TotalEnergies CEO Patrick Pouyanné recently put it plainly: US LNG cannot fully replace Qatar. Oil markets have substitutes and buffers that can ease pressure. Gas does not — at least not in time for winter 2026-27.

This assessment comes amid a rapidly evolving situation in the Middle East. Following Iranian strikes on Qatar’s Ras Laffan facilities in mid-March 2026 and the closure of the Strait of Hormuz, Qatar — the world’s second-largest LNG exporter — halted production and declared force majeure. The attacks damaged two liquefaction trains (Trains 4/S4 and 6/S6), knocking out approximately 12.8 million tonnes per annum (mtpa), or about 17% of Qatar’s pre-crisis nameplate capacity of roughly 77 mtpa.

Qatar’s Restart Preparations Underway

As of mid-June 2026, signs of recovery are emerging. Following a preliminary US-Iran deal that has raised hopes for de-escalation and safe passage through the Strait of Hormuz, QatarEnergy is repositioning LNG tankers. Vessel-tracking data shows at least four Qatar-owned carriers and one chartered vessel heading toward Ras Laffan Industrial City, with others idling nearby in the Gulf of Oman.

However, the two damaged trains represent a longer-term setback. QatarEnergy has indicated repairs could take 3–5 years, meaning Qatar will effectively operate ~17% smaller (around 64 mtpa from undamaged trains) for the foreseeable future, even as it pushes ahead with major North Field expansion projects targeting 142 mtpa by 2030.

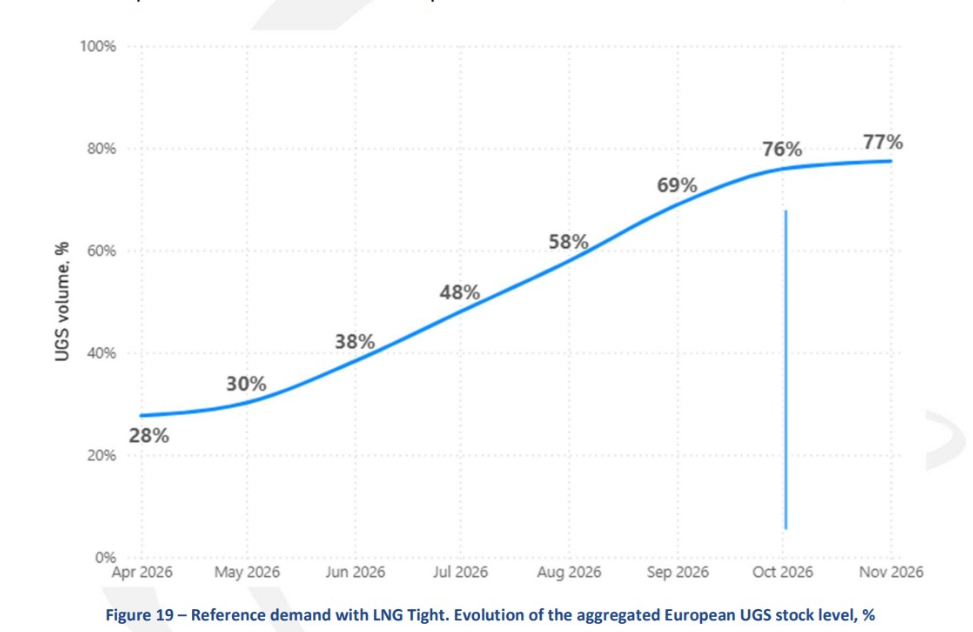

Europe’s Storage Refill Challenge

Europe enters the critical summer injection season in a precarious position. As of mid-June 2026, EU gas storage stood at approximately 42.8–45% full (around 46–51 bcm stored), well below year-ago levels and the five-year average.

The EU’s standard 90% target by November 1 has been relaxed to 80% under crisis provisions, but even this lower bar looks challenging. Analysts note that each month of lost Gulf LNG supply can drain roughly 10% of European storage levels. A prolonged outage risks pushing Q1 2027 TTF prices well above 2022 crisis highs.

Europe is on track for record LNG imports in 2026 (forecasts range from ~145 mt by Kpler to higher IEA figures around 185 bcm), driven by the need to refill storage and replace lost Russian pipeline volumes.

![]() US LNG Steps In — But Has Limits

US LNG Steps In — But Has Limits

US LNG has already begun filling part of the gap. US exporters have ramped up shipments, with Europe taking the lion’s share (often 70%+ of US cargoes in recent months). IEEFA projects the US will supply two-thirds of Europe’s LNG imports in 2026, potentially overtaking Norway as the continent’s largest gas supplier overall.

US exports hit records in 2025 and continued strongly into 2026, with extra volumes roughly offsetting the drop in Qatari loadings during the disruption period.

Yet, as Pouyanné highlighted, US LNG cannot be a complete substitute:

Much of the current and near-term US supply was already contracted before the crisis.

Global LNG supply in 2026 is still projected at least 30 mtpa below pre-war expectations, even assuming partial Qatari restarts by late summer. The much-anticipated “LNG glut” has been pushed to 2028–29.

Qatar’s long-term, oil-linked contracts and geographic positioning provided a specific type of reliable, large-scale supply that spot-flexible US cargoes (priced off Henry Hub) do not fully replicate in volume or timing for Europe’s immediate winter needs.

US LNG is helping ease the pain by boosting spot availability, supporting storage injections, and preventing an even sharper supply crunch. It provides critical flexibility and diversification. But the math remains brutal: without a swift and substantial return of Qatari volumes, Europe heads into winter 2026-27 with structurally tighter balances and a higher floor on gas prices.

The Road Ahead

A fast Qatari restart (50–80% within 1–2 months of Hormuz reopening) could bring meaningful relief and help stabilize TTF prices. However, the permanent 17% capacity hit from damaged trains, combined with ongoing global supply tightness, means the market will remain sensitive.

Longer term, buyers are already locking in new US and other flexible supply through multi-decade contracts, accelerating a shift that was already underway. Qatar, for its part, is accelerating its own massive expansion plans to reclaim market share.

Bottom line: US LNG is a vital bridge and mitigator right now. It cannot, however, fully replace Qatar’s scale and role in the near term. Europe will feel the difference this winter — and the coming years — unless both sources ramp reliably and geopolitics stabilize.

- Jack Prandelli X post (June 18, 2026): https://x.com/jackprandelli/status/2067588262646939662

- Full analysis on The Merchant Substack: https://themerchantsnews.substack.com/p/qatar-comes-back-17-smaller-thats

- Energy News Beat – Qatar Returns Tankers (June 17, 2026): https://energynewsbeat.co/exports/qatar-returns-tankers-in-preparation-for-restarting-lng-exports/

- Bloomberg – Qatar Plans Rapid LNG Restart (June 16, 2026): https://www.bloomberg.com/news/articles/2026-06-16/qatar-plans-to-rapidly-restart-lng-production-after-hormuz-opens

- IEEFA – Europe to source two-thirds of LNG imports from US in 2026 (May 13, 2026): https://ieefa.org/articles/europe-source-two-thirds-its-lng-imports-us-2026-dependence-deepens

- Kpler – European natural gas outlook 2026

- ACER LNG Monitoring Report 2026 and related storage analyses

- GIE AGSI+ storage data (via multiple reports, mid-June 2026 levels ~42.8–45%)

- Reuters and other reporting on Qatar force majeure and restart communications (April–June 2026)

All data reflects the latest available information as of June 18, 2026. Markets move fast — developments on Hormuz navigation and actual restart volumes will be key watchpoints in the coming weeks.