In a striking display of operational resilience amid escalating geopolitical tensions, Abu Dhabi National Oil Co. (Adnoc) is quietly keeping a trickle of liquefied natural gas (LNG) exports flowing from the Persian Gulf. According to Bloomberg reporting, Adnoc tankers have turned off their Automatic Identification System (AIS) signals—effectively “going dark”—to safely navigate the Strait of Hormuz following the outbreak of the U.S.-Iran conflict in late February 2026.

At least two LNG carriers loaded at Adnoc’s Das Island export terminal in recent weeks have employed this tactic. Satellite imagery from Copernicus confirms continued vessel activity at the facility, even as most commercial shipping has halted in the region.

One example is the tanker Mraweh, which went dark after loading and was later spotted near Indonesia, reportedly bound for Japan. A second vessel, the Mubaraz, followed a similar pattern earlier, reappearing off the Indian coast.

Geopolitical Chokepoint Under Pressure

The Strait of Hormuz, a narrow waterway connecting the Persian Gulf to the Arabian Sea, handles roughly 20% of global LNG trade—primarily from Qatar and the UAE. Since the conflict intensified in early March 2026, tanker traffic has plummeted, with most vessels anchoring, making U-turns, or remaining in safe waters. Qatar’s Ras Laffan facilities have also suffered damage, further constraining supply.

Adnoc’s strategy highlights the UAE producer’s determination to maintain exports from its 6 million tonnes per annum (mtpa) Das Island plant. While volumes remain limited compared to pre-conflict levels, these successful transits demonstrate that not all Gulf LNG is frozen in place.

LNG Market Outlook: Tight Supply Meets EU’s Critical Filling Season

Global LNG markets were already bracing for a supply wave in 2026, with forecasts pointing to growth of more than 7% (over 40 billion cubic meters) driven largely by new U.S. and other non-Middle East capacity. However, the Hormuz disruptions have created immediate tightness, removing up to 20% of global supply flows and delaying the anticipated rebalancing by at least one to two years. Analysts now project cumulative supply losses of around 120 bcm through 2030.

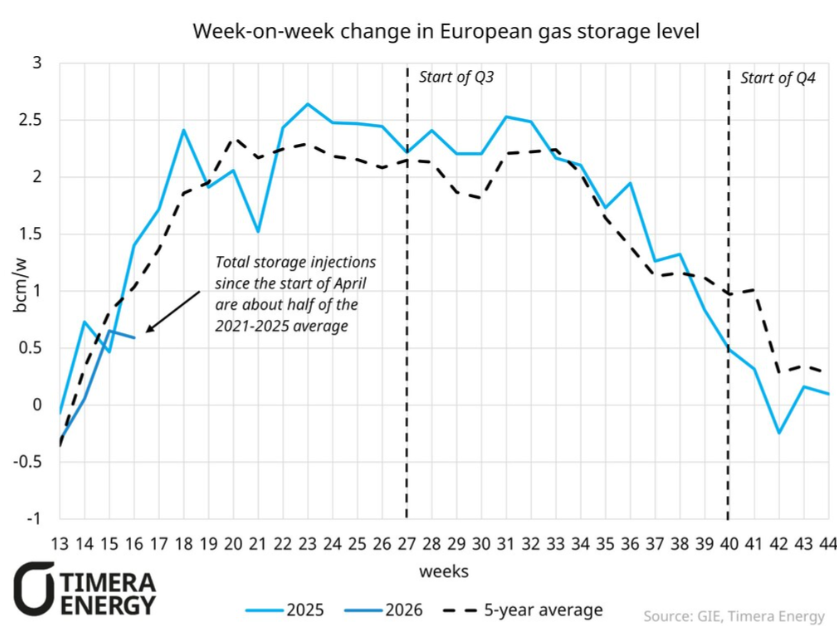

Europe is feeling the pinch as it enters the summer injection season for the 2026/27 winter. As of May 5, 2026, EU gas storage stands at approximately 34.2% of capacity—well below the five-year average and lower than the same period in recent years. ENTSOG and ACER assessments indicate the bloc can reach an 80% fill level by November 1 under current LNG import rates (~11 bcm/month), but hitting the full 90% target will be challenging without additional flexible cargoes.

