ENB pub Note: This article ran on David Blackmon’s Substack and validates several articles we have published here on Energy News Beat. We recommend subscribing to David’s Substack. David and Stu Turley will be on a Podcast this week with Tim Stewart, President of the US Oil & Gas Association.

Six weeks after I wrote a Forbes column declaring that the oil price narrative had flipped from “lower for longer” to “higher for longer,” Goldman Sachs has dropped a detailed April 23 research note supporting that thesis. The report, titled “How Fast Can Gulf Production Recover After Reopening?,” analyzes the staggering 14.5 million barrels per day, 57 percent cut in Persian Gulf crude output caused by the Hormuz shutdown and associated conflict precautions.

Goldman’s analysis, led by Daan Struyven, makes relatively optimistic in its base case, which assumes a safe, full reopening of the Strait with no renewed strikes on oil assets and limited physical damage to producing fields (unlike the LNG facilities that took real hits). Under those conditions, they say Gulf production should “mostly recover within a few months.”

But a deeper dive into the numbers and the caveats reveals a far less rosy picture. External forecasts averaged by Goldman – pulling from EIA, IEA, and Rystad Energy – show only about 70% of that lost output returning after three months of reopening and 88% after six months. In other words, even in the best-case scenario, the world will still be short roughly 1.7–4.3 mbd of Gulf crude well into the second half of 2026 and beyond. That’s a recipe for structural tightness beyond this year.

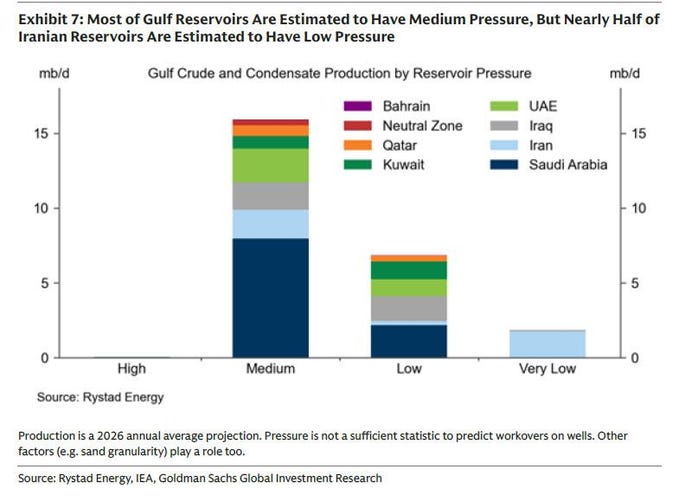

The headwinds Goldman lays out are exactly the kind of logistical and geological friction I warned about in March. Empty tanker capacity in the Gulf has plunged roughly 50%, or 130 million barrels, since the conflict escalated. Destocking previously produced crude is now bottlenecked. Fields – particularly lower-pressure reservoirs in Iran and Iraq, which make up nearly half the Iranian portfolio – require extensive workovers to restore flow rates. Some of those wells in low pressure formations will never recover prior production levels.

Procurement delays for drill pipe, materials, and skilled crews add more weeks and months. Saudi Arabia and the UAE could potentially throw more than 2 mbd of spare capacity into the market quickly, thought great skepticism exists about their real reserve capacity levels. But even that generous buffer, if real, cannot instantly erase the cumulative disruptions.

The longer the shutdown drags on, the greater the risk of permanent “scarring” to reservoir productivity. Every day of additional delay increases the odds, and this isn’t hypothetical. Goldman references five previous major supply shocks where full recovery either took quarters longer than expected or never fully materialized. The reality is that we are in uncharted territory here: an unprecedented Hormuz closure layered on top of deliberate precautionary curtailments across multiple producing nations.

This is precisely why the pre-conflict consensus of Brent heading toward $60 and WTI even lower was always built on sand. That narrative assumed an oversupplied market – based on always suspect IEA analysis – responsive non-OPEC supply (especially U.S. shale), and no major geopolitical surprises. The black swan arrived on February 28 with the U.S.-Israel operations against Iran, and the market has been playing catch-up ever since.

Enverus Energy Research was among the first to call the new regime “The Return of $100 Oil,” projecting Brent averages near $95 for 2026 and $100 for 2027. Goldman’s own earlier revisions have tracked higher, and this latest note gives analysts zero reason to walk those forecasts back.

The economic implications are already rippling outward. U.S. gasoline and diesel prices have climbed more than a dollar per gallon nationally in a matter of weeks, according to AAA data. Global inventories are being drained at a pace that cannot be sustained without further price support. American shale producers, still disciplined after years of capital restraint and consolidation, are not going to flood the market with new rigs because Brent hovers above $90. They remember 2014 and 2020 all too well. Investors demand free cash flow and shareholder returns, not another boom-bust cycle.

Policymakers in Washington and Europe keep talking about “energy security,” yet the reality on the water is that roughly 20–23 mbd of normal Hormuz throughput has been rerouted or simply idled. Even if the Strait reopens tomorrow, tanker scheduling, pipeline redirections, and field maintenance cannot be solved with press releases. The supply-driven shock we are living through is not transitory. It is durable.

Goldman’s report is sober, data-heavy, and refreshingly free of wishful thinking. It confirms what the market has been pricing in since early March: the era of cheap, abundant oil was a temporary illusion propped up by fragile geopolitics and over-optimistic supply forecasts. The return of $100 oil is not a spike. It is the new baseline until proven otherwise.

The world has an oil flow problem that will not be solved in weeks or even a few months. Higher for longer is no longer a forecast: It is most likely the operating environment for the rest of this decade.

Check out the Energy News Beat Substack: https://theenergynewsbeat.substack.com/