We sat down with Andrew Dittmar, Senior M&A Analyst at Enverus and we had a blast talking about the report they just put out. This was my second interview with Andrew and he again demonstrated that the team from Enverus knows data.

We sat down with Andrew Dittmar, Senior M&A Analyst at Enverus and we had a blast talking about the report they just put out. This was my second interview with Andrew and he again demonstrated that the team from Enverus knows data.

The discussion was around the M&A activity in the U.S and Canadian markets. It was surprising on some of the numbers that were thrown around. With the consolidations and the higher oil prices, it is going to be fun to see what is coming around the corner.

Thank again Andrew for stopping by the podcast, and look forward to your next report! The automatic transcription is below the interview, and we disclaim any errors unless they make me sound smarter or funnier.

To get in touch with Andrew his LinkedIn address is: https://bit.ly/3loDTET

For everything data around Energy – look at Enverus.com

The Energy News Beat Podcast is sponsored by King Operating Corporation.

The Energy News Beat Podcast is sponsored by King Operating Corporation.

Contact Us for a Free E-book from Jay R. Young on the Upside of Oil and Gas Investing.

HOW THE NEW MODEL WORKS AND WHY IT PUTS THE TRADITIONAL MODEL TO SHAME

Featured on Forbes.com

Full Automated Transcript:

Stu Turley, Sandstone [00:00:04] Hey, good morning, everybody. Today is a fabulous day. It’s one of my favorite companies out there. Welcome to the Energy News podcast. My name is Stu Turley and I’m the president and CEO of the Sandstone Group. And we have got Andrew Ditmar. He is the senior M&A and analyst for investors and just did a gigantic review of U.S. upstream and M&A review. Phenomenal report. Welcome, Andrew, and thank you for stopping by.

Andrew Dittmar, Enverus [00:00:38] Hey, thanks for having me on. Great to be back.

Stu Turley, Sandstone [00:00:40] Oh, hey. The last time you and I talked was about a year ago, I think before covid. And I am so glad we’re opening back up. I mean, it’s been a while.

Andrew Dittmar, Enverus [00:00:51] It has it it’s been a bit of a trip.

Stu Turley, Sandstone [00:00:57] And you were saying right before the show, this is one of your first times wearing a tie.

Andrew Dittmar, Enverus [00:01:01] Again, it is. That said that.

Stu Turley, Sandstone [00:01:05] And I. I love it. I’m excited about Nate. Are you going to be going to Nate?

Andrew Dittmar, Enverus [00:01:10] You know, I’m not sure if I’m on the books for Nape or not. I’m going to be in Houston next week for Urtext, so. Oh, that that was a trial. This is a trial run with the tie to make sure I could still tie one. Got it into pressing issues there and sit still more or less fits. I’m glad I’m not going to be doing any emergency suit shopping between now and next Monday, so I’ll be in town for Artec. I’m not sure if I’ll make it back for a hope. So it’s always a great time.

Stu Turley, Sandstone [00:01:35] Oh, you know, hey, if you’re there, I definitely want to buy a cup of coffee and say hi. I’ll tell you it. Let’s tell our listeners what you do when you’re in an M&A analyst for investors and how this report comes about.

Andrew Dittmar, Enverus [00:01:53] You’re so I’m in the in various what we call market research group and are on the job. And my team is tracking energy in the day. So we cover upstream International Canada and of course, the U.S. as well as midstream downstream. And we started adding more in the power and renewable space. It’s really part of our business, but probably still 80 percent of my time is spent on the on the U.S. upstream side. That’s where we have the most fun. And that’s what we know best, our core competencies are. And so we check those deals. We analyze them. We figure out what people are paying for production and acreage in these different plays, why a deal makes sense or doesn’t make sense, and then we amalgamate all those deals and look at what’s going on in the industry, what kind of trends are out there, who’s buying, who’s selling and what that means going forward. And then once per quarter, we put out this report that you have there, which is our inventory review just looks back over the last quarter, all your basic data. You’d want to see what happened in upstream in the day. And then we try to throw in a few slides, kind of highlighting we thought the most important pieces of the market were from the last quarter or so. In this latest report, private equity exits were a big piece of the market. So we threw a few extra slides in kind of talking about that and what’s going on in the space.

