Iran’s renewed military actions in and around the Strait of Hormuz are once again disrupting global shipping and threatening the fragile recovery of oil flows through one of the world’s most critical energy chokepoints. As of late June 2026, strikes by both Iranian and U.S. forces have set back recent gains in tanker traffic, keeping markets on edge amid an ongoing crisis that began earlier in the year.

The Strait of Hormuz normally handles roughly 20 million barrels per day (mb/d) of crude oil and petroleum products—about 20% of global supply. Disruptions here create immediate ripple effects worldwide, forcing the United States into the role of “supplier of last resort” through surging exports. This has rapidly drained domestic commercial inventories, particularly at the key Cushing, Oklahoma hub, while the Strategic Petroleum Reserve (SPR) continues heavy drawdowns to cushion prices and supply gaps.

Real Numbers: Hormuz Disruptions and Market Strain

Recent reporting highlights renewed strikes over the past several days following a period when traffic through the Strait had climbed to its highest levels since the start of the U.S.-Iran conflict. Ship operators remain wary, with analysts noting that shipping is “literally caught in the crossfire.” Specific incidents include attacks on vessels such as a Singapore-flagged container ship and an oil tanker, prompting U.S. responses targeting Iranian sites.

Analyst insights from X (formerly Twitter) underscore the stakes:

One post emphasizes that crude quality matters as much as total volume—national stockpiles don’t solve regional crises because “crude cannot teleport.”@CaptainRoyenTanker market commentary stresses that any U.S.-Iran deal must be “material” for the Strait to fully reopen. @NewsFinOil

Energy expert Anas Alhajji has highlighted legal and market dimensions, including questions around transit fees and how Russia has profited from the crisis through higher realized prices.

These factors have driven volatility in oil prices, with spikes on news of fresh incidents.

Cushing, Oklahoma: Already Below Operational Minimums

Cushing serves as the delivery point for WTI crude futures and a critical hub for U.S. pipelines and exports. Its operational minimum is widely viewed by traders as approximately 20 million barrels. Below this level, pumping becomes difficult due to suction line issues, crude can turn sludgy with sediment and water, quality degrades, and the hub struggles to meet all customer demands efficiently.

Latest EIA data:

Week ending June 12, 2026: 20.03 million barrels

Week ending June 19, 2026: 18.96 million barrels (draw of ~1.08 million barrels that week)

The U.S. is already operating below operational minimums at Cushing. Short-term operations are possible but come with rising stress: higher costs, potential quality mismatches for exports or refiners, and elevated risk of localized disruptions or force majeure declarations on certain movements. Rebuilding stocks to comfortable levels (historically 30+ million barrels) would take weeks to months, even if global flows normalize, depending on the pace of U.S. production versus export demand.