EU Storage – Source Timera EnergyEuropean buyers are competing head-to-head with Asian markets for Atlantic Basin LNG (primarily U.S. and Australian volumes). Spot prices have remained elevated, with JKM LNG around $16-17/MMBtu in recent weeks, supporting higher revenues for exporters outside the Gulf but raising refill costs for Europe. Demand response, including industrial curtailment and fuel switching in Asia, is helping balance the market, but the outlook remains fragile.

Implications for Investors

The Adnoc tanker maneuvers and broader Hormuz crisis carry clear signals for energy portfolios:

Short-term upside for diversified LNG exporters: U.S. producers and midstream players (e.g., those tied to Sabine Pass, Corpus Christi, or upcoming projects) stand to benefit from Europe’s urgent refill needs and Asian spot-market competition. Higher netbacks and utilization rates are likely through summer 2026.

Shipping and logistics volatility: LNG carriers capable of operating in high-risk zones, along with war-risk insurance providers, could see premium rates. However, operational risks and potential escalation remain material concerns.

Storage refill pressure supports prices: Low EU inventories and constrained Middle East supply point to sustained price support for TTF and JKM benchmarks through the injection season. This favors flexible, non-Russian supply chains and could pressure European utilities with high gas exposure.

Longer-term rebalancing: Once the conflict resolves and new liquefaction capacity ramps (U.S.-led wave expected post-2027), prices could moderate. Investors should monitor geopolitical developments, FID activity outside the Gulf, and Europe’s demand-side response (e.g., accelerated renewables or nuclear).

Portfolio diversification: The episode underscores single-chokepoint risks. Exposure to resilient supply routes, U.S./Australian LNG, and alternative energy infrastructure may offer better risk-adjusted returns over the medium term.

In summary, Adnoc’s “go-dark” tactic is a tactical win for UAE LNG flows, but it also spotlights the vulnerability of global energy trade. For investors, the near-term environment favors those positioned in flexible, non-Middle East LNG supply amid Europe’s storage refill scramble—yet vigilance around escalation risks and the eventual arrival of the delayed supply wave is essential.

- Bloomberg: “Adnoc’s LNG Tankers Go Dark to Get Gas Shipments Through Hormuz” (May 7, 2026) – https://www.bloomberg.com/news/articles/2026-05-07/adnoc-s-lng-tankers-go-dark-to-get-gas-shipments-through-hormuz?srnd=homepage-americas

bloomberg.com

- Reuters reports on Adnoc tankers Mubaraz and Mraweh transits (April-May 2026) – https://www.reuters.com/business/energy/second-adnoc-lng-tanker-crosses-strait-hormuz-amid-iran-war-ship-tracking-data-2026-05-06/

reuters.com

- IEA Gas Market Report Q1-2026 and related updates on Middle East disruptions – https://www.iea.org/reports/gas-market-report-q1-2026/executive-summary

iea.org

- ENTSOG Summer Supply Outlook 2026 (April 9, 2026) – https://www.entsog.eu/sites/default/files/2026-04/PR0366_260409_Press%20Release%20ENTSOG%20Publishes%20Summer%20Supply%20Outlook%202026%20and%20Summer%20Supply%20Review%202025.pdf

entsog.eu

- ACER: “Filling EU gas storage will be expensive in a competitive LNG market” (April 23, 2026) – https://www.acer.europa.eu/news/middle-east-impact-filling-eu-gas-storage-will-be-expensive-competitive-lng-market

acer.europa.eu

- Gas Infrastructure Europe (GIE) / AGSI+ storage data (updated May 2026) – https://agsi.gie.eu/ and https://energiedashboard.admin.ch/gas/eu-gasspeicher

energiedashboard.admin.ch

- Additional context from Oxford Energy, Argus, and S&P Global LNG outlooks (2026).