Stu Turley, Sandstone [00:03:14] Yep. Now you’re stealing some of my thunder. And my question is because P and how people are getting financed in oil and gas, we can go ahead and jump there if you want. I’ll be doing

Andrew Dittmar, Enverus [00:03:25] whatever works for you.

Stu Turley, Sandstone [00:03:26] Oh, hey, let’s go ahead and jump to P e because if you take a look at the share of transaction values, I believe that slide 11, I actually looked at your slide deck. So it’s kind of fun to be able to say, hey, wait a minute, what about this slide, the share of transaction by peer group in private equity-backed private, public and undisclosed. Can you tell us a little bit about the trend and what you were thinking there?

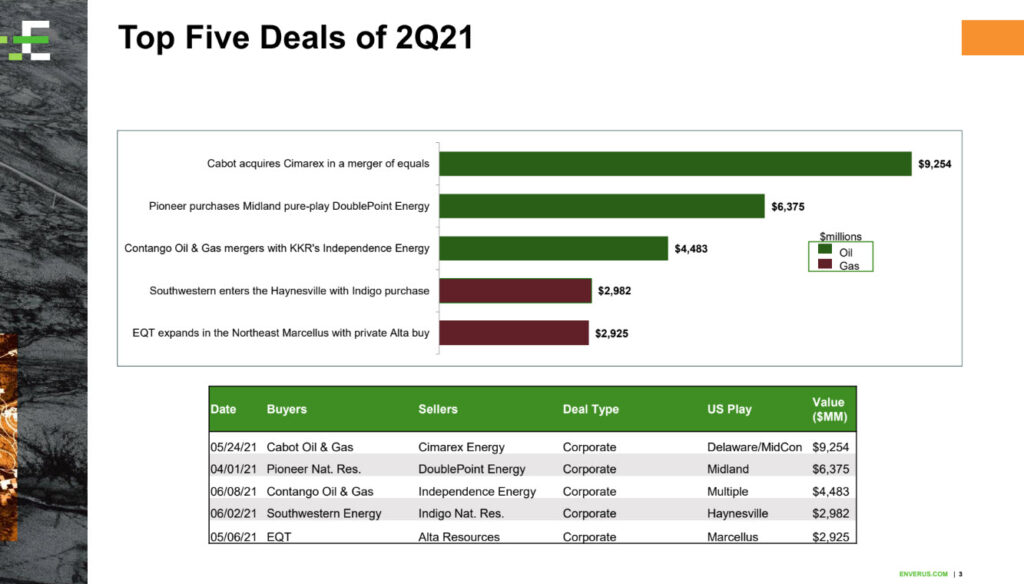

Andrew Dittmar, Enverus [00:03:52] Sure. So just to clarify our terminology, they’re public obviously is pretty self-explanatory, as is undisclosed private equity or companies that are primarily associated with institutional sponsors backed by KKR Warburg, whatever, and then private to the ones that aren’t are not public, but also not affiliated with a particular PE firm. So private and private equity, we break them up. They tend to pretty much follow the same trend, open up those together here. But what we saw, I think combined, they were about 60 percent of the value last quarter. So that was the highest that we had since twenty sixteen. And if you think back to 2016, that’s when everybody wanted to buy into the Delaware Basin and the private equity guys held most of the acreage that they wanted. And so we saw a rash of exits there is that faded out. There were some key exits here and there, but it really wasn’t a big piece of the market for probably about three or four years there. And then just this latest quarter, we really saw the exits take off. So they took off both in absolute dollar terms. And I think we had our best quarter even topping some of the twenty sixteen. M&A activity and then also in percentage terms topped more than half the market, up to 60 percent and would have really dominated even more. So in terms of percentage, we just have one big public company merger, which we may touch on a bit later. Cabot and Cimarex not strictly a harbinger of other deals, but that added about 10 billion in value. If you look at what Cimarex is getting in equity, plus the value of their assumed debt. So that had a good chunk of value, kind of a one-off deal of the public side. But, you know, in terms of overall deal flow, I think we seven deals that were over a billion dollars, which in and of itself is a pretty impressive number. And out of those seven, five or sales might be backed companies or private. So pretty, pretty dominant part. And really was the driver in that to do this last quarter?

Stu Turley, Sandstone [00:05:49] What were some of the highlights? You mentioned Cimarex and Cabot, both are top-notch companies. What were some of the highlights that Andray, you were taking a look at when analyzing that deal?

