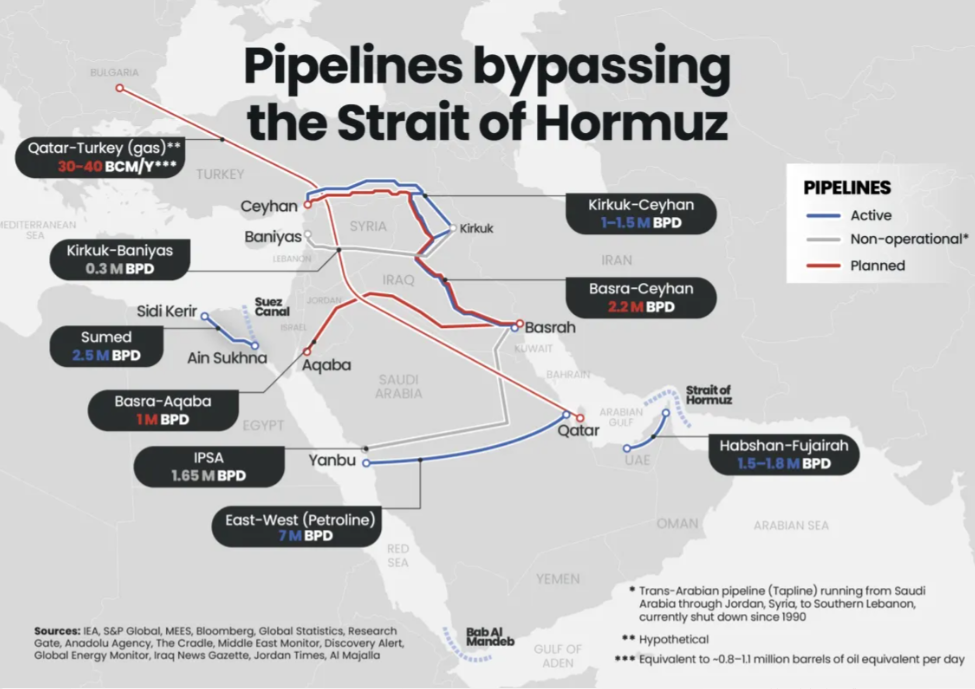

As tensions flare once again around the Strait of Hormuz—with recent incidents including a vessel struck off Oman’s coast and Iranian Revolutionary Guard warnings—Gulf oil producers are racing to secure alternative export routes. While the strait has historically carried nearly 20% of global seaborne oil trade, Iraq is moving decisively to reduce its vulnerability through accelerated northern and western pipelines. This builds on real-time flows already bypassing the chokepoint and parallels fast-tracked projects in the UAE, with Saudi Arabia leveraging its established infrastructure.

Iraq’s Northern Lifeline Already Flowing

Iraq’s North Oil Company has reversed flows on key pipelines, routing Basra crude northward to Kirkuk and onward via the existing export line to Turkey’s Ceyhan terminal on the Mediterranean. Volumes on this northern route are climbing toward 340,000 barrels per day (bpd) and delivering critical revenue after southern disruptions slashed Iraq’s exports earlier in 2026.

Last week, the Iraqi cabinet approved plans to accelerate exports through the Kurdistan-Turkey pipeline network, targeting a tripling of capacity from the current ~220,000 bpd to 770,000 bpd. The Kirkuk-Ceyhan agreement is set to expire on July 27, and Baghdad has already requested a one-year extension

Prime Minister Ali Falih al-Zaidi (sworn in mid-May 2026) is expected to advance these efforts during an upcoming White House visit, with cabinet formation targeted for early July to strengthen his negotiating position.

The Big Prize: $8 Billion Kirkuk-Baniyas Pipeline

Baghdad is accelerating its most ambitious project yet: rebuilding the historic ~850 km Kirkuk-Baniyas pipeline to Syria’s Mediterranean coast at Baniyas. A memorandum of understanding has been advanced with U.S. firm TI Capital, with reconstruction costs estimated at ~$8 billion. The deal is expected to include security guarantees that could bring major U.S. operators like Exxon and Chevron back into Iraqi fields.

Iraq is also advancing construction on a new Basra-Haditha pipeline (capacity cited up to 2.5 million bpd in some reports), which would enable westward exports via Jordan’s Aqaba port on the Red Sea or further to Baniyas.

