You can’t change the spots on a leopard, and the IRGC will not change.

The world is adding plans for a long-term problem in the Strait of Hormuz, and we cover the next steps to ensure Energy Security. Countries are not holding their breath and realize that energy security is taking center stage amid so many geopolitical issues around the world, and Energy without Choke Points is now part of many leaders’ plans.

The Energy Realities Team of Dr. Tammy Nemeth, Irina Slav, David Blackmon, and Stu Turley will address some of the changes in the world today.

1. Strait of Hormuz & Geopolitical Energy Security

The panel discusses Iran’s leverage over the Strait of Hormuz and how countries are developing alternative routes to bypass this chokepoint. They predict that within three years, Persian Gulf nations will have reduced their dependence on this route, diminishing Iran’s geopolitical power. Kuwait and other nations are negotiating pipeline deals with Oman and Saudi Arabia.

2. Europe’s Energy Dependence & Green Hydrogen Fantasy

A major focus is on Europe’s unrealistic reliance on green hydrogen and biofuels to reduce energy imports. The panel criticizes the €1 billion “hydrogen valley” project in Spain, arguing that green hydrogen cannot realistically reduce Europe’s import dependence from 50% to 24-28% by 2040. They highlight the massive infrastructure costs and note that BP and Shell have already canceled their major green hydrogen projects in Europe.

3. Norway’s Natural Gas Expansion vs. EU Restrictions

Norway is reopening closed natural gas fields and proposing 70 new exploration locations, but faces backlash from EU environmental groups. The panel notes the irony that Norway is Europe’s most reliable energy source, yet the EU restricts Arctic drilling while pushing expensive green alternatives.

4. UK’s Net Zero Policies & Energy Crisis

The UK is tripling down on net zero policies, focusing on wind and solar while planning to monitor and control consumer energy usage rather than building reliable energy infrastructure. The panel warns this approach will lead to energy shortages and higher costs.

5. Permitting & Regulatory Delays in the West

A critical theme is how Western countries (US, Canada, UK) face years-long environmental assessments and lawsuits that delay energy projects, while Middle Eastern countries build infrastructure rapidly. Examples include:

A US refinery taking 10 years to permit (coming online in 2027)

Louisiana’s fertilizer facility facing regulatory delays

Contrast with UAE doubling pipeline capacity in one year

6. Middle East Pipeline Competition

Turkey, Israel, and UAE are positioning themselves as regional energy hubs. Israel is proposing a pipeline through Gaza to export gas to Europe, while the UAE is expanding its pipeline capacity to the Gulf of Oman.

7. Global Fertilizer Crisis & Food Security

The panel discusses how fertilizer shortages (partly due to redirected production to green initiatives) could cause food insecurity in Africa. Nigeria’s petrochemical facility with fertilizer production is highlighted as critical, though there’s concern it may be exported to the EU rather than serving African farmers.

8. Data Centers & Energy Demand

Data centers are becoming a major energy consumer and facing PR problems similar to fracking. The panel discusses:

Governor Abbott’s requirement for data centers to bring their own power

UK prioritizing data center grid connections despite insufficient electricity

Elon Musk’s proposal for space-based data centers

The irony that monitoring unreliable grids requires more energy-intensive infrastructure

9. LNG & Canadian Energy Exports

Germany is signing long-term LNG contracts with Canadian facilities (like Cassilissums), though transportation via Panama Canal or around South America is lengthy. The panel notes European buyers are now hesitant about long-term US LNG deals.

10. Rig Counts & North American Oil & Gas Activity

Baker Hughes rig counts show the US at 562 (up 7 from last year) and Canada at 180 (up 42 from last year), indicating increased shale activity in North America.

11. UK’s Political & Infrastructure Challenges

Hinkley Point C nuclear plant delayed by Natural England (headed by a former Greenpeace activist with conflict of interest)

UK’s weak defense capabilities due to net zero prioritization

Potential leadership challenge to PM Starmer

Discussion of by-elections and political instability

Overall Theme: The podcast critiques Western energy policies as unrealistic and counterproductive, highlighting the contrast between ambitious net zero goals and the practical realities of energy security, infrastructure development, and geopolitical competition.