Andrew Dittmar, Enverus [00:06:02] Sure, so

Stu Turley, Sandstone [00:06:04] sorry. I think just ballpark if you would,

Andrew Dittmar, Enverus [00:06:07] now it’s a great question. Yeah, like you said, two top-notch performers, but I think that deal kind of came out of left field on I think it’s in my business and a lot of us I’m sure you do the same thing. You know, we roll over in the morning and first thing you do is grab your phone and look at see what the headlines are for the for the morning deals. And so Cimarex merging with Cavitt and drink a cup of coffee and came back to open up. And that was still there. So I had to convince myself that was really happening and probably not the only end was going through that process. So all the other public company mergers we’d seen were really in based on consolidation place. So it was deals like pioneered by Possley, Conoco, which basically had a pretty substantial permanent exposure, buying Concho, Borking, those positions up. And you highlighted both the Jeanna synergies that you get, the general administrative cost savings, as well as operational efficiencies. And we’ve talked about these points and I think for years. But the benefits of having more contiguous acreage, being able to develop with longer laterals, better access to takeaway capacity, better sourcing of drilling rigs, whatever helps if you’re a big, big dog in the base. And yes, that’s really been the trend in almost all the public public deals we’ve seen. And then you get Cimarex merging with Cavitt where they have no operational synergies that overlap in any basins. They’re focused pretty much on two different commodities and Cimarex being more or less an oil producer in the Permian with some gas exposure there and in the Mid-Continent Cavitt being a pure gas play. So, you know, I think management did did a pretty good job there, laying out the rationale, probably a little bit of an uphill battle to sell it on investors. But you are growing. You know that oil and gas prices are not entirely correlated sometimes when a commodity outperforms the other. So you’ve got broad exposure across. You can sort of allocating capital as you want to take advantage of relative outperformance by either oil or gas. And, you know, you’re reaching up to a larger scale that maybe makes you a little bit more investable for people to screening for those largest companies out there. I think there’s really the capital is flowing in, is pretty much going to the large side of the market has been so, you know, reasonably decent case there. I think we’d probably like the deal slightly more from Cabot’s point of view than Cimarex is. Cavitt has been a darling for a number of years here. It did a great job, but they haven’t really moved on anything over the years. Maybe even some of the other gas names were a little bit cheaper. They didn’t make a move to go ahead and roll those up, take advantage of their higher-priced equity. And now their stock came down a bit and some of those other gas names get a little bit more expensive. It’s tough to make an accretive deal. They have drilled up. They have a good inventory run away, but they’ve also drilled a lot over the years. And so the longer term, maybe they need to do something to to extend that run away. And obviously, merging with Cimarex, you have a huge runway in the Delaware Basin. So that takes any inventory issues off the table. So, you know, from someone else’s point of view, I mean, you get a good partner in the cabinet, lots of your bullish on gas. But I think it wasn’t if you’d asked me to pick the top 20 merger partner Cimarex might grab I can’t be honest with you and tell you the cabinet might have been on my list.

Stu Turley, Sandstone [00:09:36] You’re not the first person, Andrew, that I had heard say that that they were kind of like came out of left field on that in the different place. You mentioned the different gas versus oil and one of the basins was really the most active and single play. Was Pioneer’s purchase of double point in the middle? Is that that was on one of your main talking points there. Do you want to go over the idea of pioneers? I mean, that seemed like a pretty it was in the news a bunch.

