markets worldwide — even as crude oil prices have eased. The result: higher refining margins (crack spreads), stickier pump prices, and rising second-order costs for transportation, agriculture, and manufacturing globally.

Escalation Inside Russia: From Gas Stations to Runways

According to commodities analyst Jack Prandelli, Russia’s fuel crisis has entered a “third dimension”:

- Gas stations have run dry in multiple regions.

- Tankers in the Sea of Azov stopped moving after strikes.

- Refueling is now limited or unavailable at airports in Makhachkala, Krasnodar, Astrakhan, St. Petersburg, Yekaterinburg, and Ufa.

- Wholesale kerosene prices have surged 52% to record highs.

- Moscow has banned kerosene exports until the end of November.

- The Moscow refinery (Kapotnya) is down for an estimated 6 months following drone strikes.

- Uzbekistan’s flag carrier has already canceled flights to affected Russian airports.

These developments follow months of Ukrainian long-range drone attacks on Russian oil infrastructure. Strikes have hit major refineries, including Omsk (~420,000–440,000 b/d capacity), facilities in Tatarstan (TANECO and TAIF-NK), Saratov, and others, along with oil depots.

Ukrainian Strikes on Shadow Fleet Tankers: Disrupting Refined Product Logistics

Ukraine’s Unmanned Systems Forces conducted intensive drone operations July 6–9, 2026, striking 32–36 vessels (mostly small-to-medium shadow fleet tankers ~7,000 DWT) in the Sea of Azov. These vessels were shuttling refined fuel products from Russian ports (e.g., Taganrog) to occupied Crimea via the Kerch Strait. A follow-up operation struck another 15 Russian tankers.

Damage was described as “industrial-scale,” with many vessels set ablaze or rendered inoperable. This directly disrupts short-haul refined product supply chains critical to Crimea and broader Russian logistics.

Update: 7-11-2026 Over 76 Russian Tankers or ships have been hit in the last 6 days.

How Many Russian Barrels Have Been Pulled from the Market?

Refinery capacity offline is the dominant factor. Cumulative Ukrainian strikes have disabled a significant portion of Russia’s refining system:

- Earlier estimates (early July 2026): ~42.74% of refining capacity disabled (Ukrainian General Staff).

- IEA: More than 20% offline.

- Peak disruption periods reached ~2 million barrels per day (mb/d) of refining capacity offline.

- Russia’s typical crude processing runs around 5.5–6 mb/d. Recent strikes (Omsk + others) have added hundreds of thousands of b/d more offline.

Conservative estimate: 1.1–2.4 mb/d of refined product production capacity removed from the market in recent months, with ongoing effects as repairs lag.

Tanker strikes add logistics disruption. The ~47 small tankers hit in the latest Sea of Azov operations (each carrying roughly 30,000–60,000 barrels of products) represent an estimated 1.5–3 million barrels of immediate disrupted product movements. Because these are repeated short-haul shuttles, the ongoing effect is equivalent to hundreds of thousands of barrels per day in lost throughput to key regions.

Combined with Russia’s full diesel export ban (announced to prioritize domestic supply) and kerosene export ban, Russia has effectively pulled well over 1–2 mb/d of refined products (diesel, jet fuel/kerosene, gasoline components) from global availability in recent weeks. Russia has even begun importing gasoline to cover domestic shortfalls.