There is nothing finished about Iran right now. In fact, the IRGC says they will be charging tolls, and JD Vance says they won’t. Well, you can’t change the spots on a leopard, and wolves bite when in a corner, and the IRGC can’t tell the truth.

It seems like everyone is saying what they want their supporters to hear, and the true problem will become evident in a couple of weeks.

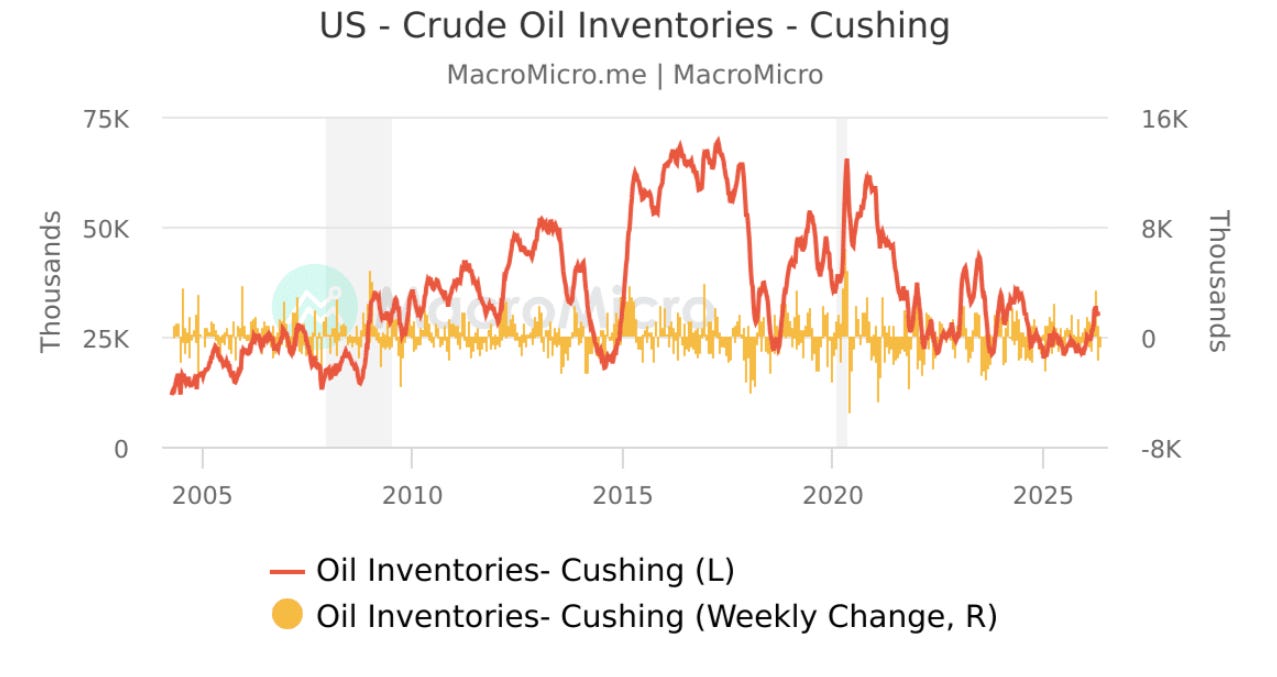

Cushing, Oklahoma — the critical delivery hub for West Texas Intermediate (WTI) crude oil futures — is rapidly approaching operational limits as inventories continue their steep decline amid global supply disruptions.

Latest EIA Data: Sharp and Sustained Drawdowns

According to the U.S. Energy Information Administration (EIA), commercial crude oil stocks at Cushing stood at 21.64 million barrels for the week ending June 5, 2026 — down 801,000 barrels from 22.441 million the prior week.

This marks the continuation of a multi-week drawdown trend. Stocks have fallen significantly from levels around 29 million barrels in early May.