Andrew Dittmar, Enverus [00:10:10] It was a big deal. Sixty-six point four billion. I want to say that that was the largest pizza we’ve tracked. And gosh, if not 10 years, darn close to 10 years. It was it’s been a long time since we saw a private sale that that kind of scale. Yeah. So pioneer, obviously, one of the more aggressive acquirers out there, they did the parts they deal late last year. I’m not very well, I think in terms of where commodity prices, where Scott Sheffield has been pretty vocal in terms of being a proponent of consolidation in the industry. And there’s really not space for more than a handful of relevant Impey companies in each play, one for play. And obviously, he sees Pioneer is playing that role in their home base. And so not surprising at all that they would go out and make an additional acquisition. If you look at what the opportunity set is out there in the in the middle of basin where their home base and there’s not that many privates of the scale of double point, you’ve got double point themselves. You know, you’ve got conquest, probably get you there and you’ve got endeavor, but there’s not many, many pieces of private that size. So obviously they like to scale and they like the fit and they we’re willing to go out and move what looked to be a pretty aggressive price to get them six point four billion. I think in our valuation we put maybe two billion of that on production, which left four billion over for upside and came out at about forty thousand per acre. So, again, kind of a throwback to the old days of Permian M&A where these thirty-forty thousand dollars an acre no, it didn’t really phase you, but we hadn’t seen one of those on a meaningful deal in a long time. So definitely screened quite a bit higher than the other deals we’ve watched in the past. And they were able to mostly fund it with pioneer stock, which is great. That’s been a big trend to revisit later. But these sales are being done for equity. We were able to fork it over as opposed to cash years back. And so that makes the deal a little bit easier. You don’t have to go out and lever up by issuing notes or drawing down the revolver. You don’t have to go through the headache of trying to do a secondary equity raise, which maybe investors wouldn’t be so receptive to. So, yeah, they really do. Most of that done with stock added a very, very strong position there in the Midland and extended already. Pretty impressive runway even further. Just the headline number. Forty thousand acres, awfully big.

Stu Turley, Sandstone [00:12:36] So I’m going to ask you to pull out your crystal ball because we got so surprised with the cabinet. Do you think Croonquist would be the next one up on the auction block, by any chance?

Andrew Dittmar, Enverus [00:12:50] It’s too hard to comment on an individual company. They got to do a fly on the wall of their management meetings and know what the team is thinking there, but certainly, they’re a rare company out there in terms of the scale that they have and the strength of their position.

Stu Turley, Sandstone [00:13:07] So it would be an attractive target.

Andrew Dittmar, Enverus [00:13:11] It was for sure. I don’t know what she’s going to depart with in Denver any time soon. So if you had to list your biggest targets left out there is on the private side and in the Permian, they’d certainly be at the top of the list.

Stu Turley, Sandstone [00:13:27] And so the other big deal that you have in your ear is contango and KKR independence, that was only, what, four-point four? What were your highlights on that rascal?

Andrew Dittmar, Enverus [00:13:40] Sure. So that’s kind of a tricky one, to put a dollar value on the nature of our business and we run an M&A database. So you need to have a buyer or seller in a deal value. So here you have Contango, which is a pretty small, publicly-traded company with pretty concentrated ownership. I think the primary individual shareholder has a twenty six percent interest in the company and they’re just a handful that essentially own the whole thing. So it’s not a real liquid public company there. So you have contango, smallish public, and independents, which holds almost all of the KKR energy real asset team if their game upstream holdings. So they consolidated all of those under the independence banner, nearly all of their holdings back, I guess, at some point and in the last year, and then merged that with Contango and in a reverse merger where they’re essentially going public and going to be able to take over the publicly traded vehicle. Right. And post-merger. So I think pro forma enterprise value is like five point seven billion when it’s all said and done based on Contango share price at the time of the deal, the value that they’re getting for independence was at four points four. So that’s what we came up with that number and where might vary from some of the other. You often see that talked about just the five-point seven billion-dollar deal, which is the pro forma enterprise. But yeah, the four-point four Independence Ticker’s interest. It’s hard to get a read-through on exactly what they have. We know some of their positions have a pretty good size. Holding in the Eagle Ford is our portfolio company called Barnardo that we imagine is included in this Hesam Blackwell, Eagle Ford assets the bottom line up in the Eagle Ford over the years and really manage this more as a yield focused company versus a growth company. So when we talk private equity, we often talk about the short-handed. It gets turned by drill flip where they go out, buy a piece of acreage that has a potential but wasn’t necessarily proven. Take some geologic risk, their drill, if you will, prove it up and flip it to a public company. And it was kind of a higher risk, high return business, which bit with some of the models that their investors were looking for. The KKR Energy Real Assets Team hasn’t been run like that. They’ve gone out and bought PDP heavy cash flowing assets and management for yield, basically, and they plan on continuing to do that as a publicly traded vehicle. Being public lets them have a broader, I guess, base to continue to leverage that model a little bit lower cost of capital usually associated with being public versus being a private. And from the commentary there, you know, they look like they’re probably going to be an inquiry once this merger is completed and they see additional opportunities out there, a pretty big opportunity set that could be broken down. There’s some sort of walking dead small publics out there that just really don’t have the universe has gotten smaller, but they don’t have a whole lot of future or growth that they’re really just waiting for somebody to come along and stack them up. So that’s one opportunity set for them. There are other private equity positions that are out there that still haven’t found an exit, would likely be willing to take equity in. And a well-run public company is an opportunity. So there’s another set for them. And then there are non core assets being sold by public companies, which are still hyper-focused on capital discipline, capital returns to shareholders in these things we’ve talked about. So they’re focused on a few core areas. And you imagine they’re probably going to be selling some not core assets. So they see sort of attractive opportunity set out there for themselves to go out and pick up those assets rather than paying PDP values on them and act as a consolidator there. So it’ll be interesting to watch what they do once once they get this sucker closed.

