In a sharp escalation of tensions in the Persian Gulf, two Indian-flagged vessels—one a VLCC supertanker carrying approximately 2 million barrels of Iraqi crude—were fired upon by Iranian Revolutionary Guard Corps (IRGC) gunboats in the Strait of Hormuz on April 18, 2026. The ships, identified as the Sanmar Herald and Jag Arnav, were forced to reverse course and turn back. Crews are reported safe, with only minor damage to one vessel.

This incident comes as Iran has reimposed strict military control over the Strait, effectively closing it again to most commercial traffic after a brief and fragile reopening tied to a U.S.-Iran ceasefire. Iranian forces broadcast warnings that passage is denied until the U.S. lifts its naval blockade of Iranian ports. Ship-tracking data and maritime intelligence confirm multiple vessels turned back today, with reports citing at least four Indian tankers (Sanmar Herald, Desh Garima, Desh Vaibhav, Desh Vibhor) and two Greek vessels failing to transit.

Broader Context: Strikes, Turnbacks, and the Hormuz Chokepoint

The Strait of Hormuz, through which roughly 20% of global seaborne oil (about 21 million barrels per day pre-crisis) and significant LNG volumes flow, has been a flashpoint since the U.S.-Israel-Iran conflict intensified in late February 2026. Iran initially blockaded the strait in response to strikes, leading to:

Attacks on shipping: Ship-tracking data (Kpler) shows 22 vessels attacked since the war began, with traffic plummeting from ~100 transits/day pre-war to just 6-7 recently. The Sanmar Herald marks the latest in a pattern that includes other tankers hit near the strait.

Turnbacks and stranded vessels: Today’s events echo prior incidents. Bloomberg and marine traffic data report several tankers (oil, LPG, chemicals) U-turning in recent days/weeks. The U.S. Central Command noted 23 vessels forced to turn around since its blockade began on April 13. Overall, nearly 1,900 ships have been stranded or disrupted at various points, with Indian-flagged vessels particularly affected (dozens initially stuck in the Gulf).

Back-and-forth reopenings: Iran briefly declared the strait “fully open” earlier this week during the Lebanon ceasefire window, but re-closed it hours later citing U.S. non-compliance. Conflicting statements from Tehran, Washington, and vessel trackers have created chaos.

This is not isolated—history is repeating elements of the 1980s Tanker War, but on a faster, more leveraged scale amid modern geopolitics.

Doomberg has been on the Podcast many times, and we truly respect his opinions and recommend subscribing to his Substack. He will be back on the podcast after he finishes writing his book.

Energy markets are not reacting in a vacuum. Today’s Doomberg newsletter, Backwards Looking (published April 18, 2026), provides a timely, clear-eyed breakdown of why oil prices behave as they do right now.