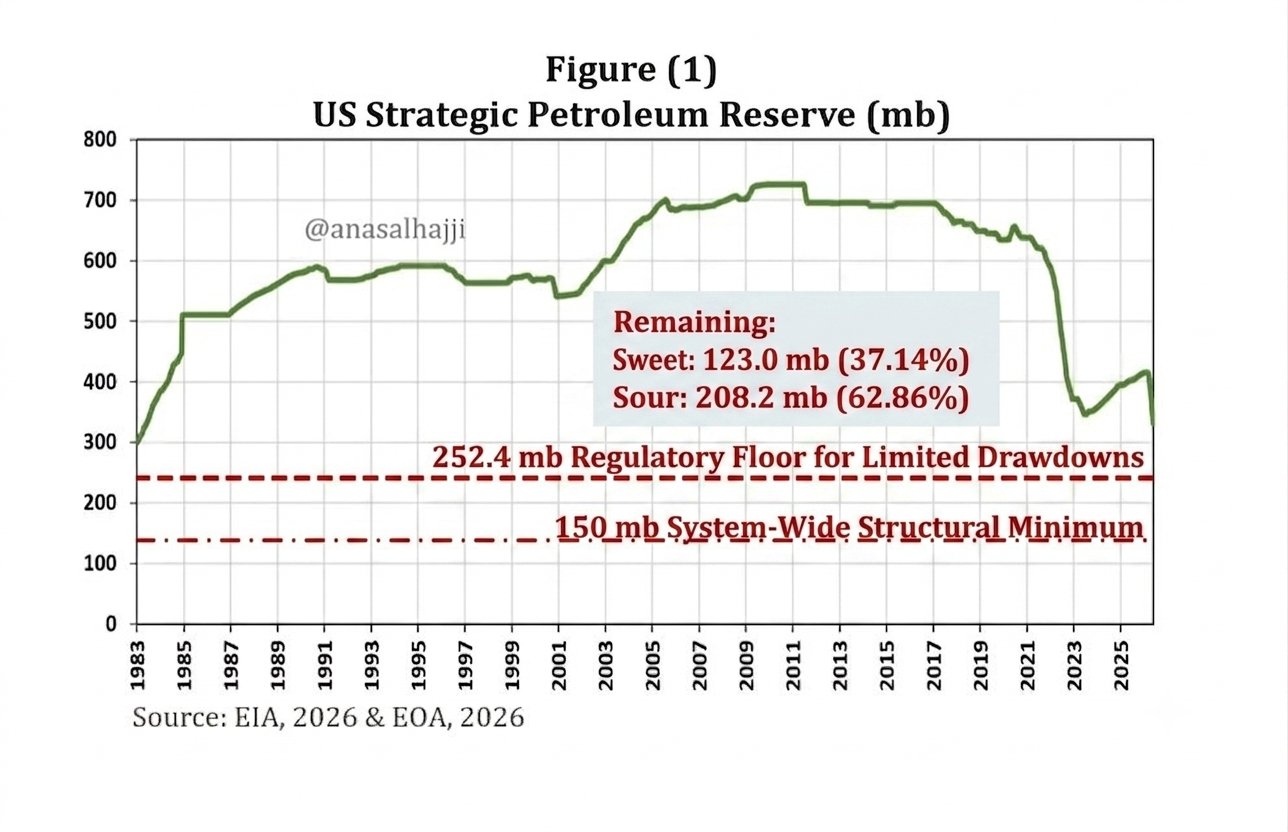

SPR Levels and Drawdown Timelines

The U.S. Strategic Petroleum Reserve stands at its lowest level since 1983. As of the week ending June 19, 2026, total inventories were approximately 331.2 million barrels.

Key composition insight (as of late June): roughly 123 million barrels sweet crude versus 208 million barrels sour crude. This imbalance represents a strategic constraint, as many Gulf Coast and West Coast refineries are optimized for sour crudes, while others prefer light sweet grades.

Drawdown context: Recent weekly draws have been in the 8–10+ million barrel range amid efforts to stabilize markets during the Hormuz-related supply shock. At a recent average pace of roughly 1.29 mb/d, projections show:

Approach to the SecDef-certified floor of 243 million barrels (tied to the 172 million barrel release authorization): around August 26, 2026.

Discussion of a legally/operationally referenced minimum around 150 million barrels: potentially November 2026 if the current draw rate holds.

Physical/operational limitations of the SPR (reduced draw rates due to cavern dynamics, sediment, and brine management) would likely begin to manifest progressively as levels fall further, well before absolute physical floors (~44 million barrels, estimated in some analyses). These constraints are not a hard “off switch” but degrade capability over time.

Will key thresholds be hit in August?

Yes, for the important 243 million barrel certified floor under current trends. Broader operational stresses at the SPR are already relevant and will intensify through the summer.

Recommendations for Consumers and Investors

For consumers:Monitor local gasoline and diesel prices closely—volatility is likely to persist with any Hormuz news.

Consider strategically topping off vehicle tanks during relative dips rather than waiting for potential spikes.

Reduce discretionary driving, combine trips, and explore public transit, carpooling, or fuel-efficient options where practical.

Businesses reliant on diesel (trucking, agriculture, construction) should review inventory buffers and hedging strategies.

For investors:

- The energy sector (upstream producers, midstream operators, and certain refiners) can benefit from sustained higher prices, but rapid resolution of the Hormuz situation or demand destruction could reverse gains quickly.

- Watch Cushing differentials, export volumes, and SPR draw rates as leading indicators.

- Consider diversified exposure within energy (e.g., via broad ETFs) and tools to manage volatility.

- Geopolitical risk premiums can evaporate fast on positive diplomatic developments.

- Long-term fundamentals (U.S. production resilience, global demand trends) remain important beyond the immediate crisis. This is not investment advice—consult professionals and do your own due diligence.

The situation remains fluid. Any material de-escalation or reopening of reliable Hormuz traffic could ease pressure on both Cushing and the SPR relatively quickly, while prolonged tensions would accelerate the timelines outlined above.

With the heavy US military activity in the area not covered on the news, it should be an indicator that something is happening. Also, look at the Iranian IRGC claiming the UAE exit port in the Gulf of Oman is a critical overreach.

- NYT article (June 27, 2026): https://www.nytimes.com/2026/06/27/business/strait-of-hormuz-shipping-iran.html

-

@CaptainRoyen

X post (June 27, 2026): https://x.com/CaptainRoyen/status/2070978215980482831

-

@NewsFinOil

X post (June 27, 2026): https://x.com/NewsFinOil/status/2070988094753353765

-

@anasalhajji

recent relevant posts (June 27–28, 2026 examples): Searchable on X; insights on Hormuz legal/market issues.

- EIA Cushing data: Via https://www.eia.gov (weekly stocks reports referenced in multiple outlets).

- SPR levels: YCharts/EIA data and DOE sources.

- Additional context: Reuters, CNN, Semafor, and analyst discussions on operational floors (243 mb certified, ~150 mb referenced minimums).

- Hormuz throughput baseline: EIA historical averages (~20 mb/d).

All data is current as of late June 2026 reporting. Markets move fast—verify latest EIA releases for updates.