Speaker 3 [00:17:27] This episode of the Energy Newsbeat podcast is brought to us by King Operating Corporation, your partner for oil and gas investments. Check them out. King Operating Dotcom.

Stu Turley, Sandstone [00:17:38] Well, I’ll tell you what, I would fail the test. The Andrew Ditmar did you phenomenally. I mean, you’re just battering all this stuff that is really cool on the equity deal. I mean, you know, your stuff and this is just really funny. And they ended up not to mention, oh, no, you’re doing great. I have to fact-check myself every morning. I have to make sure I’m the right guy here. And I had my own Easter eggs, by the way, Andrew, just in case you ever need to know that, but t without that only look like two-point nine on your chart. What do you think about that? And yes, the northeast Marcellus

Andrew Dittmar, Enverus [00:18:22] yeah, I think I think that fits the trend we’ve been talking about as a private selling out, but making the accretive acquisition, they’ve been quite a bit more aggressive on the M&A front since the Wright brothers took over control of the company. You saw them do a deal last year with they bought Chevron’s, I believe, Appalachian assets and have been mostly focused more on the Southwest Marcellus. And with this Alt-A dealer moving up into the northeast, that’s a great, great area, the Marcellus to be in. I think if I recall correctly, a big piece of that deal is gone up under Chesapeake, which normally you don’t want to necessarily have so much of your value tied up in an on up. But Chesapeake on some of the best acreage in that part of the play and post reorg that really prioritized gas. So I think 90 percent of the twenty twenty-one CapEx is supposed to go to either the Marcellus or the Haynesville, about 50 50. So anticipate that the drilling that pretty heavily Chesapeake, despite the ups and downs of financial markets or top tier shale company, it’s holding a big line up underneath them active play. They’re intending to target a pretty good spot for you to be. Plus the owner-operated acreage you’ll have there. So I think here in advance we’re pretty bullish on gas. Obviously, we’ve had a run-up in gas prices, but we see that rally sticking around and maybe even a little bit more potential upside out there. So I think I think we’re bullish on gas and it’s a good time to be doing good gas deals and good parts of the place.

Stu Turley, Sandstone [00:19:59] So do you think the higher gas prices and higher oil prices are going to slow down the nominee, or do you think it would speed it up?

Andrew Dittmar, Enverus [00:20:10] Yeah, I think it’s a it pulls in both directions and you’re never quite sure which one is going to win out in that and that type of work. And so it definitely gives buyers some confidence, opens up some of your financing options. It’s a lot easier to do a deal. It’s accretive on cash flow and you’re bringing in more cash flow for every barrel see after selling. All right. Supporting equity prices, which I think public companies having higher equity values are helping to spur some of these acquisitions, especially when you’re forking over stock if you’re able to do it with a fairly decently valued share. You’re not handing over so much stock to still get a pretty decent headline number for the private equity seller. And so if the deal is more accretive as opposed to being diluted, so on those terms, it gives you some tailwinds for M&A, particularly that public to private life we’ve seen in terms of the public mergers, it may push back a little bit more against M&A. And I think we did see more of those when the outlook for commodity prices was not awful. You get to a point where basically the market shut down, which is what we saw in the first half of last year when it was really, really big, unknown out there. And oil prices were hitting a tailspin. And CNBC was running articles about the negative, negative crude prices. Even those of us in the industry, that isn’t quite the way to one’s actually selling out of the wellhead to negative 20 dollars, but it made for a scary headline. So you need some support there and commodity prices, but we’ve run up to now, you know, some of these smaller companies probably don’t feel the urgency to sell that they would have price level back. You know, you can deliver a little bit more organically when you have strong cash flows. You can tackle those debt loads. There were issues, but then you can actually start to talk about initiating a dividend for your shareholders or doing some share buybacks, keep them happier. So I think long term if you want to take a five-year perspective, the case out there for public company consolidation is still as strong as it ever is. All those things we’ve talked about over the years, I mean, the need for scale, the best ability to only a handful of companies, how much more efficiently the US supply will be controlled? There are a few bigger players, the small ones, all those are still there. And I think the industry will move towards consolidation over the years. But definitely higher gas prices take some of the urgency out of that and make sure some of these smaller guys to stick around. Is independence a little bit longer.