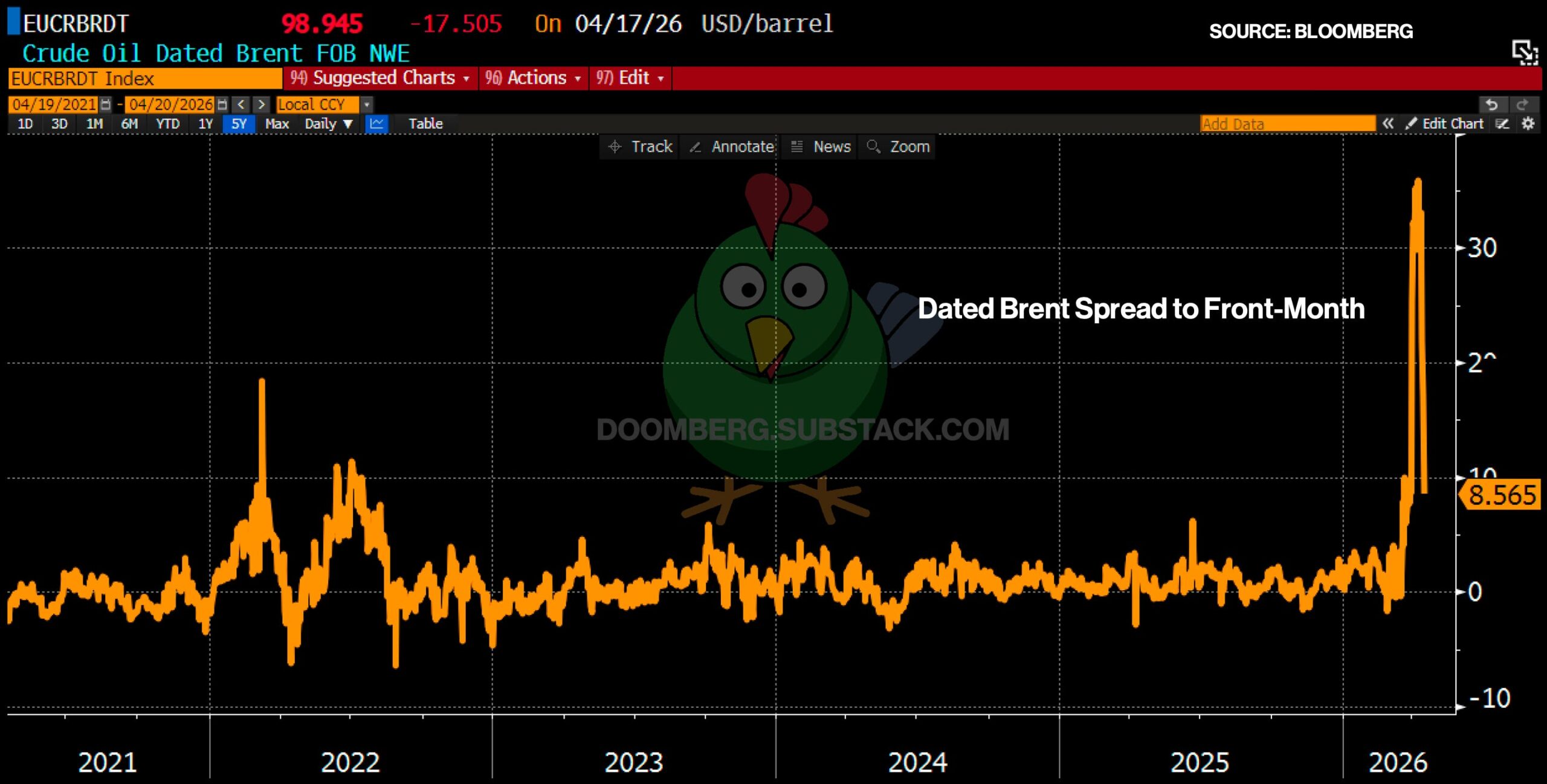

Doomberg explains there is no single “oil price”—it depends on grade, location, and timing. “Paper” prices (front-month futures like WTI on NYMEX or Brent on ICE) are what headlines quote. These are financial contracts settled in cash or with delivery options at specific hubs (e.g., Cushing, OK for WTI). In contrast, physical/delivery or spot prices (proxied by Dated Brent for seaborne crude) reflect the real cost of immediate barrels with attached shipping dates.

The newsletter directly tackles conspiracy claims of “fake paper prices” hiding a much higher physical reality (e.g., paper at ~$90-100 vs. alleged $140+ physical). It attributes extreme backwardation—near-term oil priced far higher than future months—to rational market forces amid the Hormuz war shock, not manipulation. Backwardation has widened dramatically beyond early Ukraine-war levels because the market is probability-weighting massive near-term supply risks with no easy historical parallel.

In short, Paper markets are signaling the physical crunch. Volatility reflects uncertainty over war outcomes, not a grand lie. Reopening Hormuz would ease this; renewed closure tightens it.

”

To some, this price action is not normal, but instead is proof that the “real” price of oil is much higher than the “fake paper” prices “they” are allowing to print on our collective screens. There are many versions of this claim, but this particular one—sent our way by many subscribers, with several hundred thousand views at the time of writing—captures the essence:

“I’m watching the numbers flicker on the screen — Brent crude at $92, WTI hovering near $97 — and I feel a profound sense of dread. This isn’t a market; it’s a meticulously crafted fiction. We are being lied to on a scale so vast it defies comprehension. The current paper price for oil is a government-constructed lie, a narrative woven by desperate authorities to maintain a false sense of stability while the physical foundations of our world crack beneath us.

This manipulation isn’t just an economic curiosity; it’s a trap. While futures traders cheer a modest pullback, the real cost of a barrel — the tangible liquid that powers tractors, heats homes, and transports food — has already rocketed into another dimension. This divergence between paper and physical represents the single greatest threat to global order I’ve witnessed in decades. It’s a dangerous fiction masquerading as reality, and its inevitable collapse will redefine everything we know about energy, money, and power.”

There is, of course, a much more innocent explanation for these prices, one that does not involve a grand conspiracy of manipulation. Instead, it involves a fair probability-weighting of two outcomes so unprecedented in their polarity that there is no accurate historical precedent by which to model them. Once properly contemplated, not only does the recent price action make sense, but the volatility that will surely follow does as well. Let’s unravel the mystery and brace for impact. – Doomberg

Source: Doomberg.com – We highly recommend subcribing to the Substack. And look forward to having him back on the podcast after he finishes his book.

Market Implications: Oil, Gas, LNG, and Beyond

Oil: A sustained Hormuz closure removes ~16-21 million bpd from global supply. Prices, which plunged 9-11% Friday on reopening hopes (Brent to ~$90, WTI to ~$84), are poised to spike again. Goldman Sachs and others have warned Brent could average well over $100 for 2026 if disruptions linger even a month. Physical premiums (Dated Brent spreads) will widen further in backwardation.

Gas and LNG: Middle East LNG exporters (Qatar, UAE) rely on safe passage. Tensions raise insurance and freight costs, tightening global LNG markets. Europe and Asia, already navigating high storage and alternative sourcing, face higher spot prices. U.S. LNG could see export arbitrage opportunities, but overall energy inflation ripples through.

Other markets: Higher oil feeds inflation (transport, plastics, chemicals). Energy stocks rally; broader equities may wobble on recession fears. Geopolitical risk premium stays elevated until clear safe-passage guarantees emerge (e.g., naval escorts).

Will the market crash on Monday?

Almost certainly not. Friday’s drop was on reopening news. Renewed closure and today’s strikes point to the opposite: a risk-off rally in crude futures and the energy complex. Any “crash” would require rapid de-escalation and full straight reopening—unlikely given the U.S. blockade stance and Iran’s leverage play. Expect volatility, but upward pressure on energy prices dominating headlines.

I have to hand it to President Trump, the Trump Administration, and our U.S. Military for leaving the blockade in place and not trusting them until the deal is done. They have surpassed “Baggdad Bob” and his horrible lying and stepped it up to an entirely new level of false representations.

The situation remains fluid. Diplomatic channels (via Pakistan and others) are active, but trust is low. For now, the Strait’s valve is shut again—and markets will price that reality aggressively.