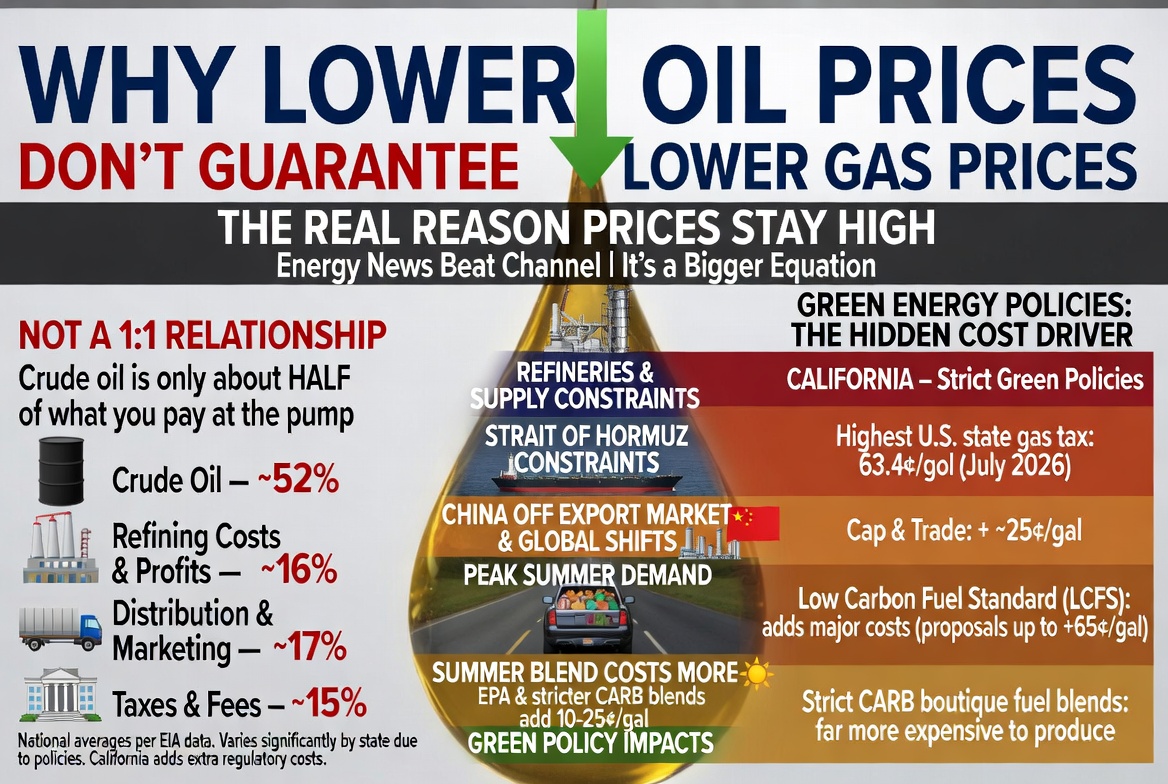

Why Crude Prices Fell While Pump Prices Barely Budged (or Rose)

Crude oil dropped from peaks near $120 to around $70 in recent periods, yet gasoline and diesel prices remained resilient. The reason is clear from market dynamics highlighted by analysts:

- Russian refineries under attack + export bans = less refined product supply hitting the market.

- Strait of Hormuz pressures are choking the fuel flows.

- China’s fuel exports dropped sharply.

- Peak summer driving season + more expensive EPA summer-blend gasoline (10–25 cents/gallon premium to produce).

Crude is only about half the cost at the pump. The refining/margin half is currently “broken” — meaning tight product supply supports higher crack spreads even if crude is softer.

US Refinery Storage Levels and California’s Vulnerability

Latest EIA data (week ending July 3, 2026):

- Commercial crude oil inventories: 411.4 million barrels (up 3.0 million barrels week-over-week).

- Gasoline stocks: 212.1 million barrels (down 1.9 million barrels).

- Distillate fuel oil (diesel/heating oil): 103.6 million barrels (down ~5 million barrels).

- Refinery inputs: 17.0 mb/d (down 173,000 b/d); utilization ~95.8%.

US product inventories are drawing down amid strong demand, while crude has seen a modest build.

California (PADD 5) is particularly exposed.

The state has chronically low crude storage (around 9.1–9.2 million barrels in mid-2026 data, or ~29% of ~32 million barrel tank capacity). California consumes ~1.3 mb/d of crude but produces far less domestically and relies heavily on marine imports for both crude (~75% of supply from outside the state) and, increasingly, refined products.

Recent and upcoming refinery closures (Phillips 66 Los Angeles, Valero Benicia) are removing significant in-state refining capacity, forcing higher reliance on global imports for gasoline and blendstocks. California has reported only 4–6 weeks of buffer supply in some assessments (a rolling forecast), making it sensitive to any global tightening in refined product availability.

Impacts on Consumers and Investors

Consumers:

Higher gasoline and diesel prices at the pump, especially in import-dependent regions like California and the West Coast.

Potential for localized shortages or rationing if disruptions worsen (already seen in Russia).

Second-order effects: Higher transportation and logistics costs feed into food prices, goods inflation, and broader economic pressure.

Investors:

- Refiners stand to benefit from elevated crack spreads (strong product margins relative to crude).

- Upstream producers face mixed signals — softer crude but potential support if product tightness spills over.

- Energy sector volatility increases; Russian energy assets face further downside from capacity losses and sanctions pressure.

- Broader markets could see inflation reacceleration risks if energy costs rise persistently.

- Opportunities in trading refining margins or hedging product exposure.

The Bigger Picture: Global Second-Order Effects

Reduced Russian refined product exports remove a meaningful supply source from an already tight global product market. When combined with Middle East tensions (Hormuz), Chinese export declines, and seasonal demand, the risk of sustained higher fuel costs worldwide rises. This can amplify inflation, slow economic growth, and pressure central banks.

Russia’s crisis is a stark reminder that refining capacity and logistics are far less flexible than crude production. Attacks on downstream infrastructure create longer-lasting market distortions than crude supply shocks alone.

Appendix: Sources and Links

- Jack Prandelli X post (fuel crisis escalation, kerosene ban, refineries, airfields): https://x.com/jackprandelli/status/2075941113500749898

- Jack Prandelli X post (why crude fell but gas prices held, Russian refineries, export bans): https://x.com/jackprandelli/status/2075961114118979661

- Energy News Beat article on Ukrainian strikes on 15+ Russian tankers (Sea of Azov operations details): https://energynewsbeat.co/crude-oil/ukraines-defense-forces-struck-another-15-russian-tankers/

- EIA Weekly Petroleum Status Report (July 3, 2026 data): https://www.eia.gov/petroleum/supply/weekly/

- Wikipedia: 2025–2026 Russian fuel crisis (capacity loss estimates, domestic impact)

- Reuters, IEA, Bloomberg reporting on refinery strikes, export bans, and output revisions (various July 2026 articles referenced in searches)

This situation is fluid. Continued strikes, repair progress, or policy responses (further bans or imports) will determine how deep the global ripple effects go. Energy markets are watching closely.