Stu Turley, Sandstone [00:22:44] So you’re saying in the terms of, Andrew, higher gas prices and higher oil prices means the walking dead can walk further? Is I just getting so I mean, that gives a little extra a little bit further?

Andrew Dittmar, Enverus [00:23:02] We’ve got to we’ve got in a different classification here. We have we’ll call them, you know, sub 500 million market cap guys that it probably doesn’t matter where commodity prices go. They’re not all that investable. Right. And then you’ve got guys that were sub 500 million market cap back in mid-twenty. But with the rally in crude prices, they actually have pretty decent assets and their balance sheets aren’t terrible. And they’re the ones that maybe have some legs now with commodity prices where they are. So there have been some you can’t escape the Walking Dead. And I think there’s a number of companies that have done that here at commodity prices, too. And I think it still makes sense for them to be consolidated longer term, but they’re not in any rush to do so.

Stu Turley, Sandstone [00:23:46] Oh, I love your terms, Andrew. Well done. When we talk about even had the global aspect on some of these things and the Canadian kind of things going on, you know, we’ve had a couple of interesting problems with Canada, with the closing of the pipeline, the Keystone pipeline. That was painful. We have line five in line three, having lots of problems and everything else. And on the Canadian slide deck, you have here that it saw more M&A than average in Q2. Could you give us a few of your thoughts on Canada in the upstream deal values in their?

Andrew Dittmar, Enverus [00:24:33] Yeah, so I’m not nearly as familiar with the Canadian market as I am in the US and oh, OK, we’ve got since we’ve merged with our US, we’re now owned in Paris and Berlin, actually based in Calgary. We have some very sharp Canadian analysts out there that could certainly speak much more fluently to that than I can. But just at a very high level, you know, the trends in the U.S. and Canada often rhyme with each other anyway, always exactly in sync. But they to do tend to move in the same direction. So the same push for consolidation that we’ve seen here in the United States is also present in Canada. And, you know, I think commodity prices, when they were so beat up these companies didn’t really see a way forward on some of these deals. But they’ve hit a point where it makes sense to merge. And it’s a tip of the scale and some of their key unconventional plays like the Montney back towards being economic. And, you know, the same factors at play. I mean, we’ve seen some of the private’s exits by sales to the public. We’ve seen some mergers between the public companies. I think it’s mostly been not oil sands, which were big drivers of Canadian demand eight years ago. But it’s been quite a big Montney activity, maybe some DeVonté and some other just general light oil assets out there. So, yeah, green shoots in the Canadian market as well and makes its case for consolidation there that we’re seeing here in the US.

Stu Turley, Sandstone [00:26:00] Sounds fantastic. And this may be an off-base question and that is on your analysis and going through and reviewing the value of a company, the CSG crop into some of those. I mean, some of those formulas, they have to say, hey, we’re doing this for ESG. But how does that play into the assessment of a company’s value if that is a checkoff box?

Andrew Dittmar, Enverus [00:26:28] Yeah. No, I think it is an important checkoff box in this market. I think we’re still in the process of figuring out what role that’s going to play exactly. But we’re used to talking about deals. It’s accretive on a cash flow basis, is accretive on a free cash flow basis. And that, we say is accretive on an ESG basis. So if you want a deal that’s going to improve your ESG metrics that harms them. And so if you’re interested in being a potential seller, whether you’re a private equity-backed company or whether you’re at the smaller public, both for your own benefit as an existing company and as a potential target, if you really have your ESG points nailed down and a larger company that’s focused on this compound by you and it helps improve their overall metrics, you know, it’s going to make you considerably more attractive, I think, in overall valuation. So that is going to is playing a role in M&A and we’ll probably play a greater role as we move forward.

Stu Turley, Sandstone [00:27:26] Oh, fantastic. Kind of another fun question for you, and that is carbon capture is it fits into ESG and trying to go into the green. You’re out. I don’t know. And I’m just throwing this out as a discussion point on carbon capture and those kinds of things are those buzzwords that are also in the ESG discussion points that you have, or have you seen those in any of those?