These moves echo Iraq’s 1980s strategy during the tanker war—routing oil overland to evade threats in the Gulf.UAE Fast-Tracks Parallel Expansion

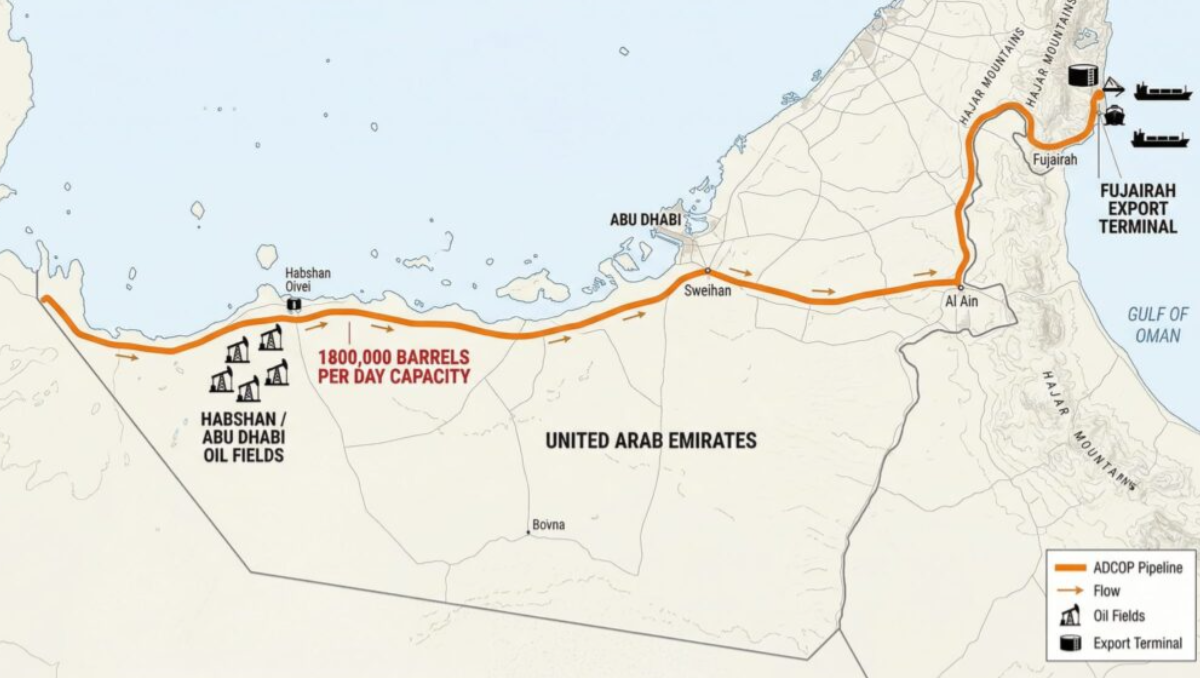

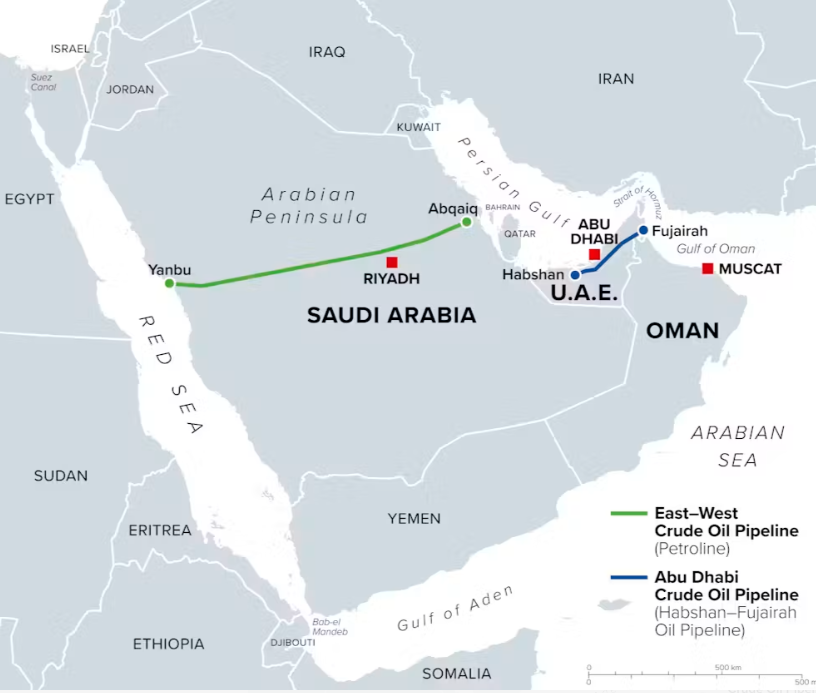

The UAE is not standing still. Abu Dhabi has directed ADNOC to accelerate its new West-East Pipeline (parallel to the existing Habshan-Fujairah/ADCOP line). The existing pipeline already carries up to 1.8 million bpd directly to Fujairah on the Gulf of Oman, fully bypassing Hormuz. The new line, already ~50% complete as of May 2026, is expected online in 2027 and will double ADNOC’s Fujairah export capacity to approximately 3.6 million bpd.