Historical context of Cushing inventories (red line: levels; yellow: weekly changes).Net outflows have dominated due to strong refinery demand and surging U.S. crude exports filling global gaps created by Middle East disruptions (particularly the Strait of Hormuz). While detailed weekly inflow/outflow breakdowns are not publicly itemized in standard EIA reports, the consistent net draws reflect high outflows to refiners and export-oriented pipelines, with inflows from key basins (e.g., Permian) insufficient to offset demand. Midstream operators have reportedly redirected some flows northward to support Cushing, but analysts describe this as a zero-sum shift that strains other regions.

Approaching the Operational Bottom

Industry consensus identifies ~20 million barrels as the critical operational threshold at Cushing. Below this level, significant challenges emerge:

- Difficulty maintaining pipeline pressure and flow rates.

- Issues with floating-roof tanks (structural concerns or operational limits).

- Increased risk of pulling lower-quality crude containing sediments, water, and sludge from tank bottoms, complicating refining and export specifications.

- At the recent pace of ~800,000 barrels per week, Cushing could approach or breach the 20 million-barrel mark within 2–3 weeks (potentially by mid-to-late June), depending on the exact pace in upcoming data. The next EIA weekly report is scheduled for June 17, 2026 (covering the week ending June 12).

Implications for Refineries

Low Cushing inventories directly impact refineries, particularly those in the Midwest connected via pipelines originating from or through the hub:Supply constraints: Potential localized shortages or the need to source alternative (often more expensive) crudes.

Quality and operational issues: Risk of degraded crude quality if tanks are drawn too low.

Cost pressures: Higher basis differentials (local Cushing prices vs. futures) and potential impacts on refining margins.

Broader system strain as the hub struggles to meet all customer demands efficiently.

Implications for Consumers

For everyday consumers, the effects are indirect but meaningful:

Upward pressure on WTI crude prices can translate into higher gasoline and diesel prices at the pump.

Increased market volatility may cause sharper short-term swings in fuel costs.

In a context of already tight global supplies, sustained low inventories at this key U.S. hub add to the risk of elevated energy prices through the summer driving season and beyond.

The June 22/24 Contract and Potential Squeeze Dynamics

The NYMEX July 2026 WTI futures contract (CLN26) expires on June 22, 2026, with the first notice day around June 24.

This period is critical. Traders who short the contract and do not close positions face potential physical delivery obligations into Cushing. With inventories near operational bottoms and limited readily available physical barrels, covering shorts or fulfilling delivery could become difficult — setting up conditions for a short squeeze as paper-market positions collide with physical scarcity.

Even if geopolitical tensions ease and the Strait of Hormuz reopens, physical resupply lags significantly. Tanker transit times (often 35–40+ days around alternative routes) mean the current drain on U.S. inventories will persist for weeks.

Insights from Chevron CEO Mike Wirth (Bloomberg Interview)

In a recent Bloomberg interview highlighted by market analyst Jack Prandelli, Chevron CEO Mike Wirth noted that global markets may be able to absorb Strait of Hormuz disruptions until early September (around Labor Day). Key buffers include:

- Lower Chinese crude demand.

- Ongoing global inventory drawdowns.

- Limited (but ongoing) tanker movements through the strait (with some vessels reportedly moving at night or with support).

Wirth estimated actual flows through Hormuz closer to ~3 million barrels per day — lower than some higher official estimates. This suggests inventories are providing a temporary cushion, but as Cushing data shows, these buffers are depleting rapidly in key physical locations.

Bottom Line: Physical Reality vs. Paper Market

Recent price softness (potentially driven by hopes of diplomatic progress) appears disconnected from the tightening physical picture at Cushing. With inventories on track to test operational limits soon, upcoming EIA data and the July contract expiration could force a reckoning between paper positions and physical constraints.

The situation underscores how quickly logistics and storage realities can override headline-driven sentiment in energy markets.

Buckle up, we are in for some turbulence.

Check out for Stu Turley on The Energy News Beat Substack: https://theenergynewsbeat.substack.com/

For David Blackmon https://blackmon.substack.com/

For Tammy Nemeth https://thenemethreport.substack.com/

For Irina Slav https://irinaslav.substack.com/