Andrew Dittmar, Enverus [00:27:51] Yeah, I mean, I think that’s another area that’s being figured out and it’s kind of captured plays a role there that may be a little bit more specialized way. We’re probably drifting further and further from my real area of expertize that

Stu Turley, Sandstone [00:28:10] I was just cool. I was just kind of figuring out because I haven’t seen it and I didn’t know if you had seen it on the M&A type stuff, so I hadn’t seen any of that in there yet. So but then again, you sit there and say it’s coming around the corner and you guys are seeing all that. So I’ll tell you what, we’ve got about three or four more minutes. And Andrew, I really appreciate your time. You hit it out of the park with your knowledge. And I just really appreciate it. And I hope you get to go to the tape. And I’d love to sit down and buy a cup of coffee and pick your brain because your report and the rest of your team’s report were absolutely phenomenal.

Andrew Dittmar, Enverus [00:28:53] So joining me now is always great to be on.

Stu Turley, Sandstone [00:28:57] Now, give us a few thoughts. The world, according to Andrew, in some crystal ball in the next few months. Just your general thoughts.

Andrew Dittmar, Enverus [00:29:11] Sure, so

Stu Turley, Sandstone [00:29:14] he as he calmly leans back,

Andrew Dittmar, Enverus [00:29:18] the old liberal predictions are hard, especially about the future. You know, I think. We probably expect more of the same for the most part. The last week’s been a little bit interesting in terms of oil prices and equity prices, you know, all of a sudden it’s great to have put it behind us and now they’re throwing out these variants that are floating around. And the market got a little spooked late last week going into Monday. I think last time I checked, it was rallying today. So if you get some more volatility back and we talked about you asked if the higher crude prices helped or hurt M&A. And I kind of gave you the answer that maybe a little bit of both. I can pretty unequivocally say that volatile crude prices kill the enemy. So when you’re bouncing around like maybe you’re headed back towards it doesn’t do anybody any favors. So if we see increased volatility in the market, that’s certainly going to hurt the deal flow, you know, provided that the prices settle down and hold more or less it higher prices, I don’t know. We need to be exactly where we topped out, but we need to be probably north of fifty-five on strip pricing for crude and then somewhere north of three through twenty-five, one strip for gas. And provided we hold those prices we expect it to continue. We think there’s lots of private equity still left to exit, maybe not some of the big marquee deals like a double point. I mean there are a few out there plus we talked about earlier. But just by its nature, as you move through these kinds of really active periods, you tend to winnow out the deals that are available. The guys are really on the edge and want to sell, find a deal. Who doesn’t want to buy the same deal? So you just kind of naturally lose a little momentum as you go. I always thought that the public side to was 20, 20 was just going wild. I mean, gosh, there was a point where we got to like 20 billion dollars in public mergers in two days, I think with oh, my kind of go Concho and pioneer Parzania was like the next afternoon. And so then you sort of getting when I think more M&A provided volatility, that doesn’t spike, but maybe on a smaller scale than what we saw it or that we’re going to. Visit 30 billion-plus in the quarter for the rest of the year, so we’ll be closely watching crude prices and see where that takes us.

Stu Turley, Sandstone [00:31:42] So this race would be even more volatile than billionaires trying to get to space. So we had had that race going on as well. I think it was.

Andrew Dittmar, Enverus [00:31:55] Yeah, that’s right. Bezos just got back. So just a no big deal. Just a quick, quick, quick trip up there. You know,

Stu Turley, Sandstone [00:32:03] hey, at least that’s one checkbox you and I are probably not going to be on any time.

Andrew Dittmar, Enverus [00:32:08] Yeah, but that’s right. And it’s pretty far down the bucket list. So, you know, we’re talking about difficulties making it to Houston these days. OK, you know, if if I have to go a year to get across the state, my perspective, it means basically.

Stu Turley, Sandstone [00:32:25] Excuse me again. Thank you, Andrew. It is clear that investors must think of you as a very good resource. You are actually very knowledgeable and very much impressive. So, again, thank you for stopping by.

Andrew Dittmar, Enverus [00:32:40] So, yeah, it is always, always great to be on and look forward. Hopefully, see you in person here before long. Sounds great.