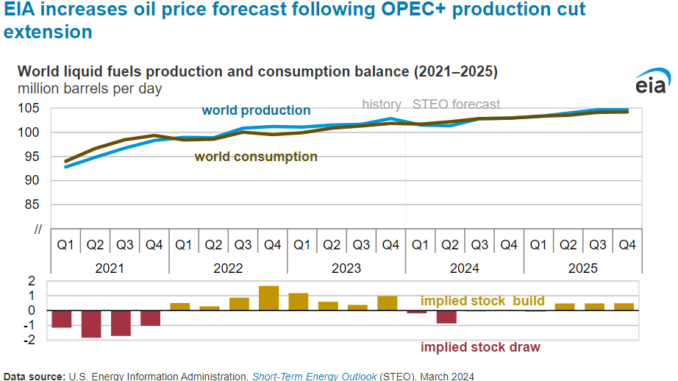

We increased our forecast prices for crude oil and petroleum products for the remainder of 2024 in our March Short-Term Energy Outlook (STEO) following the announcement that OPEC+ will extend the existing voluntary production cuts through the second quarter of 2024. We now forecast significantly less global oil production than world oil consumption through the first half of 2024, requiring draws on world petroleum stocks (inventory). Stock draws tend to increase oil prices.

We reduced our forecast for world oil production in the second quarter of 2024 (2Q24) to 101.3 million barrels per day (b/d) in the March STEO in response to OPEC+ extending its cuts. That results in global oil production that is 0.9 million b/d less than our forecast of 102.2 million b/d for world oil consumption. Although we expected some OPEC+ countries to continue to restrict production, we expect the March 3 announcement to result in larger cuts to production than we had previously assumed. The announcement includes an additional voluntary production cut from Russia.

The current OPEC+ agreement includes two types of production cuts. The first type is officially stated production targets, and the second type is additional voluntary cuts pledged by certain OPEC+ countries. Although our previous forecast assumed that some OPEC+ members would maintain voluntary cuts—which had been set to expire after 1Q24—through 2Q24, this new announcement pledges that cuts will be continued for all member countries through the first half of 2024. Because OPEC+ did not relax production targets and because Russia added new voluntary production cuts, market participants will have to withdraw oil from stocks to meet demand, which puts upward pressure on oil prices.

The draw on global oil stocks during 2024 will keep Brent crude oil prices elevated, averaging $88/b in 2Q24, $4/b higher than we had forecast in the February STEO. Prices will remain relatively flat for the rest of the year before falling to $82/b by the end of 2025 as OPEC+ supply cuts expire and production increases.

Several factors present uncertainties to our forecast:

- Geopolitical tensions. No crude oil or product tankers have been lost because of the ongoing attacks on commercial shipping in the Red Sea, but many ships are rerouting to avoid the area. Rerouting lengthens the trip and increases costs. Attacks continue to pose a threat to ships that transit the Red Sea, which could increase prices further.

- OPEC+ compliance. If some countries do not comply with the latest round of voluntary OPEC+ production cuts, it would increase the amount of oil in the market, which would reduce prices.

- World oil consumption and economic growth. Stronger demand growth than our forecast would reduce global stocks and raise oil prices, just as less demand growth would increase global stocks and reduce prices.

Crude oil prices make up more than 50% of U.S. retail gasoline prices. Refining costs fluctuate seasonally but usually determine between 10%–25% of the retail gasoline price. Distribution costs and taxes make up the rest. Following large planned and unplanned refinery outages in the United States in recent weeks, we increased our refining margin forecast, which is the difference between the wholesale gasoline price and the Brent crude oil price. Both higher crude oil prices and refining margins led us to increase our regular-grade retail gasoline price forecast by 20 cents per gallon for June, July, and August from what we forecast in the February STEO.