How Fast Could This Be Impactful?

Short-term (now–Q3 2026): Iraq’s northern route is already adding real barrels (targeting 340k–770k bpd via Turkey). This provides immediate revenue relief and market supply.

Medium-term (2027): UAE’s doubled Fujairah capacity comes online. Combined with Saudi Arabia’s established 7M bpd and Iraq’s potential Kirkuk-Ceyhan boost, non-Hormuz Gulf exports could rise meaningfully.

Longer-term (2–4+ years): Full Kirkuk-Baniyas rehabilitation and Basra-Haditha line would add substantial new capacity (potentially 1+ million bpd westward), though security, financing, and cross-border agreements in Syria/Jordan remain hurdles.

Collectively, these projects are shifting the Gulf from near-total Hormuz dependence toward diversified, resilient export corridors.

Impact on Global Oil Markets

These bypass accelerations enhance global supply security and reduce the risk premium historically priced into oil due to Hormuz vulnerability. Supply resilience: More barrels can reach markets even if Hormuz faces future disruptions (mines, threats, or blockades). This dampens price spikes from geopolitical events.

Potential downward pressure: As Iraq restores lost production/export capacity (southern flows were severely curtailed) and the UAE expands post-OPEC exit, additional supply could enter the market—especially if demand growth slows.

Stabilizing effect long-term: Diversified routes lower systemic risk, benefiting consumers and supporting steadier investment in upstream projects.

Price outlook: Near-term volatility may persist amid ongoing regional tensions, but structural improvements in bypass capacity should moderate extremes compared to previous crises.

Implications for OPEC and OPEC+UAE: Already exited OPEC (May 2026). No longer bound by quotas, it can pursue higher output aligned with its expanded bypass and capacity goals (targeting 5M+ bpd).

Iraq: Remains in OPEC+ but has signaled frustration with quotas that don’t match its capacity or post-war recovery needs. PM al-Zaidi has warned of the potential suspension of membership if quotas constrain output. Increased northern/western exports give Baghdad more leverage to push for higher allowances.

Saudi Arabia: As the de facto OPEC+ leader with the strongest bypass infrastructure, it maintains significant influence. Its demonstrated ability to reroute 7M bpd strengthens its hand in managing market balance.

Broader dynamics: The push for bypasses highlights diverging national interests within the group. Producers with alternatives (Saudi Arabia, the UAE, and increasingly Iraq) gain flexibility, potentially complicating coordinated cuts or adherence to quotas. This could accelerate a shift toward more market-driven production among Gulf members.

In summary, Iraq’s acceleration—building on already-flowing northern barrels and ambitious new pipelines—marks a strategic pivot toward energy independence. Combined with the UAE’s 2027 doubling and Saudi Arabia’s proven 7M bpd bypass, the Gulf is building a more robust export architecture. For global markets, this means greater resilience and potentially less volatile pricing tied to Hormuz risks. For OPEC/OPEC+, it introduces new pressures on quotas and cohesion as members prioritize national security and revenue maximization.

Appendix: Sources & Links

- X post by@argosaki(June 26, 2026): https://x.com/argosaki/status/2070467348549767216 (and thread)

- CNBC (June 9, 2026): “Iraq and UAE race to establish alternative oil pipelines” – https://www.cnbc.com/2026/06/09/iraq-uae-hormuz-oil-pipelines-oil-iran-war.html

- Reuters (May 15, 2026): UAE accelerates West-East pipeline – https://www.reuters.com/business/energy/uae-accelerate-oil-pipeline-project-help-bypass-hormuz-2026-05-15/

- Nikkei Asia (May 27, 2026): UAE and Iraq bolster pipelines – https://asia.nikkei.com/spotlight/iran-tensions/iran-war/uae-and-iraq-bolster-pipelines-to-bypass-hormuz-bottleneck

- WSJ (June 3, 2026): “The Hormuz Squeeze Is Redrawing the Oil Map for Good”

- Al Jazeera (May 15, 2026): UAE to accelerate oil pipeline project

- Various reports on Kirkuk-Baniyas/TI Capital (SANA, Cradle Media, June 2026)

- IEA and pipeline capacity references from multiple outlets (Saudi East-West at 7M bpd ramp-up)

- Additional context from UKMTO advisories and regional reporting on Hormuz incidents (June 25–26, 2026)

All information drawn from publicly reported developments as of June 26, 2026. Timelines and final capacities remain subject to political, security, and commercial developments.